Investment thesis

Apple (NASDAQ:AAPL) is returning cash to shareholders at an unprecedented rate with a new $90 billion buyback program launched a few days ago. At the same time, the company is pushing to grow through financial services that will bring a new ecosystem on top of the legacy hardware ecosystem. Through this, Apple is set to continue growing. For the long-term investor, the combination of cash returns and growth present a buying opportunity based on my valuation of the Apple stock.

Business overview

Revenue breakdown

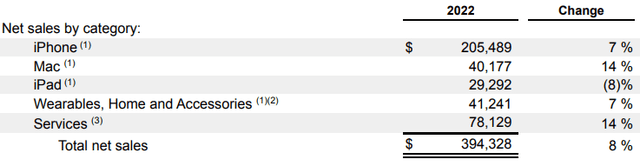

Apple’s business and products need little introduction. Here, I will resort to simply presenting the distribution of Apple’s revenue (from the most recent full year reported):

Apple 2022 10-K filing

As shown in the presentation, an entire 50 %+ of revenues come from selling iPhones. Sales of the iPhone has grown in the single-digits the past year.

The second largest segment is Services – App Store, Apple Music, Apple TV, Apple Pay, Apple Card etc. – and this segment accounts for ~38 % of revenues. Alongside the Mac segment it is the fast-growing segment with a 14 % increase year-over-year.

Apple’s most recent quarterly earnings

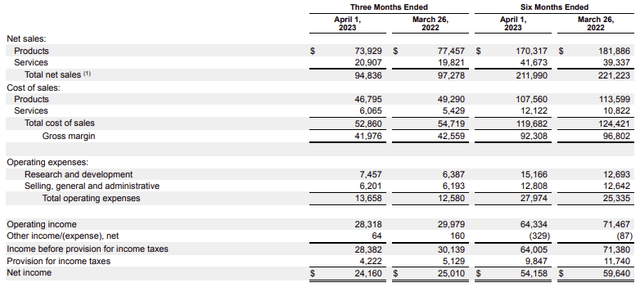

Apple reported earnings on 4 May 2023 covering Q2 2023, topping consensus estimates.

EPS came in at $1.52. Revenues were $94.84 billion, a 1.5 % year-over-year increase. Net earnings for the company were $24.16 billion.

In its 8-K filing, Apple summed up results as follows:

Apple most recent 8-K filing

While the most recent quarterly results were pretty good, looking at the past several years leaves an even more convincing impression. Apple has managed to grow top and bottom lines almost every year for the past 10 years:

Author’s presentation, data from Apple 10-K filings

As shown above, profit margins are consistently in the ~20 – 25 % range, suggesting strong pricing power and consistent cost control.

Because of its wide span of products and services, it’s hard to determine a very comparable, direct competitor to Apple. Obviously, Apple competes with several major companies, but none have identical segments.

If we narrow competitors down to making smartphones, you can point to Samsung being the largest competitor. The comparison of numbers between the two, however, is perhaps not as informative as it could be as Samsung offers a much wider array of hardware than Apple:

Author’s presentation, data from Companiesmarketcap.com

As Apple is generally compared to other members of the “Big Five” tech giants, I would like to point out one company – Microsoft (NASDAQ:MSFT) – which I believe is more comparable to Apple than Samsung or other hardware companies. Microsoft has displayed a quite similar growth pattern to Apple:

Analyst’s presentation, data from Microsoft 10-K filings

Microsoft, on the other hand, has been able to grow its profit margin substantially over the past few years in particular. Microsoft’s profit margin is more volatile than Apple’s, it appears.

The future development of Apple’s numbers and its ability to keep competing with Microsoft and others will come down to its growth efforts which I will examine in further detail below.

Growth prospects of Apple

One of the great strengths of Apple is the “Apple Ecosystem”. This is the system-wide integration that makes for better user experience for users who have multiple Apple devices. All Apple devices are able to “talk together”. And when new devices are added, it adds to the ecosystem and the value to the Apple customer.

This ecosystem started with hardware, and in recent decades has expanded to services and most recently financial services.

Whether in one area or the other, I believe it’s obvious that Apple must continue to develop its ecosystem to grow – and not least to grow enough to justify paying ~30x earnings for the stock.

In the following sections I will try to analyze the potential growth areas for Apple and make my own personal assumptions about them and their potential for investors:

Apple hardware

In recent years, Apple has come under criticism for not innovating. By “innovating”, much of that criticism seems to point to the lack of new blockbuster hardware products – whereas if we go back a little further in time, the company would frequently launch new blockbusters like the iPhone in 2007, the iPad in 2010, and the Apple Watch in 2015. Of course, the company has launched several new products: Including the HomePod in 2018 (smart speaker) and the Mac Studio and Studio Display in 2022. But none of these seem to have caught quite the same general excitement as previous hardware innovations.

My take on Apple’s hardware segment from an investment standpoint is that it is currently the vastly most important area to Apple from a revenue and earnings perspective – and that it will remain so for a long time. I suspect that the segment is going to continue to grow, but I anticipate that will be mostly from upgrades to popular current products (mostly the iPhone, iPad, Watch). In valuing Apple – see the Valuation section – I will attempt to determine the investment value of Apple’s hardware segment based on an assumption of single-digit growth.

