Investment Thesis

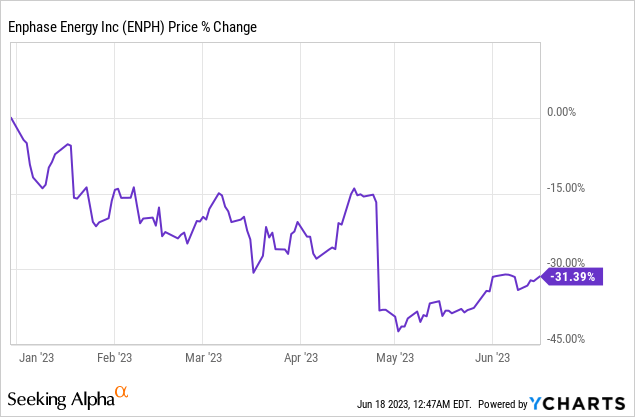

Despite the recent rally in the market, Enphase Energy’s (NASDAQ:ENPH) performance continues to be weak, with shares down nearly 30% YTD (year to date). The solar leader has now declined 45% from its all-time high in December, as the market is concerned about the company’s near-term outlook.

The massive decline seems like an overreaction as the company should continue to benefit from favorable market trends. In my previous article, I said that I really like the company’s growth prospects but the elevated valuation continues to be a major hurdle. After the recent drop, I believe the company is much more reasonably priced and the risk-to-reward also looks more favorable. Therefore I am upgrading Enphase from a hold to a buy.

Favorable Market Trends

I want to touch more on the market trends in this article as I believe Enphase is well-positioned to benefit from multiple long-term tailwinds. The massive solar energy market is poised to expand rapidly due to Energy Transition and the recent momentum continues to be very encouraging.

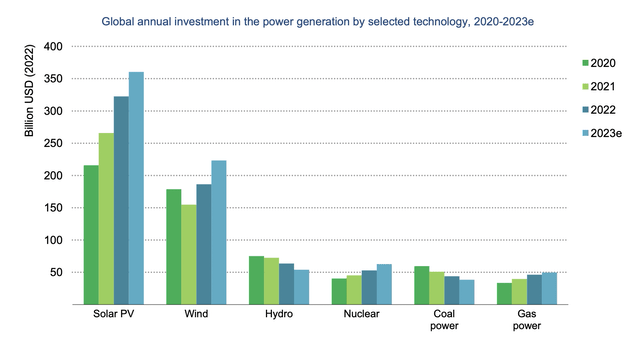

According to Grand View Research, the global market size of solar energy systems is forecasted to grow from $189.5 billion in 2022 to $607.8 billion in 2030, representing an excellent CAGR (compounded annual growth rate) of 15.7%. As shown in the chart below by IEA (International Energy Agency), solar PV (photovoltaics) is by far the clear leader in renewable power generation, and its global investment is set to increase by 10.8% from $325 billion last year to $360 billion this year, which should continue to drive market expansion.

IEA

Upbeat Installation Rate

The recent traction was encouraging in both the residential and commercial segments. During the first quarter of 2023, residential solar PV installations amounted to 1641MW, up 31.6% YoY (year over year) compared to 1247MW. Commercial installations also grew 23.3% YoY from 317MW to 391MW, according to the SEIA (Solar Energy Industries Association).

