Last month, I detailed how high profile ETF manager Cathie Wood and her firm Ark Invest were continuing to increase their holdings in cell programming and biosecurity company Ginkgo Bioworks (NYSE:DNA). Even as shares continued to hit new lows, two of the firm’s ETFs kept buying more shares. After the close on Wednesday, Ginkgo reported its Q1 results, with the report leading to more questions about the company’s future growth trajectory.

For the first quarter, total revenues came in at $81 million. This was a decrease of 52% driven by the expected ramp down of K-12 Covid testing in Ginkgo’s Biosecurity business unit. Despite the year over year plunge, the reported figure actually smashed street estimates by nearly $9 million. Cell Engineering revenues (formerly called the Foundry segment) showed 59% growth, coming in at $34 million.

One of the big issues for Ginkgo currently, like any early stage company in this space, is that net losses are quite tremendous. The company lost almost $205 million in the period, or 11 cents per share, which missed street estimates by 2 cents. That loss was much narrower than the year ago period, which featured a large stock based compensation charge. However, adjusted EBITDA came in at negative $100 million, as compared to less than $1 million in the red a year earlier.

These large losses are leading to a bit of cash burn at the moment. Free cash flow was negative $110 million in the period, up from less than $25 million in the year ago period. That’s not a major problem at the moment as the company’s cash position was at $1.2 billion at the end of Q1, but it will be something to watch. The main issue here is that a lot of the net loss add-backs on the cash flow statement are due to stock based compensation, which means investors are being diluted a bit each quarter.

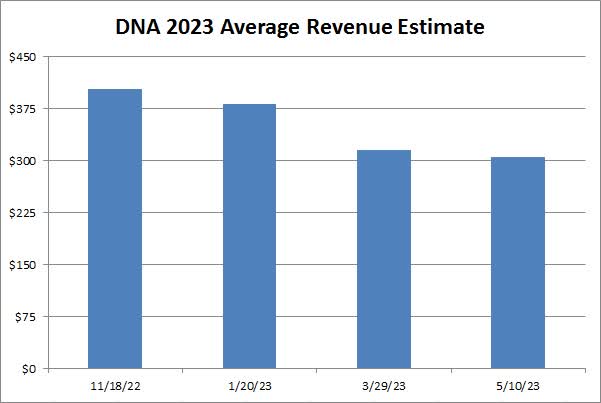

The reason why I think the stock got tripped up in the after-hours session was management’s revenue guidance for the year. Revenue is still expected to be at least $275 million, but the Q1 result annualizes out to quite a bit more than that. As the chart below shows, street estimates have been coming down for several months, with the 2023 average being over $304 million going into this report. Either management was being very conservative here, or analyst estimates need to continue lower moving forward.

DNA 2023 Average Revenue Estimate (Seeking Alpha)

I bring up this potential guidance disappointment because it makes me wonder about growth in the coming years. We’ve already seen analyst revenue estimates for future years drop quite a bit. Last year, the Cell Engineering segment showed 27% revenue growth, and this year’s forecast for at least $175 million implies growth of at least 21.5%. However, analysts next year are expecting more than 45% overall top line growth on top of this year’s more than $304 million current estimate.

The current average 2024 revenue estimate implies quite a bit of revenue growth acceleration, and we’re not sure if the Cybersecurity business will show any growth in 2024. The company talked about emerging product lines that could develop more recurring revenues, but in the past six months, the average revenue estimate for the next three individual years has come down by 30%, 36%, and 44%, respectively. When investors see growth estimates come down like that in such a short time period, sentiment is likely to remain quite negative.

As for Ark Invest, the stock is held in both the flagship ARK Innovation ETF (ARKK), along with the ARK Genomic Revolution ETF (ARKG). There have been more share purchases since my previous article, with those two funds holding about 158 million shares as of Tuesday. That is just under 10% of Ginkgo’s Class A shares outstanding (the shares that trade in the market), although Ark’s overall ownership percentage is a bit less if you include Class B and C shares discussed in the 10-Q filing.

Going into Wednesday’s report, the average price target for Ginkgo on the street was $4.52, implying massive upside from current levels. However, with not a lot of analysts covering the name, the $12 high target brings up that average quite a bit. If we continue to see revenue estimates come down, it’s likely that we’ll also see some price targets cut too. With shares down a dime to $1.25 in the after-hours session, the stock fell below its 50-day moving average again (purple line below). That could add some technical selling pressure, especially if the 50-day starts to head lower again.

DNA Last 3 Months (Yahoo! Finance)

In the end, Ginkgo Bioworks reported mixed results for Q1 on Wednesday, sending shares lower in the after-hours session. While revenues did come in well ahead of street estimates, net losses were also larger than expected. Management did reiterate its 2023 revenue forecast, but there remains a large disconnect between that guidance and the street. While the name has a strong supporter behind it in Cathie Wood, tremendous revenue estimate cuts for future years seem to be hanging over this stock. Until those expectations stop falling, and perhaps until those large losses improve a bit, I don’t know if investors will see the tremendous upside that some analysts are calling for.

Read the full article here