Executive Summary

Throughout this report, it will become evident to investors why Upstart (NASDAQ:UPST) Holdings, Inc., a financial technology company, is a risky investment and why positive returns on its stock should no longer be expected. The company’s value proposition is centered around its AI technology; however, when comparing Upstart to FICO, it is evident that Upstart’s value proposition is inconsistent with its business model. Although Upstart claims to have superior technology, its core revenue relies on referral and platform fees, unlike FICO’s licensing-based revenue model. Furthermore, Upstart’s reliance on marketing and its user base as its main assets suggests that its technology is not the driving force behind its success. Insider trading lawsuits, along with questionable insider selling and related-party transactions, raise concerns about the integrity of the management team. Additionally, the company’s largest customer, Cross River Bank, faces potential failure, posing a significant risk to Upstart’s revenue and growth. Weak financial performance, a challenging economic environment, and an overvalued stock further contribute to the expected low positive returns. Investors should carefully stay away from Upstart.

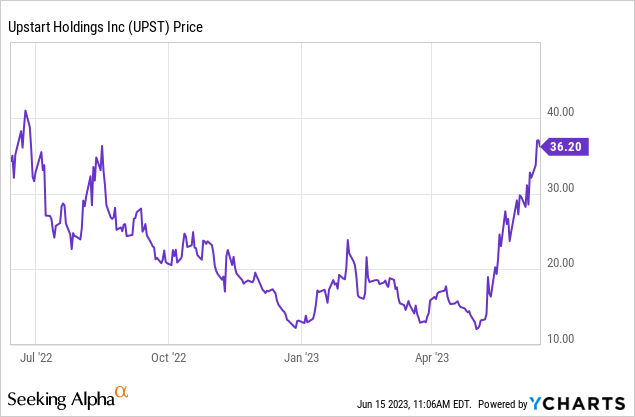

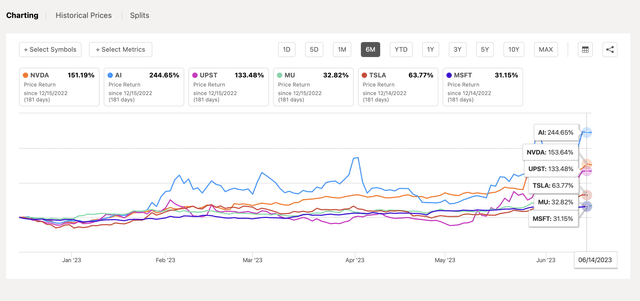

YCharts

Source: YCharts

Company History

Upstart Holdings, Inc. is a financial technology company founded in April 2012 by Dave Girouard, Paul Gu, and Anna Counselman. The company, headquartered in San Mateo, California, operates as an AI lending platform that collaborates with banks and credit unions to provide consumer loans using non-traditional variables for credit assessment. Initially, Upstart launched an Income Share Agreement product, allowing individuals to raise funds by sharing a percentage of their future income. However, in May 2014, the company shifted its focus towards the personal loan marketplace. Upstart offers both 3-year and 5-year loan products and utilizes an income and default prediction model that incorporates factors like education history, employment, and traditional underwriting criteria to assess creditworthiness. Over the years, Upstart has secured funding from various investors, including Google Ventures, Kleiner Perkins Caufield & Byers, and The Progressive Corporation. In late 2020, the company went public through an initial public offering (IPO).

Value Proposition and FICO Comparison: The Company’s True Asset isn’t its Technology

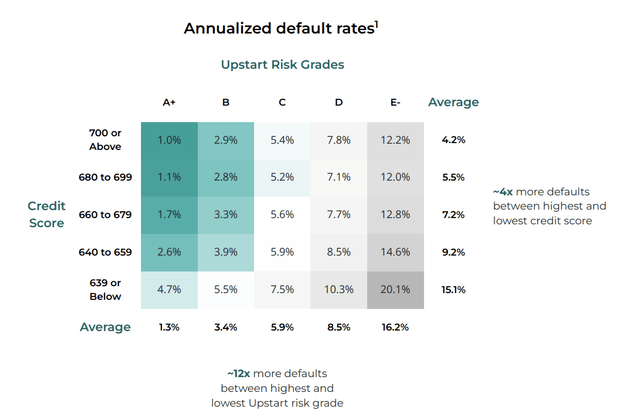

One of the equivocations regarding Upstart’s business model is its value proposition. I will reveal some of the inconsistencies between what most people believe to be Upstart’s value add and what I think the company’s value add truly is. Most people believe that Upstart is a leader in artificial intelligence and that they leverage AI technology to connect borrowers and lenders. To put it concisely, consumers get approved more easily, obtain a lower rate, and borrowers obtain a better risk/reward profile with their loan book. Upstart continuously proclaims that its technology is superior to competitors, notably Fair Isaac Corporation (FICO). Upstart is always sure to include this chart in its earnings presentations.