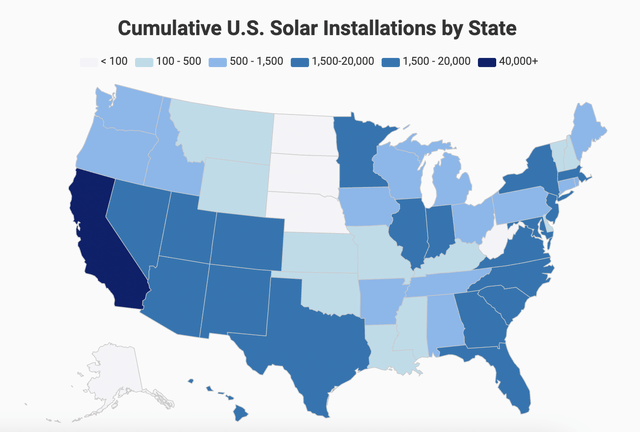

While the number of residential solar installations had grown significantly in the past few years, there is still ample room for further increases. As you can see in the picture below, the penetration rate of solar energy systems is still pretty low outside of California, especially on the northern side. The SEIA estimate that solar installations outside of California will grow 50% from 4000MW in 2022 to 6000MW in 2026. The rising solar installation in other states should be a major growth driver for Enphase moving forward.

SEIA

Declining Costs

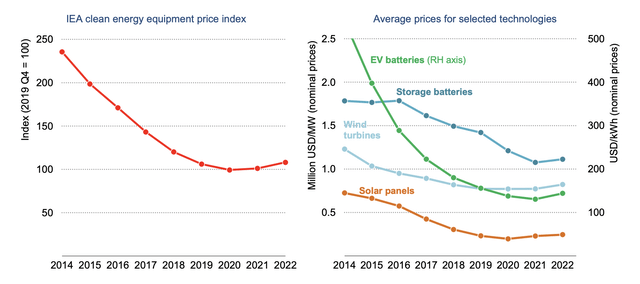

The cost of solar energy systems is also set to continue its decline, which should further increase its affordability and attractiveness, especially to households and small businesses. As shown in the chart below, the price index of clean energy equipment has dropped over 54% from 240 in 2014 to 110 in 2022, thanks to the advancement in technology and the expansion in scale.

The price index had rebounded in the past two tear due to elevated inflation, but it should start heading back down as inflation eases. For instance, the US CPI (consumer price index) for May came in at just 4%, down from 4.9% in the prior month and 9.3% in the prior year. The US PPI (producer price index) was even softer at just 1.1% YoY, which should favor pricing moving forward. The lower inflation should benefit Enphase as costs continue to decline.

IEA

Accommodative Policies

The overall costs and demand of Enphase should also benefit substantially from the Inflation Reduction Act (IRA) that was passed last year. The IRA is aiming to facilitate green energy transition through tax credits and rebates, which are available to both households and businesses.

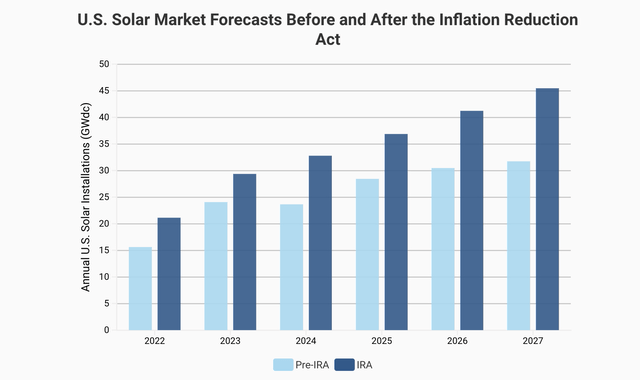

For instance, manufacturers can get a 30% investment tax credit for eligible investment costs in facilities and equipment. Or they can also choose to claim a production credit for certain components based on the volume of product manufactured. As shown in the chart below, the SEIA projects the IRA can boost solar deployment by 34%, while the IEA expects the capital costs for companies to be reduced by up to 15%.

Badri Kothandaraman, CEO, on IRA boosting capacity

The IRA will help bring back manufacturing to the US. We are opening manufacturing lines with three different manufacturing partners, adding a capacity of 4.5 million microinverters per quarter, bringing our overall global capacity to 10 million microinverters per quarter as we exit 2023.

The favorable policies are also seen in other regions. In Europe, the REPowerEU plan and the Net-Zero Industry Act proposal by the European Commission aim to increase renewables to 45% of Europe’s energy generation by 2030. Asian countries like Indonesia and the Philippines are also targeting renewables to account for 34% and 35% of power generation by 2030. These green political trends across the globe should continue to provide strong tailwinds for Enphase moving forward.

