Investment thesis

International Business Machines Corporation (NYSE:IBM) is a dividend champion with a fascinating history in general and over the past decade especially. The company experienced secular shifts and was forced to change to deal with declining financials. I consider that the company succeeded in facing massive restructuring, and its cash flow metrics are still stellar. The dividend yield together with valuation looks attractive to me.

Company information

IBM is a leading U.S.-based enterprise IT hardware, software, and services provider. The company has a vibrant history tracing back to 1911.

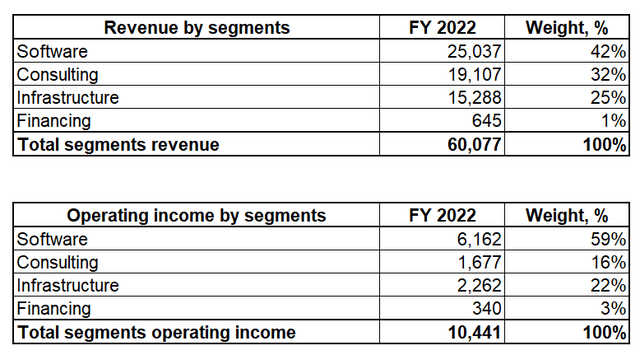

The company’s fiscal year ends on December 31. The company has been restructuring its business over the past several years to address changing technological environment. To align with the new structure, the company has revised its segment reporting into four major categories: Software, Consulting Infrastructure, and Financing.

Compiled by the author based on the latest IBM 10-K

Financials

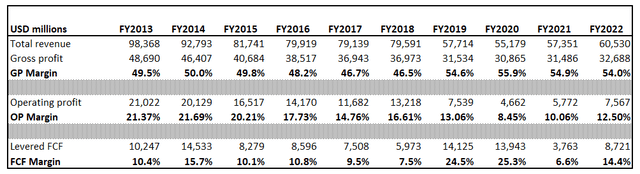

If we look at the company’s financials over the past decade, we can see that the company has been changing its business significantly to survive in the changing technological environment.

Author’s calculations

The company’s revenues were declining substantially between FY 2013 and FY 2020 due to a secular decline in traditional business which significantly decreased demand for mainframes and servers. The industry faced technological disruptions that changed the overall business landscape of IBM. Increased adoption of cloud computing, mobile devices, and data analytics made legacy hardware look like a dinosaur. IBM had to adapt to the changing market dynamics and transform its products and services to be cloud-compatible. This transition involved significant investments in cloud infrastructure and services, impacting the company’s financial performance in the short term.

As we can see from the financial dynamics over the past three years, we can see that the company succeeded in the transformation. I consider it to be successful because of the expanded gross margin over the decade and the operating margin turning back to double-digits from the 8.5% bottom in FY 2020.

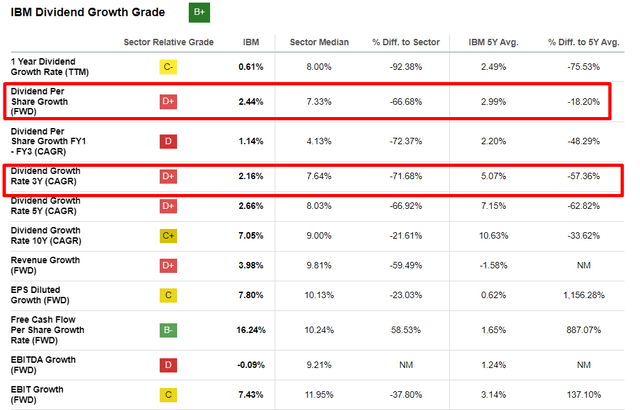

What I also like about IBM’s financial performance is its exceptional free cash flow [FCF] margins which the company managed to sustain regardless of the very harsh secular headwinds it faced. For me, it is a solid quality sign of the management, which allowed the company to demonstrate an A+ dividend consistency over the past quarter century.

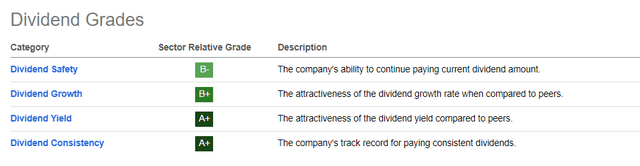

Seeking Alpha

Apart from strong dividend consistency, Seeking Alpha Quant assigns IBM stock the highest possible dividend yield grade of “A+”, and I agree with it because the company’s current forward dividend yield is above 5% which I consider attractive, especially in the current environment where inflation dipped below 5% and is on the path to its historical averages.

