Introduction

Archer-Daniels-Midland (NYSE:ADM), the agriculture giant with a $40 billion market cap, is trading 25% below its all-time high as the market has shifted its focus from value to growth stocks again. While economic headwinds and slowing inflation have caused investors to become less optimistic about ADM’s future, the company remains in a terrific spot. The newly crowned dividend king is now yielding close to 2.5%, and it has an attractive valuation and is poised to continue to benefit from long-term agriculture tailwinds.

In this article, we’ll discuss all of it and more!

Suddenly, Sellers Dominate

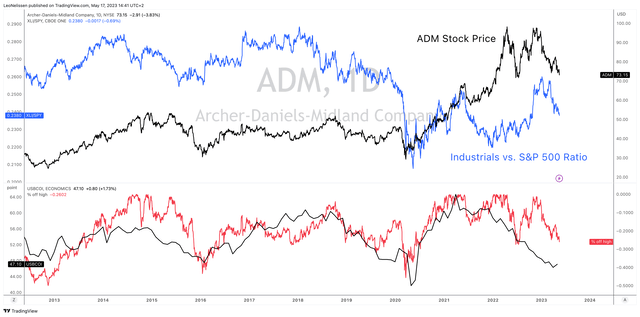

Let me start this article by throwing a somewhat complicated-looking chart at you.

TradingView (ADM, ISM Index, XLI/SPY Ratio)

The chart shows four different indicators:

- In the upper part, I compare the ADM stock price to the ratio between industrial stocks and the S&P 500. While ADM is a member of the consumer staple sector and not an industrial company, the ratio perfectly captures investors’ willingness to buy cyclical stocks. While ADM is defensive, it still relies on the health of the agriculture industry. Given the relationship between agriculture and energy, ADM is somewhat cyclical.

- The lower part of the chart displays the ISM Manufacturing Index. This index, as displayed by the black line, shows that we’re in a declining economic trend.

- The red line displays the distance (in percent) ADM shares are trading below their all-time high. Just like the upper part of the chart, the lower part displays that ADM’s market value is being dragged down by lower economic growth expectations.

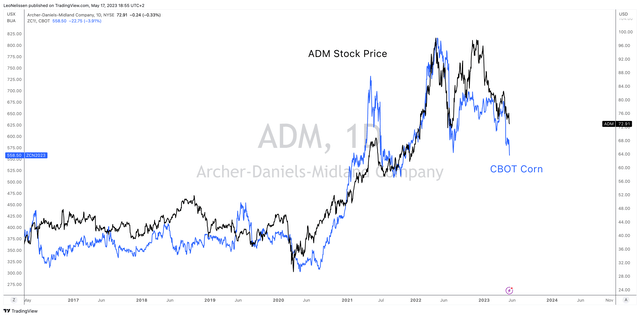

We also see that key agriculture commodities like corn are weakening. The chart below compares ADM to the price of CBOT corn, the most active corn future.

TradingView (ADM, CBOT Corn)

The good news is that this is making the ADM dividend a lot more juicier.

The ADM Dividend

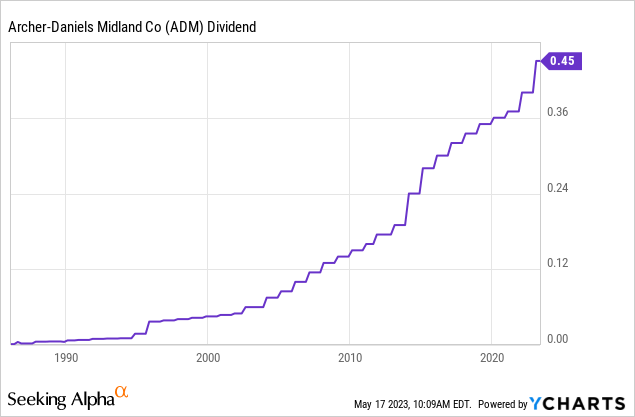

Before we dive into the company’s progress, we see that the recent stock price decline has caused the dividend to become a lot more attractive.

ADM currently pays a $0.45 per quarter per share dividend. This translates to $1.80 per year, and it implies a dividend yield of 2.5%.

While 2.5% isn’t something that gets income-seeking investors excited, it’s backed by a company that can call itself a dividend king as of 2023.

