WTI Oil prices have been trading around $70 per barrel, which is about 50 dollars less than the August 2022 peak achieved largely on the back of the Ukrainian conflict. Now to profit from such a decline, you have ETFs that essentially make use of the downside in oil prices like the ProShares UltraShort Bloomberg Crude Oil ETF (NYSEARCA:SCO) which I covered on December 2 last year.

At that time, I had a hold position as the time window to make money by being long had elapsed and the subsequent price action proved me right as the ETF plunged by over 20% over one week. My aim with this publication is to assess for another trading opportunity, but this time, through shorting, following announcements made by the joint ministerial OPEC+ meeting on June 4 about a one million bpd (barrel per day) production cut.

The Price Action Since December 2 (www.seekingalpha.com)

For this purpose, I first walk investors through the risks involved in leveraged ETFs before touching upon related supply and demand parameters.

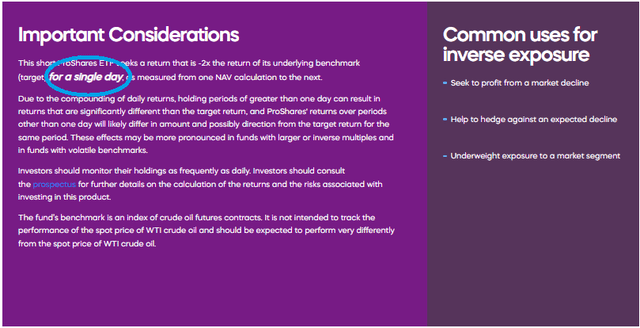

The Risks Posed by Leveraged ETFs

First, a conventional ETF is an index fund that is listed on an exchange and replicates a stock market index. In contrast, a leveraged ETF amplifies the variations of its benchmark index in order to multiply its gains. Thus, especially those who are adept at the buy-and-hold approach to investing in funds are cautioned as to the risks in putting money into SCO. This is also highlighted by the Securities and Exchange Commission.

Another difference is that while a traditional ETF invests in the stocks of the underlying index, a leveraged one like SCO uses derivatives to achieve the same result, namely futures. In this respect, the key thing to note is that the leverage effect is on a day-to-day basis, in turn implying that it is the daily performance that is multiplied by two. This is the reason the issuers insist investors should check returns on a daily basis and not over the long term.

Important Info (www.proshares.com)

The compounding effect explains this.

This is related to the daily price fluctuations and the more these vary during the trading period, the more compounding eats away at the gains. Moreover, the higher the degree of leverage the more can be losses, and for this purpose, SCO is a two times (2x) inverse leveraged ETF, whose fund managers charge fees of 0.95%.

Consequently, the ETF has a multiplier effect whereby when the Bloomberg Commodity Balanced WTI Crude Oil Index drops by 1%, gains of two times or 2% can be obtained, but, the compounding effect can also mitigate these. For example, instead of yielding 2%, one can end up only with only 1.5% or even less. Worst, any unanticipated market move as is often the case for commodities can easily destroy your gains due to the multiplier effect working against you.

This is the reason why in order to trade leveraged ETF, it is important to first carefully study the price action while also considering supply and demand factors in order to maximize the possibility of not losing money. For this matter, we can learn a lot from the OPEC+ which is the Organization of Petroleum Exporting Countries comprising 13 members enlarged to accommodate other partners notably Russia.

Dissecting OPEC+’s Move

Thus, coming back to the meeting, the production cut will be a voluntary one by the Saudis and will come into effect in July. This adds to the 3.66 million bpd agreed in 2022 and last April, which has been extended to the end of 2024 from 2023. Additionally, for Russia which remains desperate for oil revenues to finance its presence in Ukraine, its production target remains unchanged.

Learning from the OPEC alliance’s April meeting, when there was a decision to voluntarily reduce production by 1.66 million bpd until December next, this only resulted in an ephemerous upside in WTI, to the $82 level before prices fell again to around $68. This short-lived recovery in oil prices came amid fears of a global economic recession, rising rates from major central banks, and a slower-than-expected recovery in demand in China coming out of Covid restrictions.

Moreover, there have been earlier signs of discord, between the world’s major oil producers, Saudi Arabia and Russia. Thus, far from honoring an earlier commitment to cut its production from 500,000 barrels per day, Russia has supplied Asian markets including major markets such as India and China. Now, the country eventually decided to comply with the cut by the end of this year, but this still needs to be verified. Now the fact that Russia is only second to Saudi Arabia in terms of production and may not be strongly committed to timely cuts somewhat weakens OPEC+’s position, and, instead of weakening it further, it seems that the Saudis have opted for a voluntary production cut.

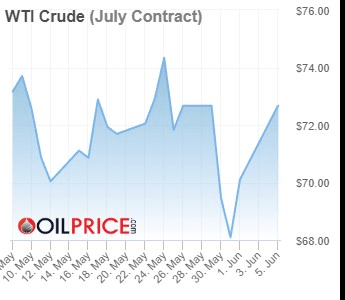

This caused WTI to temporarily spike to the $73.98 level before retrenching back to around $72.5 at the time of writing, or a brief upside. Also, unlike the above $10 upside seen in early April when going into the meeting, there has only been a $7 rise since the beginning of June.