Seeking Alpha

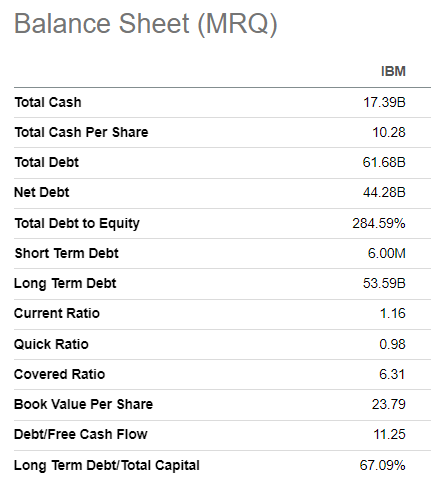

I consider IBM’s financial position as strong as well. Liquidity looks sound and the outstanding cash of $17 billion also indicates that the balance sheet is in good shape. Critics might argue that the total debt-to-equity ratio of about 300% is a red flag, but I do not think so since the company’s debt has been historically much higher than both equity and cash due to the capital allocation strategy. So, I do not see high risks in substantial debt amounts. The major part of the debt is long-term, so I see low risks here.

Seeking Alpha

The company reported its Q1 FY 2023 earnings on April 19, slightly missing on the topline but beating consensus estimates for the EPS. GAAP revenue was flat on a YoY basis. In constant currency and adjusted for M&A, revenue rose 4% year-over-year. IBM’s business is highly seasonal so I do not compare QoQ here. The non-GAAP gross margin was 53.7% in Q1 FY 2023 versus 52.9% a year earlier.

I would like to underline two factors I like in the current challenging and uncertain environment. First, IBM has minimal exposure or manufacturing presence in China which is good given rising geopolitical tensions between the world’s two biggest economies. Second, IBM is focused on the enterprise market, while many other technology companies rely on consumer business and are currently vulnerable to the softening demand for personal electronics devices.

Overall, I believe that IBM’s financial performance is strong, and the company is well-positioned to weather potential storm.

Valuation

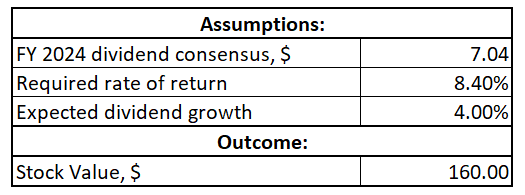

As seen in the “Financials” section, IBM has consistently paid out dividends to its shareholders. Therefore, I have one more option other than discounted cash flows [DCF] for valuation. Let me start with the dividend discount model [DDM]. To start with underlying assumptions, let me determine the discount rate first. I consider 8.4% WACC which is provided by valueinvesting.io to be reasonable. I also have dividend consensus estimates projected at $7.04 per share in FY 2024. For dividend growth, I take the average between the historical 5-year average forward dividend growth rate and 3Y CAGR, which is 4% if rounded.

Seeking Alpha

Incorporating all the above assumptions into the DDM formula gives me a fair share price of $160, 24% higher than the current stock price. Looks attractive to me but let me cross-check with the DCF approach.

Author’s calculation

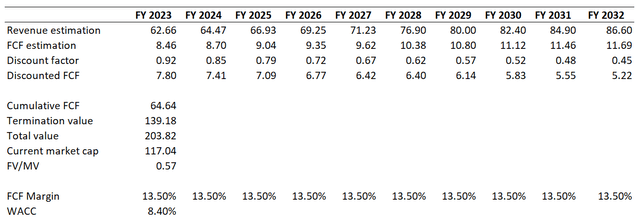

The discount rate would be the same as I used for the DDM approach. For future revenues, I use consensus earnings estimates, the revenue is expected to grow at about 3% CAGR which I consider modest. For the FCF margin, I prefer to be conservative and use the average for the last decade, which was at 13.5% with SBC deducted.

Author’s calculations

As you can see from the above spreadsheet, the company’s fair business value is substantially higher than the current market cap. Actually, it is about 2 times higher than the market cap, indicating massive undervaluation.

To conclude, I think that IBM is very attractively valued at current levels. If we add up about 5% dividend yield, I believe that the stock can be a compelling investment opportunity, but before we make a final decision let me discuss significant risks in the next section.

Risks to consider

As a technology company, IBM faces fierce competition and high technological disruption risks. IBM must actively monitor industry trends, invest in cutting-edge technologies, and foster a culture of innovation to navigate these challenges successfully. On the other hand, based on the history of overcoming secularly unfavorable shifts for IBM over the past decade, we can conclude that the management is strong in innovating and reorganizing.

As I mentioned in the “Financial” section, IBM’s business is well-positioned in the current challenging environment. But the recession and credit crunch are still looming, and it will highly likely affect all stock prices to go down if the worst scenarios unfold. Therefore, there is a risk of an overall stock market downturn, and IBM is highly likely to follow the same direction.

Bottom line

Overall, I believe that IBM stock looks like an attractive investment opportunity. Despite the high risks of the potential overall market downturn, I consider IBM as a solid long-term bet given its attractive valuation and high dividend yield. I assign IBM stock a buy rating because I believe that the benefits outweigh the risks here.

Read the full article here