The Global X Lithium & Battery Tech ETF (NYSEARCA:LIT) provides investors with exposure to the whole EV supply chain, from the mine mouth all the way to the end of the assembly line. LIT offers a good alternative for investors who may want exposure to the EV supply chain but who may not want the risk that comes from owning individual stocks. And the ETF has shown some impressive returns, climbing over 84% in the past five years.

However, the EV supply chain has taken some hits over the course of the last year. Lithium prices are down substantially and even mighty Tesla, Inc. (TSLA) has seen its stock price drop sharply from previous highs. The price drop may look like an opportunity, but there are a number of factors that may weigh down EV sales and lithium prices over the course of this year. In this article, we’ll review LIT and discuss those factors.

ETF Background

Global X bills its Lithium and Battery Tech ETF as providing exposure to “the full lithium cycle, from mining and refining the metal through battery production.” However, the ETF, which seeks to provide returns similar to that of the Solactive Global Lithium Index, does much more than that. By holding positions in major EV producers such as BYD Company Limited (OTCPK:BYDDF), Tesla, and Rivian Automotive Inc. (RIVN), among others, it extends that exposure to the whole EV supply chain.

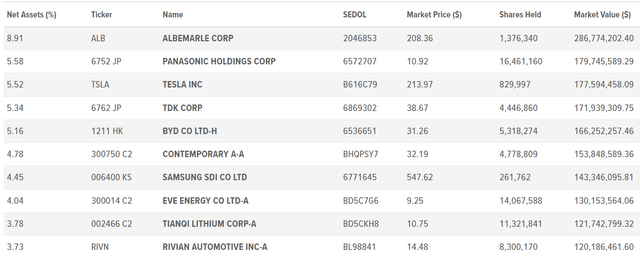

LIT Top 10 Holdings (globalxetfs.com)

One obvious advantage of taking such a broad stroke approach is that it provides investors looking to bet on the EV thesis a one-stop shop. An individual who foresees liquidity continuing to flow into battery metals as well as the stocks of EV and battery producers over the long term can benefit from this trend by simply buying and holding the fund. However, such investors should also bear in mind its 0.75% total expense ratio.

A Broad Mandate

But there are also some possible disadvantages of LIT’s approach. Having such a broad mandate and holding stocks in such disparate industries such as mining, battery production, and vehicle assembly may prevent investors from taking advantage of liquidity flows between the sectors that comprise the EV supply chain.

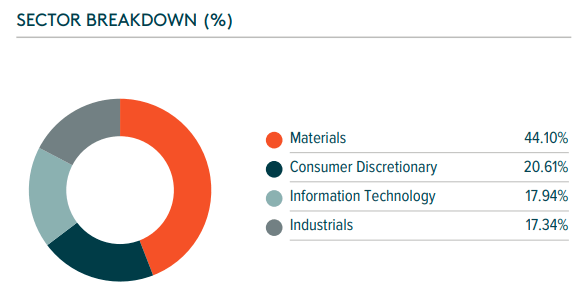

LIT Sector Breakdown (globalxetfs.com)

That’s because, while it’s true that increased liquidity flows into the EV sector as a whole will eventually lift all boats, there is a certain zero-sum dynamic between the commodity producers that supply the sector and the manufacturers that build and assemble its products; this is common in many goods producing industries.

If lithium prices remain elevated for an extended period, as occurred during most of last year, then a greater portion of total revenue flowing into the EV sector will go to lithium miners and a corresponding smaller portion will go to battery and EV producers. Of course, the reverse is also true, a long run of depressed lithium prices will squeeze upstream producers and benefit downstream OEMs. The OEMs can raise prices, but that will eventually become a drag on sales.

LIT’s broad-based approach helps neutralize some of this intra-industry risk. This method should help smooth returns over the long term by reducing the impact of commodity price changes on the overall portfolio; although, that is something about which investors looking to bet on rising lithium prices should be cognizant.

China Weakness

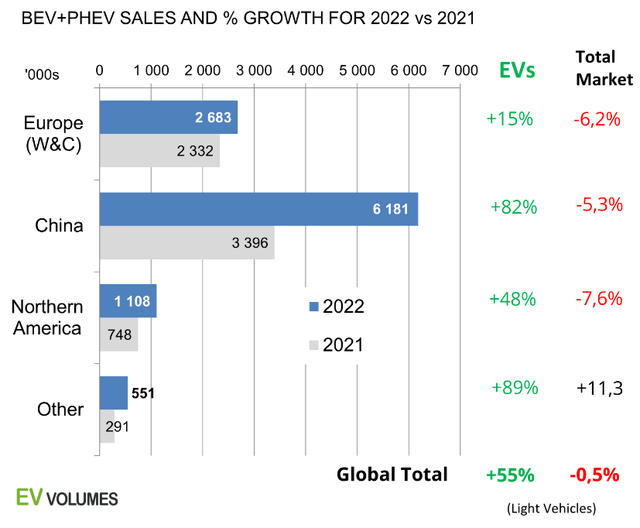

Currently much of the EV supply chain is dependent on the Chinese economy. As seen in the exhibit below, both overall sales numbers as well as growth rates in the Chinese market continue to outpace those of other regions.

ev-volumes.com

And EV sales in China have continued to show decent numbers during the first four months of the year. Plugin vehicles now have a 35% market share and over 1.9 million units moved during the January-April period. However, there are some growing risks on the horizon.

China’s real estate market continues its slow-motion implosion. A crisis that ostensibly began with the collapse of the China Evergrande Group (OTC:EGRNF) in 2021 was, in reality, building up for much of the last decade as Chinese real estate developers constructed millions of unnecessary housing units. The fact that the country’s population has also begun to shrink will not help in resolving the problem either.

Takeaway

One can easily foresee a continued decline in Chinese real estate prices given the initial huge overbuild and China’s discouraging demographic picture. And like most Americans, Chinese individuals have most of their wealth tied up in residential real estate; therefore, a continued fall in real estate prices could eventually have a substantial impact on global EV sales. Such an occurrence would filter down through the whole EV supply chain and given the fact that China is currently the center of the EV universe, it could mean that the Global X Lithium & Battery Tech ETF will remain at depressed valuations for months to come.

Read the full article here