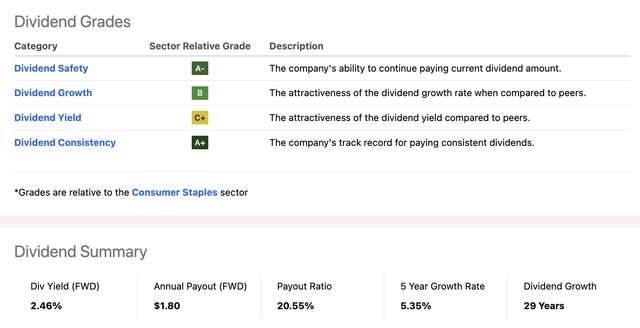

In January, ADM hiked its dividend by 12.5%, which marked the 50th consecutive annual dividend hike. This also explains why the company’s dividend consistency score is so high in the Seeking Alpha dividend scorecard below. Please note that the table says 29 consecutive years of dividend growth. I believe that this is caused by a spin-off or split that makes it hard to track long-term dividends. ADM is, in fact, a dividend king.

Seeking Alpha

Furthermore:

- On average, the ADM dividend has been hiked by 8.8% per year over the past ten years.

- The company has a payout ratio of 21%, which is below the sector median of 61%.

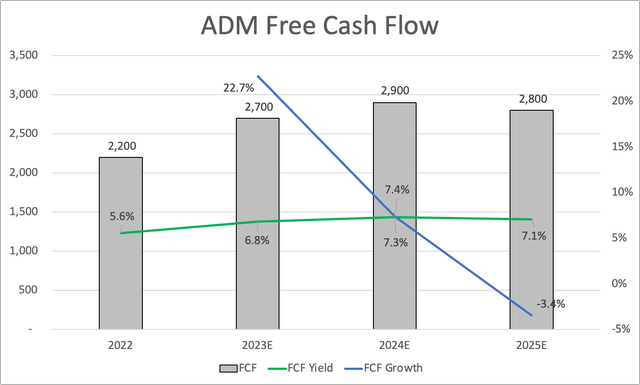

- The company’s cash payout ratio is roughly 35% using 2023/2024 estimates. As the chart below shows, ADM is expected to boost free cash flow to $2.7 billion in 2023, followed by another increase of 7.4% in 2024.

Leo Nelissen

In the first quarter alone, ADM generated operating cash flows before working capital of $1.3 billion. $325 million was allocated to capital expenditures, and $600 million was returned to shareholders through share repurchases and dividends.

It also helps that ADM has a stellar balance sheet, which allows it to use free cash flow for shareholder distributions.

ADM maintains strong liquidity with nearly $10 billion of cash and available credit. The adjusted net leverage ratio of 1.2x EBITDA is well below its 2.5x threshold. The company enjoys an A credit rating.

This brings me to the company’s latest quarterly update, which revealed a lot about its business and the state of global agriculture.

Unlike Its Stock Price, ADM Is Doing Fine

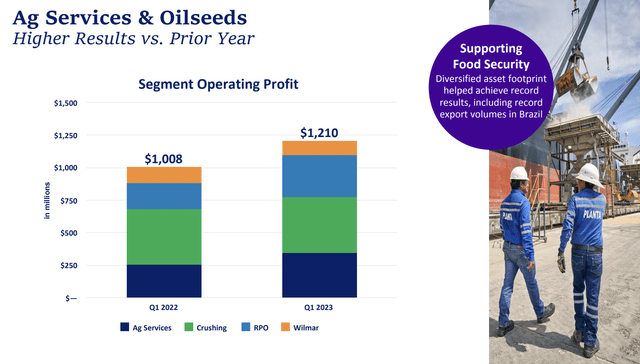

In 1Q23, ADM reported 1.8% higher revenue. In agriculture services and oilseeds, which accounted for 78% of 2022 revenues, the company boosted operating profit by 21%.

Archer-Daniels-Midland

South American origination witnessed excellent risk management and increased export demand due to the Brazilian soybean crop, leading to significantly higher year-on-year results. North American origination also saw higher results, driven by stronger soybean exports. Global trade performed well, thanks to solid margins and efficient execution.