WTI Crude oil spot price (oilprice.com)

However, this upside does have the potential to be sustained in the medium term as the Saudis have both the willingness and the spare capacity together with the storage that goes along with it to cut production, which should translate into less supply reaching the oil markets. Now, coupled with this, there are demand-related factors that are favorable to higher prices including the agreement on the debt ceiling after weeks of heated negotiations thereby removing the threat of a U.S. default. Along the same lines, a pause by the Federal Reserve in terms of monetary policy action may also support prices as it favors business appetite for risk-taking across the board.

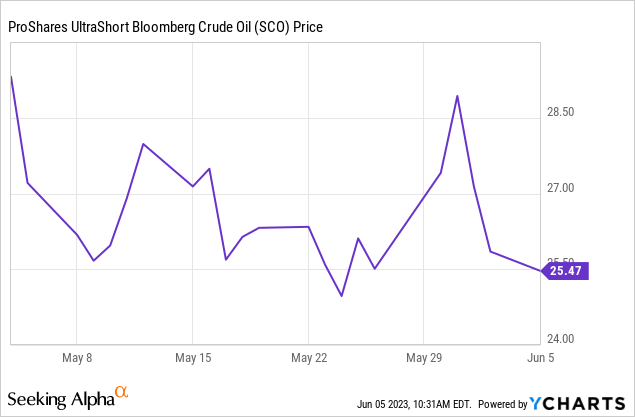

SCO’s Price Action and Demand/Supply

Looking at the price action, the OPEC+ move has caused SCO to drop by about $3 at the time of writing. However, do bear in mind that the ETF’s share price does not follow the spot price of WTI crude oil as it tracks an index composed of crude oil futures contracts. Still, there is a degree of inverse correlation whereby when oil prices rise, SCO suffers as shown by the latest drop to $25.47.

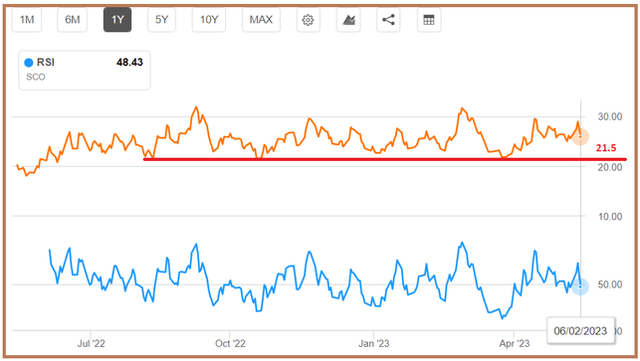

Now, with SA’s Quant ratings pointing to a “Sell”, it appears that the price could drop further, but, most of the price action with respect to the OPEC+ meeting seems to have been priced in by the market, with the RSI of 48.43 (chart below) also not indicating an overbought condition yet. This position is further supported by the fact that it looks like the Saudis have attempted to put a floor underneath the price, instead of boosting it as would have been the case if other members had announced cuts.

However, in the medium term, the ETF’s value is likely to drop below $21.5, a support level it has reached three times in the last year as shown by the red line below.

Chart showing Support Level and RSI (www.seekingalpha.com)

The reason for this is oil futures contracts for March 2024 trading lower than those for July 2023 by $2.52 which is synonymous with a phenomenon called backwardation. This shows that less oil is being stored in commercial storage facilities probably because of the high cost of capital and that the oil market is primarily functioning according to demand-supply dynamics. Hence, possibly fearing a supply-related problem, traders are willing to pay more for the commodity now than waiting in the future to place their contracts. This problem is confirmed by a decline in drilling rigs, by 15 to 555, or the largest since September 2021, favoring a reduction in supply. This in turn means higher prices and may seem to justify shorting SCO.

No immediate Trading Opportunity, but there is More

Additionally, data by the International Energy Agency released in May mention that current oil prices simply do not reflect the crisis markets will face in the future and is “at odds” with the tighter conditions expected in the second half of this year. As a result, the agency has raised its forecast for global oil demand for 2023 by 200K barrels per day to a record high of 102 million, which also is up from last month’s estimate. This rise also takes into account China’s economic recovery and purchase of 3 million barrels of crude oil for the American Strategic Petroleum Reserves.

Therefore, prices are likely to rise which means that the opportunity to short SCO is there, but, it is also important to also get the timing right, which is not the case right now as the rise in oil prices caused by OPEC+ is not likely to be sustained in the immediate term. Thus, for those who did not short SCO prior to the meeting, it is probably too late. Also, as mentioned earlier, momentum indicators are not favorable which means that those who are invested may have to wait for longer to pocket expected gains. In this connection, the longer they wait more can be lost to the compounding effect.

Now, this value erosion (or decay or beta slippage) which becomes evident when you check SCO’s 5-year performance, can be used to short the ETF as part of a tactical trade, possibly as part of a hedging strategy. The advantage here is that the 0.95% fee charged by ProShares is less than the borrowing cost which can exceed 3% for short-selling the shares of a security directly and on top does not require the holding of a margin account.

Alternatively, instead of shorting SCO, one can also invest through more conventional buy-and-hold funds like Energy Select Sector SPDR Fund ETF (XLE) due to take advantage of oil’s longer-term prospects. Still, investors are cautioned that a lot will depend on Russia, and with no signs of the Ukrainian conflict ending, the production cuts planned by OPEC+ could be partially offset by more exports to China and India.

Finally, for oil bears looking to make money through short, in the absence of any major catalysts, the best time to place bets is next week as the Fed interest rate actions unravel and weaker PMI services data increase the likelihood of a pause.

Read the full article here