That’s not meaning to say I think Apple can’t tap into new areas of growth. I think they have and will – in other areas than hardware:

Apple services

“Services” as a segment is Apple’s second largest in terms of revenue. It’s also the fastest growing. In the context of Apple’s hardware business starting with the Apple I in 1976, betting big on services is a fairly new venture for Apple. “Services” spans a wide range of various services, but here I will focus on the financial services introduced by Apple:

In 2014, Apple launched Apple Pay. From a technological standpoint, it can replace a credit card and PIN transaction at a contactless-capable point-of-sale terminal. From a business standpoint, it was the kick-off to building a new financial ecosystem. This continued when in 2019 Apple launched Apple Card, a credit card issued by Goldman Sachs (NYSE:GS) but branded under the Apple “umbrella”. One of the key features of being a cardholder is that you can buy new Apple products and pay for them over time, interest-free (“Apple Card Monthly Installments”). To Apple, this means retaining customers and incentivizing repeat business. The culmination of this approach came when Apple launched their BNPL service (Buy Now, Pay Later) followed up by their savings account powered by Goldman Sachs but also branded under the Apple name. The savings accounts offers Apple customers a fixed rate of 4.15 % annually on savings. I call this a culmination because it means you can now keep your money within the Apple ecosystem (using the Apple bank account, the Apple credit card, Apple Pay and the BNPL service) and you are incentivized to keep it there when you spend money. This also benefits Apple from a data perspective: They know more about their customers the more they keep them within the ecosystem. In that sense, it’s all about data; what you buy, where you buy, and how much you buy. The further upside for Apple in this regard is that it keeps a steady flow of capital coming in to Apple for financing and cash allocation internally. Over time, however, I suspect growth will be centered around Apple’s financial services. The danger, of course, is that Apple is becoming more of a “financial institution” with all that involves – including the risk that depositors withdraw their money from the Apple ecosystem.

Apple Dividends and Buybacks

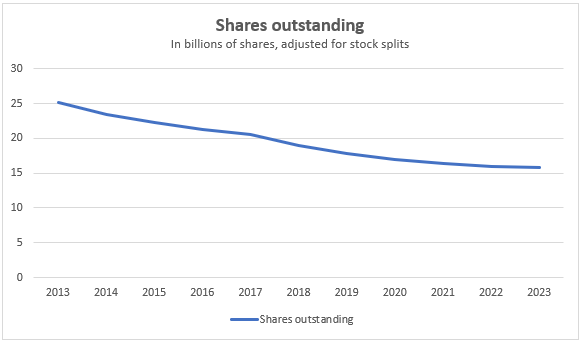

Apple has bought back a significant amount of shares since initiating its first comprehensive buyback program in 2013:

Apple 10-K filings and most recent 10-Q filing

Buybacks are often criticized in the media and even among much of the investment community. I think people who disfavour buybacks when made by a company that has surplus cash flow and whose shares trade at attractive prices ought to study the practices of some of the best investors in the world and their take on the issue. Here’s Warren Buffett’s take:

When you are told that all repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to either an economic illiterate or a silver-tongued demagogue (characters that are not mutually exclusive).

One reason you may even favour buybacks over dividends is that the benefit of buybacks for continuing shareholders is tax free – aside from the marginal excise tax imposed on the business buying back its shares. This is different from dividends which are taxed as capital income. Over time, it makes an enormous difference whether value is taxed or not as returns compound.

Of course, buying back shares must be done at times when the stock is undervalued. Most of the time buybacks are automated according to an authorization by the company’s board of directors. But that doesn’t change the fact that management will have made the assessment that a) the company has or is able to obtain excess cash to return to shareholders, and b) the best opportunity to utilize that cash is through buying back the share. When the company in question – as in the case of Apple – has been able to grow consistently, even automated buybacks turn out to be great purchases even if made at wildly different price points (that perhaps wouldn’t necessarily seem “undervalued” at the particular time of purchase).

In my opinion, buybacks have greatly benefitted investors of Apple. To illustrate this, let’s have a look at the dividend and the EPS. The current dividend of Apple is $0.92 per share a year. If Apple had maintained its 2013 share count to date, that dividend – all else equal – would be ~$0.59. EPS for 2022 was $6.15. It would have been ~$3.88 without the buybacks.

I think it’s beyond doubt that Apple shares would have been worth less with about half the dividend and half the earnings per share.

But then the important thing isn’t the past but the future. Will buying back shares still be beneficial for continuing shareholders going forward? It certainly would underscore the shareholder friendliness of management, which is important. But to me the most important component in answering that question is whether Apple will continue to be able to grow. On 4 May 2023, Apple launched a new $90 billion buyback – underlining management’s belief in the approach.

