Owl Rock Capital Corporation (NYSE:ORCC) and VICI Properties Inc. (NYSE:VICI) are relative newcomers to their respective industries.

ORCC’s IPO occurred in July of 2019, yet it is recognized as one of the top tier Business Development Companies (BDCs). Although shares are closing in on the stock’s 52-week high, ORCC still trades well below the valuations recorded during much of 2021 and the first few months of 2022.

VICI was spawned by the Chapter 11 bankruptcy reorganization of Caesars Entertainment Operating Company in 2017. Like ORCC, shares of VICI are underperforming with the stock’s price down nearly 4% year-to-date.

Since the IPO, VICI’s management has worked to diversify the company in more than one respect. From an upstart to the best performing REIT in the S&P 500 last year, those efforts have served investors well.

With yields over 5% and positive prospects, I see both stocks as solid investment.

VICI Properties (VICI)

When VICI was formed, the REIT had a single customer…Caesars. Since then, VICI has transformed into a reasonably well diversified business. Today, the firm has 50 properties and eleven tenants. Those properties are spread across fifteen states and a Canadian province.

Furthermore, nearly half of VICI’s current properties are in regional markets. Regional operators tend to suffer less severe downturns associated with macroeconomic headwinds.

To achieve the desired diversification, VICI went on a spending spree. Recent acquisitions include the February 2022 purchase of the land and real estate assets of Venetian Resort Las Vegas for $4 billion. That was followed in April by the acquisition of MGM Growth Properties, a casino centered REIT, in a deal valued at $17.2.

Early this year, VICI acquired the remaining 49.9% interest in the MGM Grand/Mandalay Bay joint venture for $1.3 billion in cash along with the assumption of $3 billion in property-level debt. And in its first expansion outside the U.S. the REIT acquired four casinos from PURE Canadian Gaming for $200.8 million.

The growing list of tenants and properties also resulted in a surge in revenues. As of the end of Q1 ’23, total revenues are up nearly 111%, adjusted FFO has increased 73% and FFO per share has grown by 18.6% over the comparable quarter.

Astute investors might be concerned that VICI’s land grabs resulted in a debt burden. Rest assured that isn’t the case. Last year the REIT received investment grade credit ratings from S&P and Fitch.

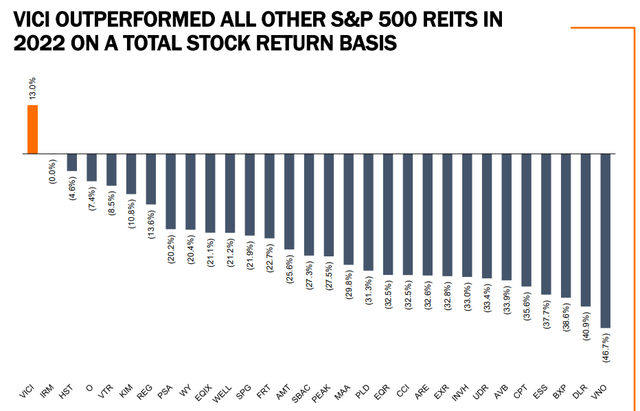

VICI is the only REIT listed on the S&P 500 that beat the index in 2022.

VICI Investor Presentation

It is difficult to imagine a business with a safer revenue stream than that possessed by VICI.

The average remaining lease term is 42 years as of March of 2023, and the REIT collected 100% of rents since the stock’s IPO.

In 2023, 50% of leases have CPI escalators, and over the long-term, 96% of leases have CPI escalators. Furthermore, 76% of the rent rolls are from tenants listed in the S&P 500.

The REIT’s debt ladder is well staggered with no debt due in 2023.

The gaming regulatory environment creates high barriers to entry.

Management has a stated goal of delivering an annual total return of 10% to 12%.

Owl Rock Capital Corporation (ORCC)

ORCC is a business development corporation (BDC). BDCs make loans to and invest in small and mid-sized businesses. By law, at least 70% of a BDC’s assets must be invested in nonpublic US companies with market values of less than $250 million.

A minimum of 90% of a BDC’s income is distributed to investors. That distribution generally results in a rather high yield. Consequently, investors unfamiliar with the business model may view BDCs as having “sucker yields.” However, for those with knowledge of BDCs, history shows top notch business development corporations weather recessions and bear markets well.

Case in point: there are two BDCs I rate as leaders of the pack, Main Street Capital (MAIN) and Ares Capital (ARCC). MAIN has never reduced the dividend payout.

Shortly after the firm’s IPO in 2007, MAIN initiated a monthly dividend of $0.13 a share.

Today MAIN pays a monthly dividend of $0.23 a share, and the company issued two special dividends in 2023. The first was $0.18 in March and the second was $0.23 in June.

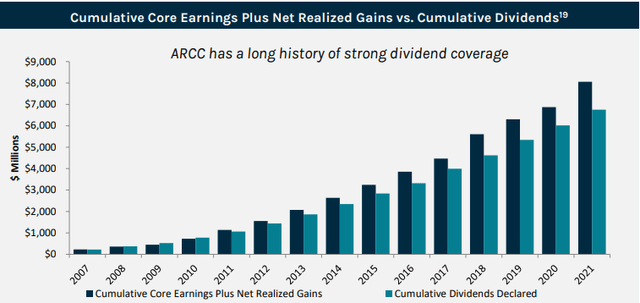

However, ARCC did cut the dividend during the Great Recession. In the middle of 2009, the base quarterly dividend of $0.42 was reduced to $0.35, but the share price had fallen so that the stock was yielding over 18% after the dividend cut was in place.