SEIA

Second Quarter Outlook

Enphase’s second-quarter guidance came in below the consensus but it is by no means weak. The estimated revenue of $700 million to $750 million still translates to a growth of roughly 37% at the midpoint, which is very strong considering the current backdrop. The management team cited some impact from the macroeconomic condition but I believe the headwind should ease and second-quarter results could come in much better than expectations.

Badri Kothandaraman, CEO, on US revenue

In the US, our revenue decreased 9% sequentially due to seasonality and macroeconomic conditions and increased 28% year-on-year.

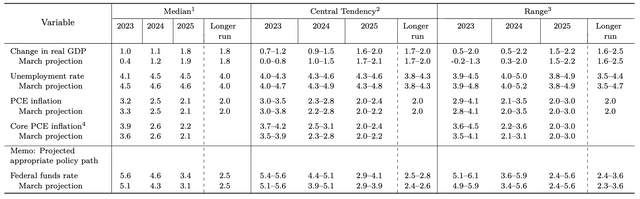

Besides the possibility of the management sandbagging, the economy is also holding up much better than most expected. Other than some risk-sensitive sectors such as financials and high-growth tech, most sectors have been doing well. In spite of the improving traction, the Federal Reserve raised its 2023 media GDP outlook from 0.4% in March to 1% in the recent meeting. The forecasted median unemployment rate for 2023 is also lowered from 4.5% to 4.1%, as shown in the chart below. I believe the strong resilience should provide meaningful support for Enphase demand.

Federal Reserve

Discounted Valuation

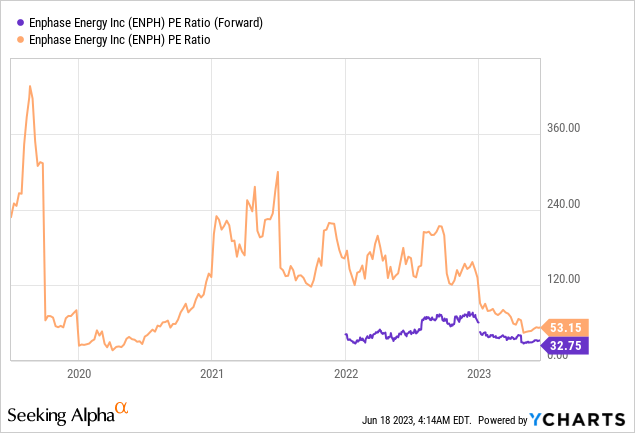

Enphase’s valuation has been hysteric for a long time but it is now looking a lot more reasonable and compelling. The company is currently trading at an fwd PE ratio of 32.8x, which is pretty discounted on a historical basis. As shown in the chart below, the current multiple represents a meaningful discount of 43.6% compared to its 5-year average fwd PE ratio of 58.2x.

While revenue growth is lower compared to the past few years, the estimated growth of 31% for FY23 is still vastly strong than most companies. This is not a direct comparison, but big tech companies like Microsoft (MSFT) and Netflix (NFLX) are both trading at a higher fwd PE ratio with estimated revenue growth of just single digits. This should give you a broad sense of how much discount Enphase is currently trading at.

Investor Takeaway

Energy Transition is one of the largest trends in this decade and the huge and rising investments demonstrate the optimism in this industry. I remain very confident in Enphase’s long-term outlook as the company is well-positioned to benefit from multiple tailwinds. The solar installation rate has been upbeat so far this year and should continue to increase as other states catch up on the transition. The costs and demand should also improve throughout the year thanks to easing inflation and favorable global policies.

Considering the stronger-than-expected economy, second-quarter results may also come in better than most expected. Despite the strong backdrop and prospects, shares continued to slide and the valuation is now meaningfully discounted on a historical basis. The huge pullback presents a compelling investing opportunity and I rate Enphase stock as a buy.

Read the full article here