Q1

Source: Q1 Earnings Presentation

Upstart’s claim is that relative to Upstart’s credit checks, FICO’s credit checks lead to 12 times more defaults among the highest-risk lenders, and about 4 times more defaults among low-risk lenders. The purpose of the chart is to highlight the true value added from its AI services and to generate a narrative that the company is going to extract significant rents from FICO due to its superior technology.

Forbes

Forbes

Source: Forbes

I am of the opinion that the narrative of Upstart replacing the FICO score has inconsistencies with the company’s business model. Once these inconsistencies are further explored, one will realize that Upstart’s technology isn’t even their biggest asset and that their value adds are misrepresented. There are several distinctions between the two companies’ business models. Firstly, FICO’s revenue generation is significantly different from Upstart s. FICO’s core revenue stream comes from licensing its technology for scoring and credit solutions, whereas Upstart’s core revenue generation comes from net revenues encompassing referral and platform fees.

10-Q

Source: 10-Q

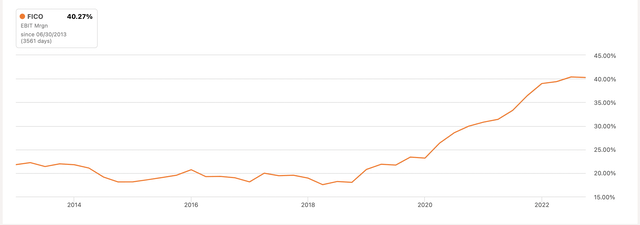

Secondly, FICO’s business model is much more attractive than Upstarts, which makes me question the company’s reasoning to launch a loan marketplace with its “superior” technology being the underpin. FICO has enjoyed 10 years of nearly 20% EBIT margins and even obtained a 40% EBIT margin last year. Additionally, FICO’s business model is much, much less cyclical than Upstart’s business because they don’t depend on loan growth, or highly liquid credit markets to get loans off its balance sheet.

Seeking Alpha

Source: Seeking Alpha

Finally, FICO doesn’t need to endure credit risk; whereas, Upstart not only has needed to endure credit risk, but has to pay banks a percentage of the loans that they keep on its balance sheet.

10-Q

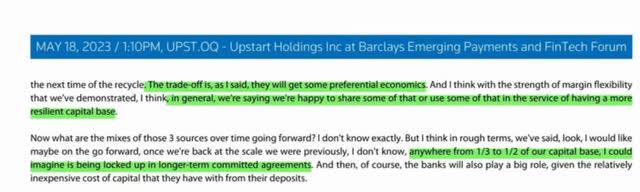

These incentives aren’t something that investors should expect to go away either; at Barclay’s FinTech forum Upstart’s CFO, Sanjay Datta, acknowledged that to secure more long-term funding partners, either loan originators or investors, they would need to offer “preferential economics”.

Source: Twitter

My main concern for investors pertains to the company’s inconsistencies regarding its value proposition and business model. Upstart claims its technology will replace a company such as FICO; however, Upstart needs to have much more skin in the game to attract and retain long-term customers. If Upstart’s technology is truly superior, it could have a recession-resilient business with high operating margins and be free of credit risk by simply licensing its technology to banks and credit unions. This leads me to believe that the company is overstating the capabilities of its technology and that it’s not the main asset driving the company’s core revenue. Instead, I believe that Upstart’s main value add is marketing and that their 2.6 million users are the company’s greatest asset. Upstart’s customer base provides regional banks and credit unions access to a pool of customers that otherwise might not have existed, enabling them to grow their loan books in exchange for a fee. Further, it provides hedge funds and investors the ability to purchase asset-backed securities with various risk pools that are tailored to varying levels of risk tolerance. Now Upstart bulls may point to the 4.9-star rating on Trust Pilot as proof that they have “superior” AI technology, but when looking at the reviews for FICO and lending marketplace company LendingClub (LC), Upstart doesn’t stand out.

Trust Pilot

Source: Trust Pilot

Featured Customers

Source: Featured Customers

Therefore, because the company oddly chose to be a finance company rather than a SaaS firm, and the reviews display that Upstart does not stand out in terms of service, I believe that the company doesn’t have any superior technology. Although being a conduit for banks and investors does add value in the marketplace, it is evident that artificial intelligence has been used as lipstick to drive Upstart’s returns in 2021, as well as the 100% jump we saw in May this year. Overall, I do not believe that Upstart will replace FICO, as its technology is not the pulse of its business.

