Recap

Cathie Wood, renowned investor and founder of ARK Invest, made a significant move in the first quarter of 2023 by completely divesting all her positions in Farfetch Limited (NYSE:FTCH). In a dramatic turn, Farfetch stock surged by 30% following the Q1 2023 earnings release.

Farfetch, a prominent player in the e-commerce industry, had set ambitious targets for its growth in 2023. The company aimed to achieve a 16% increase in GMV and a substantial 31% rise in revenues. Moreover, Farfetch had plans to enhance its operational efficiency by boosting the EBITDA margin by 6-9% throughout the year.

Considering these developments, investors now face a crucial decision: whether to buy or sell Farfetch stocks. On the one hand, Cathie Wood’s decision to divest her positions may raise concerns and warrant caution. However, the subsequent surge in the stock price following the impressive earnings release suggests that market sentiment is currently positive.

Unraveling complexity: the business model

We have compiled a list of four companies that can be compared to Farfetch, as we believe this will provide a clearer understanding of Farfetch’s business model.

| Platform | Business model | Unique Features |

|---|---|---|

| Farfetch | Brands and marketplace | Global network of boutiques and brands, logistics support |

| YNAP | Brands and marketplace | Curated luxury shopping experience, personal shopping services |

|

Etsy (ETSY) |

Marketplace | Marketplace for unique and creative goods, strong community engagement |

|

The RealReal (REAL) |

Marketplace | Authentication process for all items, physical stores in addition to online platform |

|

Revolve (RVLV) |

Brands | Extensive range of brands, influencer collaborations, and strong social media presence |

YNAP’s luxury marketplace

Firstly, let’s consider YNAP (Yoox Net-a-Porter Group). Farfetch has a third-party marketplace business similar to YNAP to serve consumers and luxury brands. However, the online luxury marketplace platform may not be optimal for luxury brands. Brands often face a challenge when it comes to exerting complete control over the presentation of their products on third-party platforms. This lack of control can be a significant concern for brands seeking to maintain a consistent and high-quality brand image. Richemont, a luxury goods conglomerate (OTCPK:CFRHF), recognized this issue and saw it as a compelling reason to acquire YNAP. This acquisition provided Richemont with a higher degree of influence over how its products were presented, ensuring that they received the attention and presentation they deserved.

In a similar vein, Farfetch acquired the New Guard Group, aiming to achieve a similar purpose. However, the moment Farfetch decided to acquire the New Guard Group, it became evident that Farfetch would face challenges in establishing meaningful partnerships with other top-tier luxury brands due to potential conflicts of interest.

In August 2022, Farfetch made a strategic move by acquiring a 47% stake in YNAP with a call/put option that provides potential for Farfetch to increase its ownership stake in the future. It’s important to note that this deal could potentially result in a 15% dilution of Farfetch stock, as it’s a stock transaction.

From a shareholder perspective, we view this acquisition as less favorable. It is unlikely to significantly enhance Farfetch’s bargaining power with luxury brands as there are only 4 million users on YNAP’s platform, and the stock dilution can prove costly for existing shareholders.

We believe that Farfetch will eventually put less emphasis on growing the marketplace platform and more effort into building its private brand or focusing on a particular luxury market, despite its aim to do so.

Etsy’s small business marketplace

The aim of Farfetch is to link consumers, curators, and creators. Small and independent brands use Farfetch to market their goods to consumers. In this market, it competes with Etsy. Along with major labels like Versace and Gucci, Farfetch also works with its own brands like Off-White. As a result of Farfetch’s reliance on big brands for product supply, it has a conflict of interest when it comes to serving small brands by prioritizing showcasing products from big brands on the main page or default search results. We think that this dispute has reduced the potential for independent or small brands to grow.

Pre-owned business model at The RealReal and eBay

Farfetch has ventured into the pre-owned item market by encouraging customers to sell their products to the platform in exchange for store credits. This move has put Farfetch in direct competition with established players such as eBay and The RealReal. However, it is worth noting that both eBay and The RealReal have shifted their focus from B2C to B2B operations in pre-owned luxury items. We have an article discussing the rationale behind this transition.

Firstly, the prices of pre-owned items online are often not significantly lower than the original retail prices, reducing the incentive for retail consumers to purchase through these platforms. Secondly, retail consumers may lack the expertise required to accurately assess the value and condition of luxury items sold online, further diminishing their interest in pre-owned purchases. As a result, online pre-owned luxury platforms tend to be more appealing to experienced buyers who can leverage the advantages of a wide selection and convenient shopping experience.