ORCC Investor Presentation

Unlike MAIN and ARCC, ORCC’s history does not include the Great Recession. Even so, we have the COVID bear market to draw from to evaluate the stock’s dividend history.

Not only was the dividend maintained during the COVID inspired bear market, management also funded a share repurchase program to buy back stock at a steep discount to NAV.

Despite the macroeconomic headwinds in place during that time frame, Owl Rock had zero non-accruals. That speaks volumes regarding the quality of ORCC’s portfolio.

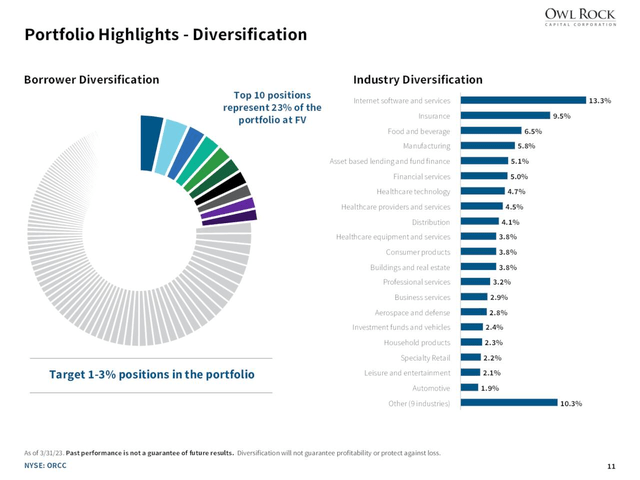

Some of that strength is related to ORCC having a wide range of diversification among both the companies and industries that constitute its portfolio.

ORCC Investor Presentation

ORCC also mitigates risk in that 71% of loans are first-lien. Should a firm with a first-lien loan declare bankruptcy, ORCC would have first claims on that company’s assets. In most cases, that also includes intangible assets such as trademarks.

Since its IPO, ORCC has had a 4 basis point (0.14%) annualized loss ratio. On the last earnings call, management noted there were only two loans on nonaccrual status at the end of the quarter.

Owl Rock is also one of a select group of BDCs with investment grade credit ratings.

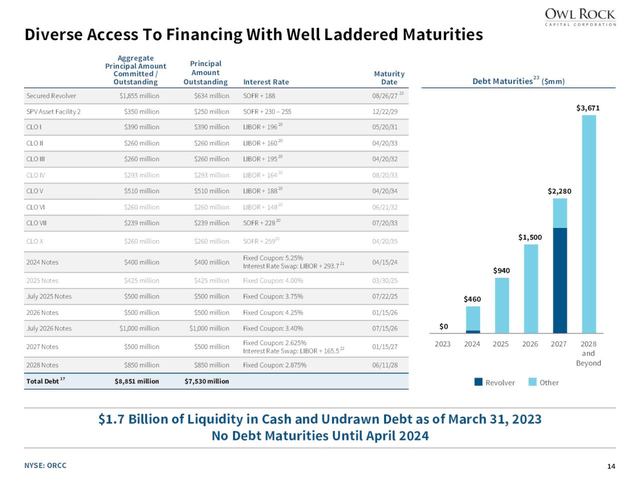

ORCC has 60 unique finance partners across the firm’s secured facilities. Weighted average cost of debt 5.2%, and there are no near-term maturities.

Financing chart (ORCC Investor Presentation)

Another positive for investors is that insiders hold relatively large positions in the company. Insider holdings tend to constitute a low double digit percentage of the float.

I’ve seen significant discussion among pundits regarding the possibility that the current banking malaise could provide opportunities for BDCs. During the Q1 earnings call, management answered an analyst’s question on the topic. The response indicated ORCC does not expect a significant opportunity to emerge from the banking crisis.

The following two comments provide insights as to management’s view of the current business environment.

…we continue to expect and are prepared for more challenging conditions in the back half of the year. Like many in the market, we have been anticipating a shift in consumer demand on the back of the higher rate environment and a subsequent contraction in the economy. We remain vigilant and are proactively analyzing our portfolio. Craig Packer, CFO & COO

…we like recession-resistant sectors. We like businesses that have annuity-like cash flows. We like businesses backed by private equity in a significant way. And our biggest sectors, software, insurance, health care, food and beverage, have been our biggest sectors every quarter since we started and it’s served us well, and it’s put us in a great spot in a potentially weakened economy to outperform. Craig Packer, CFO & COO

Management also stated, “we should have very strong earnings this year and next year.”

ORCC notched a new record quarterly NII for the company. Management expects to deliver ROE in excess of 12% for the fiscal year based on the current outlook for rates and credit performance.

Summation

I consider VICI and ORCC to rank among the best investments in their respective industries. Shares of VICI are trading well below that stock’s 52-week highs while ORCC’s is trading at virtually the same share price seen in June of 2022.

While BDCs provide high yields, there are risks related to this industry in the form of sensitivity to interest rates and macroeconomic events. However, in the past, the market has grossly overreacted to BDCs’ prospects during recessions, often giving investors an excellent opportunity to invest in leaders like ARCC, MOAT and now ORCC at bargain basement valuations.

While we are not experiencing that type of opportunity today, ORCC is trading a bit below net asset value. Meanwhile, a number of the firm’s rivals are trading at or above NAV.

I rate both stocks as BUYS.

I added to each position the day I submitted this article.

Read the full article here