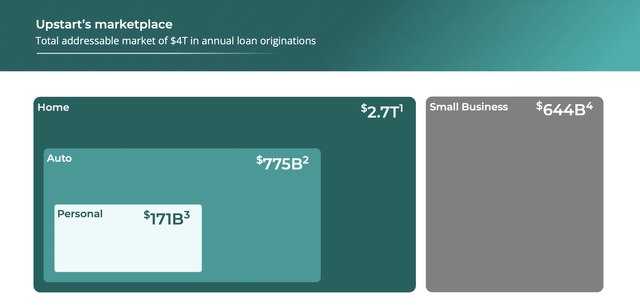

Misrepresenting Their Total Addressable Market

Technology and economic moat wouldn’t be the only misrepresentation that Upstart’s management team has made. The management team even exaggerates its total addressable market in its earnings presentations by claiming that its addressable consumer base is the gross loan value of all small business, personal, auto, and home loans outstanding.

Earnings Presentation

In actuality, because they are really a marketplace lender, their total addressable market is the aggregate transaction value generated by those networks. Statista provides a more accurate figure for Upstart’s total addressable market.

Statista

Source: Statista

As you can see, the $32 Billion-dollar gross transaction value is much, much smaller than the TAM management is proclaiming it can reach. Once again highlighting how the management team has misrepresented an important characteristic of its business.

Litigations and Insider Activity

Not only has Upstart utilized the AI narrative to create lipstick for its marketplace lending business, but there is reason to believe that the insiders were also pumping the share price to sell on the euphoria. The company’s executives and early investors have been facing several pending insider trading lawsuits.

10-Q

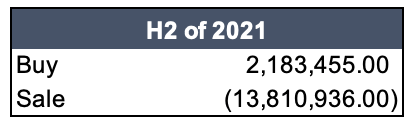

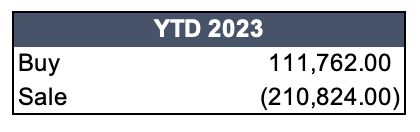

Let’s talk about the preliminary lawsuit filed against the senior executives and the hedge fund, Third Point. When assessing the company’s previous related-party transactions and insider selling near the 2021 highs, the discoveries raise some concerns. When excluding stock units RSUs, Upstart’s insiders sold around 14 million shares in H2 in 2021 when the stock was in the 300s.

Excel

Coincidentally, a prominent insider, Third Point, was buying a massive amount of the loans that originated on Upstart’s platform, particularly during the run-up in 2020 and 2021.

Proxy Statements

Source: Proxy Statement

Proxy Statement

And if you think the insider selling has stopped, once again, ironically during the company’s recent big pop in 2023, insider selling has been high, notably from CFO Sanjay Datta. Once again, the exhibit displays the total shares bought and sold, excluding the issuance of RSUs.

Excel

Considering I believe that the company has been utilizing AI as a lipstick to glamourize the company’s business model, the fact that heavy insider selling has occurred during large pops or multi-year highs, in addition to the heavy related-party transactions, I think that the plaintiffs have a valid case.

The Largest Customer is a Sketchy Bank

Upstart’s largest customer/loan originator is Cross River Bank which accounted for 30% of the company’s total revenue last quarter. In my opinion, this bank is bound to have no operations in the future. The bank grew out of nowhere during the creation of the PPP loans, they’ve depended on offshore crypto firms for growth which is now going into shambles, and they’ve been recently accused of fraud for its lending practices. The likely failure of Cross River Bank may materially impact the stock price of Upstart by potentially killing the recent positive sentiment surrounding the company, and the loss of a core customer will also put a knife in the growth endeavors of the business; considering the likelihood of the bank’s failure, this adds another risk for investors to consider.

Financial Position: Nothing to be Excited About

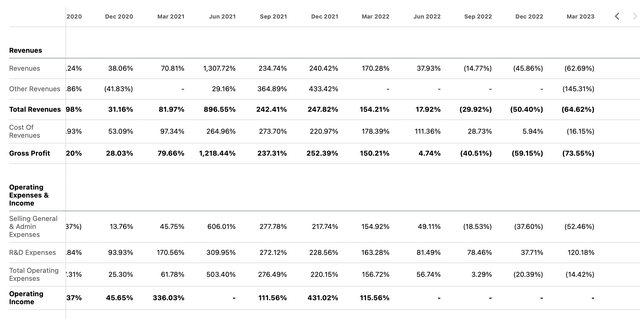

Upstart’s current financial position is definitely sub-optimal. Q1 revenues are down 62% QoQ, gross profit is down 74% QoQ, and the company isn’t even EBITDA positive anymore.