Given these considerations, we maintain a relatively pessimistic view of Farfetch’s B2C pre-owned luxury business.

Farfetch as a brand vs. Revolve

When examining the landscape of high-end apparel brands in the online platform space, Revolve stands out as a significant player, despite not always being recognized as such at first glance. In fact, we consider Revolve to be most closely aligned with Farfetch, both in terms of their business models and target audiences. Revolve leverages its online platform to sell its own exclusive high-end brand, Forward.

Navigating the maze: the fundamental

Digital platform services

Revenues breakdown (FTCH)

Financials (in $ thousands) (FTCH)

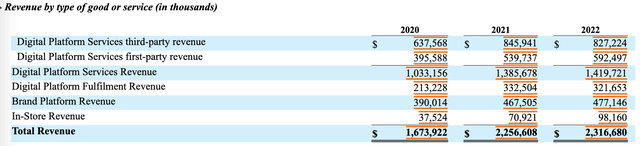

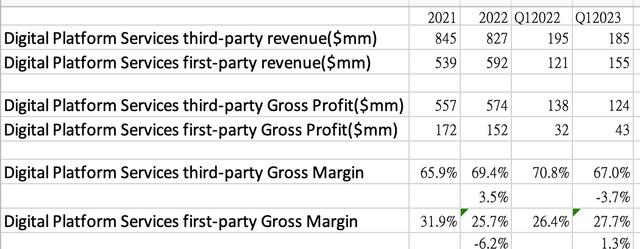

Farfetch witnessed diverging performances between its first-party and third-party businesses in 2021. Notably, the revenue generated through its third-party partnerships experienced a decline of 3% in 2022, and this downward trend continued in the first quarter of 2023 with a further decrease of 5%. In contrast, Farfetch’s first-party revenue showcased a positive trajectory during the same periods, exhibiting growth rates of 9.9% and 27%, respectively.

The underperformance of Farfetch’s third-party business can be attributed to its lack of competitive advantage within the market. This disadvantage has had repercussions for the company’s overall valuation, as evidenced by a 25% drop in its stock price over the past year.

However, there are signs of improvement within Farfetch’s operations during the first quarter of 2023. While the company experienced a decline in third-party revenue, its first-party revenue displayed promising signs of returning to a growth trajectory. Additionally, there was an enhancement in the first-party margin, indicating an improvement in profitability. Given these positive indicators, the 30% increase in the company’s stock price can be considered justified.

Digital platform financials (FTCH, LEL Investment)

Brand platform

The company’s brand platform and first-party products showed similar performance, with revenue growth and margin expansion in Q1 2023. The company attributes this positive outcome to solid underlying growth.

Looking ahead to 2023, the company expects its growth to be primarily fueled by licensing partnerships with Reebok, Ferragamo, and NMG.

Localization & private Client

The company believes that implementing a localization strategy will aid in expanding its presence in regional markets. In pursuit of this goal, they acquired stakes in YNAP and strengthened their partnership with Alabbar, a company controlled by Mohamed Alabbar, who holds significant influence in the Middle East region. While we recognize the importance of relationships in the luxury industry, the company must also tap into local markets for sustained growth. However, it should be noted that this partnership might not necessarily be favorable for Farfetch stockholders, as it could be costly and primarily increase the company’s revenues rather than its profits.

Another area of focus for the company is its private client strategy. To cater exclusively to its high-spending private clients, who annually spend over $10,000 and have an average order value of $1,000-significantly higher than the average order value on the Farfetch platform-the company has introduced a dedicated app called Fashion Concierge. Private clients gain access to exclusive and rare items, such as unique handbags, limited edition watches, fine jewelry, art, and homewares.

This service heavily relies on the relationships established by stylists with other luxury brands to secure high-quality and exclusive inventory. However, similar to the localization strategy, the private client strategy faces challenges regarding margin transparency. Additionally, both strategies appear to rely heavily on relationships with local companies or individual stylists, suggesting limited scalability. Maintaining multiple product lines and business models to drive growth can also incur substantial costs.