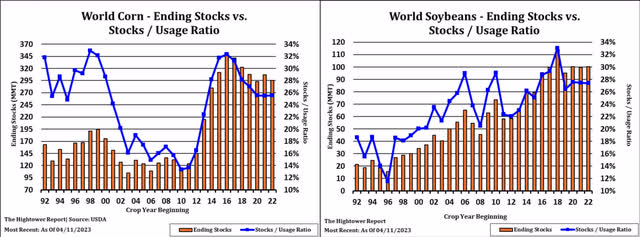

I’m not surprised by these results, as export demand is high. When looking at two key crops that were also mentioned by ADM, we see that the global stocks/usage ratio of both corn and soybeans is at multi-year lows. In this case, the data includes China, which is an import nation.

CME Group

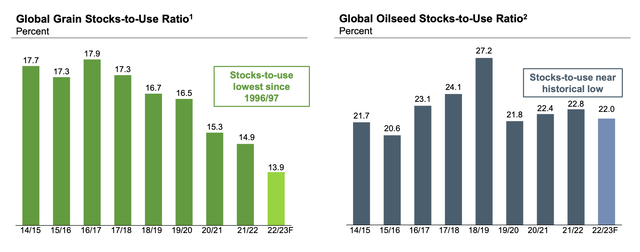

The data below, which excludes China and is provided by fertilizer giant Nutrien, shows that global grain stocks are at levels not seen since 1996/1997. This indicates high export demand benefiting export nations like the United States, Brazil, and Canada. It also confirms ADM’s numbers and comments.

Nutrien Ltd.

Related to this, the company noted that despite supply and transportation constraints in the Black Sea region and severe drought in Argentina, it leveraged record Brazilian crops and improved demand in China. Broad-based food demand remained resilient across key geographies, leading to solid volumes and strong operating margins in various sectors, including vegetable oils, flavors, sweeteners, starches, and wheat milling.

With that said, crushing results were in line with the first quarter of 2022. However, crush margins in EMEA nations were lower year-over-year as trade flows adjusted from the dislocations caused by the war in Ukraine. Refined products and other results were significantly higher compared to the prior year period.

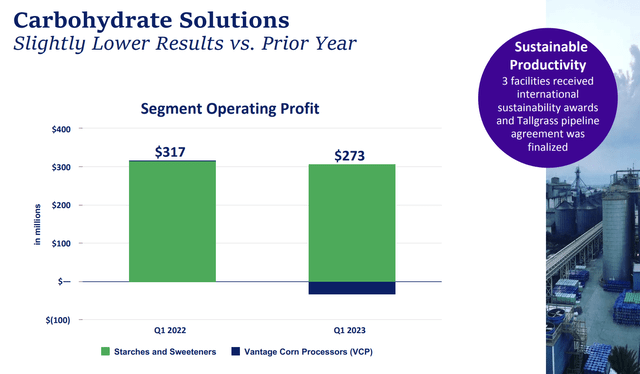

The carbohydrate solutions segment performed well but less successfully than last year. Ethanol margins decreased compared to 1Q22 due to high industry stock levels.

Archer-Daniels-Midland

Furthermore, the global wheat milling business posted significantly higher margins driven by robust customer demand. Vantage Corn Processors’ results were considerably lower due to weaker ethanol margins.

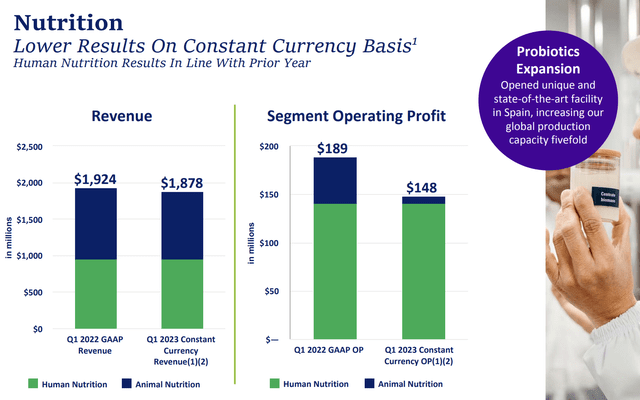

The smaller Nutrition segment also saw lower results. As Human Nutrition was strong, the decline was mainly driven by Animal Nutrition due to much lower margins in amino acids.

Archer-Daniels-Midland

So far, so good.

What matters is what the company expects going forward. After all, trade tailwinds and ethanol headwinds were expected, given global developments and pricing.