Seeking Alpha

Seeking Alpha

Source: Seeking Alpha

Additionally, the company also went through roughly 48% of its cash balance in the previous quarter. Also, with management mentioning “preferential economics” to secure funding partners, it’s likely that as Upstart continues to issue more loans, they’ll incur an increase in credit risk. Given the current state of the business, the interest rate environment, and the dire need to attract investors, I imagine that these incentives will begin to be fairly heavy. A perfect example is Castlelake agreeing to purchase up to $4 billion of installment loans from Upstart. My guess is that not only will a lot of these loans be sold at a discount, but there will likely be some sort of credit enhancement or other economic incentive attached that will make Upstart incur some credit risk for these loans. Therefore, Upstart will likely have a similar credit risk to what they’ve got now, only in the future it might be off-balance sheet. The one positive item regarding their financial position is that the management team announced that they secured $2 billion in much-needed funding to handle the economic headwinds. However, as explained in the valuation section, that is not why this stock is up so much in 2023.

The Economic Environment: Nothing to be Excited About

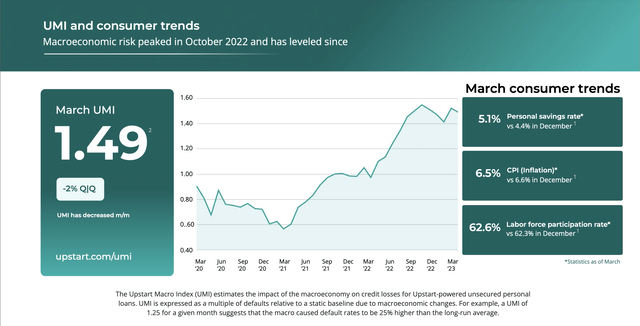

In Q1, Upstart claimed in their earnings presentation slide deck that economic risk had peaked in October 2022.

Earnings Presentation

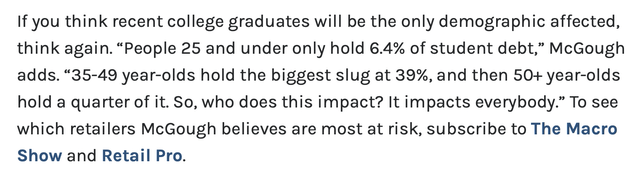

However, investors should remain vigilant as student loan repayments restart in July. The relief provided by student loan forgiveness will serve greater than most think as the majority of student loan debt outstanding is held by the United States’ core consumer base. An excerpt by Brian McGough over at Hedgeye broke this down.

Hedgeye

Source: Hedgeye

Between no more debt relief and continued lagged impacts from the Fed’s rate hikes, I think the U.S. consumer will continue to struggle, creating yet another risk variable for investors in Upstart to consider.

Valuation

To determine Upstart’s valuation, we must determine what caused such an upswing in its share price in 2023. Unlike most people, I do not think that the announcement of Castlelake’s loan purchases or the $2 billion in funding has been the driver of the stock’s performance. Instead, the stock has benefited from a positive narrative through generative AI, enabling a euphoria that’s causing shorts to cover. When looking at the returns of other AI stocks, we see that Upstart has been a constituent among a group of companies benefiting from the AI euphoria.

Seeking Alpha

However, as mentioned before, I not only think that Upstart’s technology isn’t its greatest asset, but that it’s been used as lipstick for investors. Further, considering that a closer peer like LendingClub is sitting at a $1 billion valuation, all of the risks associated with the economics, the integrity of the management team, and their customer concentration, Upstart’s intrinsic value is likely around its book value of $7.59 per share. This leaves me with the consensus that Upstart is egregiously overpriced.

Final Thoughts

Upstart is a perfect example that you shouldn’t take management’s word at face value. It is evident that AI has been used as a lipstick to generate a positive narrative for the stock, as there is no proof outside of the management’s word that their technology is superior. Also, the management has been faced with several lawsuits related to insider trading, which should make us question the integrity of what they’re proclaiming. Finally, between the company’s questionable customer base, a distraught American consumer, the need to increase its own credit risk to obtain customers, and the company’s depleting financial position, my intrinsic value estimate for Upstart is around book value at $7.59 per share, which is much below the current market price of $37. For these reasons, I think investors are much better off staying away, rather than playing gambler’s fallacy.

Read the full article here