Valuation puzzle solved by the sum of the parts

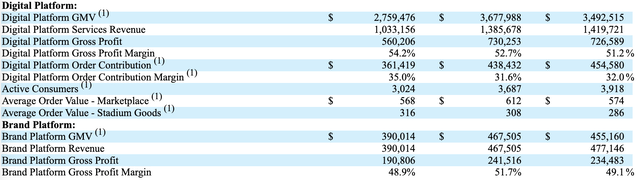

The company had projected a 16% increase in GMV and a 30% increase in revenue for 2023. This growth was primarily attributed to licensing deals and partnerships, which would predominantly contribute to first-party and brand platform revenue.

Nevertheless, its third-party sales, which still make up over 55% of its total profits, were on the decline. Therefore, the future ambiguity of its third-party revenue stream may be detrimental to its valuation.

So, in our opinion, the optimum method for stock valuation is the sum of the parts. The company’s third-party operations would be assessed as a marketplace platform, and the other aspects of the business would be assessed as a brand company. Each of them would be applied using different valuation multiples.

Base case:

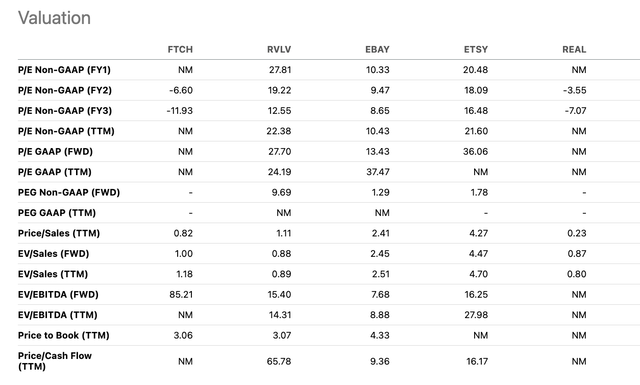

Since Farfetch has a similar gross margin level to eBay at 70% and a similar growth trajectory, we chose eBay as a comparison in our base scenario and assume that its third-party revenue will remain flat. We arrived at a $2 billion valuation for its third-party business by using eBay’s P/S ratio of 2.4x.

Valuation multiple (Seeking Alpha)

Margin (Seeking Alpha)

Based on management’s projections, we assume that its brand platform sales will reach $600 million in 2023. Its first party revenue will increase to $710 million in 2023 if we additionally assume that it will grow at the same rate as the GMV of the digital platform. Furthermore, we forecast a 30% increase in in-store sales. Based on these presumptions, $1.4 billion in revenue is generated. We picked Revolve as a comparable because it had a similar gross margin profile as Farfetch’s brand portfolio. As a result, if we utilized Revolve’s P/S ratio of 1.1x as a benchmark, Farfetch should be valued at $1.5 billion without accounting for its third-party business.

By combining the results of the two calculations above, Farfetch should have a market value of $3.5 billion by the end of 2023, a 77% increase from its present stock price.

Bear case:

Our worst-case scenarios would only value the company’s first-party business if we completely disregard its marketplace platform, since we think the company will eventually stop operating this line of business. In this scenario, the company would be valued at $1.5 billion, a 24% decrease from its present value.

Since we are generally skeptical about its third-party business, we feel that the base scenario has more potential but a lower likelihood of playing out in the long run. The bear case’s downward valuation is, however, rather constrained given how stressed its valuation is right now.

Overall, we observed that Farfetch’s brand portfolio was less competitive than that of its rivals. Following the death of its founder in 2021, the Off-White company appeared to lose its impetus, and the excitement surrounding sneaker culture had subsided. This is also evident from Stadium Goods’ declining average order value. We concluded that the risk-reward profile is fairly balanced.

Off-White google search (Google trend)

Bankruptcy case

The company expected it to generate positive free cash flow in 2023. It continued to grow its user base. However, as of Q1 2023, the company had only $485 million in cash and cash equivalents. In Q1, its cash burn rate remained high. We think there are still downsides ahead in the first half.

Catalysts

Moving ahead, there are a couple of catalysts that warrant close attention and have the potential to reshape our perspectives. Firstly, the re-acceleration of growth in the company’s third-party revenues is a key catalyst. Secondly, the acquisition of high-quality brands or improvements in fundamental aspects could also play a significant role. Presently, the company employs multiple business models to cater to diverse markets. While we currently view this strategy as unfavorable, it has the potential to change if the company decides to consolidate its operations. Therefore, we currently rate the stock as “Neutral.”

Read the full article here