In the second quarter, the company expects the Ag Services & Oilseeds segment to continue its strong performance. Crushing is projected to be robust but lower than the previous year based on current crush margins. Also, as expected, the company does not anticipate a recurrence of last year’s significant volatility that affected energy and grain trade flows in Ag Services.

In its Carbohydrate Solutions segment, the company expects resilient demand and strong margins for Starches and Sweeteners products in the second quarter. However, ethanol margins, while improving, are projected to remain below last year’s levels, which isn’t something that came as a shock.

For the full year, Nutrition aims to achieve 10% plus constant currency operating profit growth, led by Human Nutrition. The company remains optimistic about the Human Nutrition sales pipeline and growth opportunities, expecting a continued recovery in demand fulfillment and reduced destocking effects.

In this segment, operating profit growth will be heavily weighted towards the second half of the year.

Valuation

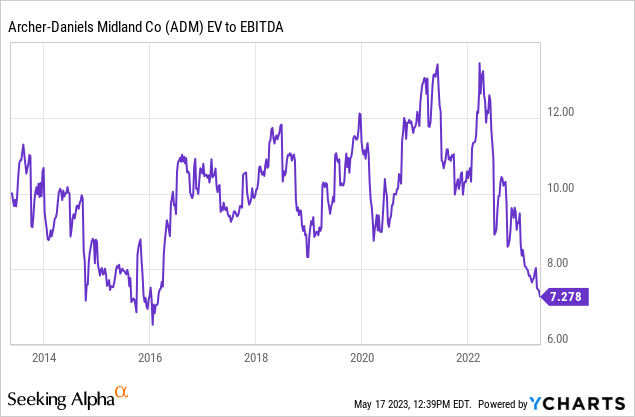

ADM is trading at 7.8x 2023E EBITDA, based on its $39.6 billion market cap, $7.9 billion in 2023E net debt, $340 million in minority interest, and $6.1 billion in expected EBITDA.

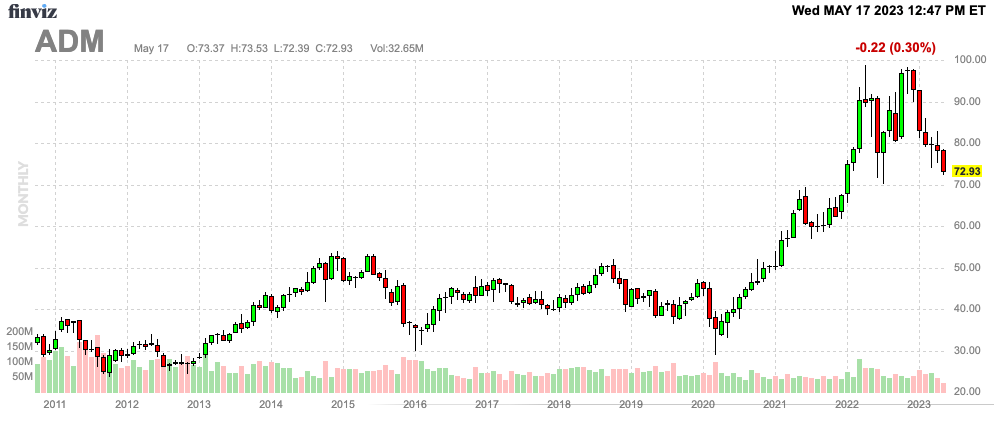

Given these numbers, I believe that ADM has a fair value between $100 and $110.

FINVIZ

Needless to say, I cannot guarantee that ADM is bottoming. Further economic deterioration could make this a bumpy recovery. However, I like the risk/reward, and I am considering buying ADM for a number of portfolios that I am advising if I can get in between $60 and $70.

Takeaway

Archer Daniels Midland, an agriculture giant, is currently trading 25% below its all-time high and offers a dividend yield of 2.5%. The company recently became a dividend king with 50 consecutive years of dividend increases.

ADM has a strong balance sheet, with ample liquidity and a favorable credit rating. In the first quarter of 2023, ADM reported higher revenues and operating profits in its agriculture services and oilseeds segment, driven by global export demand.

The company expects continued strong performance in the Ag Services & Oilseeds segment and resilient demand in its Carbohydrate Solutions segment.

ADM is trading at an attractive valuation, and while further economic deterioration could pose risks, the stock presents a favorable risk/reward opportunity.

Read the full article here