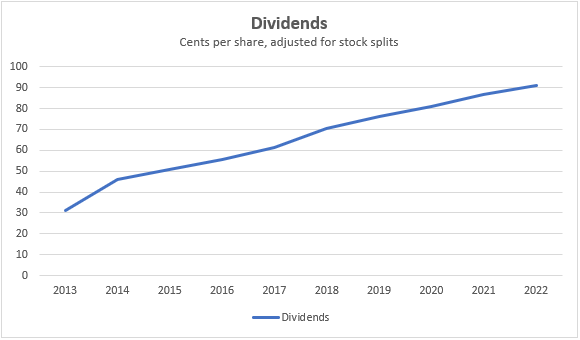

Aside from buybacks, Apple returns cash to shareholders through quarterly dividends. Dividends have come up substantially over time:

Author’s presentation, data from Nasdaq.com

As noted previously, one important factor in Apple’s ability to raise the dividend has been buying back the share. When Apple buys back shares, those shares are retired and the dividend that would have otherwise accrued on the shares is voided.

Apple Stock Value

In 1937, John Burr Williams conceived the idea that the value of a business was equal to the amount of all future dividends paid out to investors in its lifetime (discounted to present-day value). This is now known as the dividend discount model (DDM). This has since become an authoritative model for valuing equities. At the time of the DDM’s conception, most cash returns to investors were in the form of dividends. Now in 2023, the majority of cash returns to investors in the United States come in the form of share repurchases/buybacks. Apple has led the way in transitioning from dividends to buybacks. This makes valuing Apple based on dividends alone quite misleading as you’d be disregarding the billions of dollars returned through buybacks. In other words, you’d be modelling a value of Apple that did not account for the obvious value attained from being less shareholders owning the same company.

For the purposes of this valuation, therefore, I will use a modified version of the dividend discount model – the so-called H-Model – and when discounting the expected dividends I will add in the expected future buybacks. You could say that in doing so I am considering the buybacks merely a different kind of dividend that I will add on top of the “classic” dividend, and then discount the total returns.

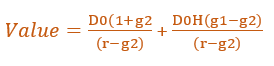

The H-Model itself consists of the following elements:

Author’s presentation

The elements of the H-model mean:

Author’s presentation

The general idea of the H-Model is to reflect that typically companies who increase their dividend will do so at a faster pace initially than later. One valuation is made for the period of high increases, one for the period of lower increases, and the two are added together for an aggregate valuation.

For 2022, Apple paid a total of $14,793 million in dividends and made buybacks of $89,402 million. This is $6.63 per share currently outstanding (annually).

In terms of Apple’s hardware business, it generates ~80 % of revenues – and can therefore be said to also be responsible for 80 % of dividends and buybacks. For this valuation, I will assume that the hardware business will grow at ~7 % annually – which is slightly more than the weighted average growth rate of the individual parts of the hardware segment – for 10 years, and thereafter at a “perpetual” rate of 5 %. 80 % of Apple’s payouts to shareholders (dividends and buybacks) at said growth levels is worth $152.49 at a discount rate of 9 % (used here as it’s somewhat in line with historic returns of the S&P 500).

In terms of Apple’s services segment, it is responsible for ~20 % of Apple’s business and the corresponding percentage of cash returns. In terms of growth, I will assume 14 % growth in line with current trends for 10 years, and a perpetual rate of 5 % thereafter. 20 % of Apple’s payouts to shareholders (dividends and buybacks) at said growth levels is worth $49.73 at a discount rate of 9 %.

Under these assumptions, each share is modelled to be worth a total of ~$200.

To ‘challenge’ my calculations in connection with the valuation according to the DDM model above, I would like to analyze valuation multiples and compare them to past levels. Apple’s 5-year average P/E ratio is ~24.5. This compares to a current P/E ratio of ~29. Assuming a value in accordance with the 5-year average, each stock should trade at ~$145. This would suggest overvaluation by the market currently.

The analysis above suggests a “value range” of $145 to $200 per share of Apple. With the stock trading in the “sweet spot” between the two, this may be the right time to pick up the stock if you believe the growth assumptions I made in respect of the hardware/services business.

Risks associated with the Apple stock

As with any other publicly traded business, Apple discusses certain risk factors impacting their business in the 10-K filing. One such risk factor identified by management is one I think is currently very relevant. Management defines it as:

[Apple’s] business can be impacted by political events, trade and other international disputes, war, terrorism, natural disasters, public health issues, industrial accidents and other business interruptions.

Substantially all of Apple’s manufacturing is performed by outsourcing partners located in mainland China and several other parts of Asia. This includes manufacturing of the iPhone which as noted earlier accounts for more than half of Apple’s revenues.

It’s impossible to forecast geopolitical developments, but with analysts pointing to a worsening relationship between the United States and China and increased military tensions, I think it’s equally impossible to ignore the risk imposed on Apple by this relationship. Apple is doing something about it – having recently upped their production significantly in India – but the risk is still there with great dependence on China in particular.

Perhaps one way to account for this risk factor while the Apple management is doing theirs to handle it would be demanding a larger margin of safety on the purchase price. You could simply value the company and only buy if and when the discount to your valuation is attractive enough.

Another risk I would like to highlight here is one defined by management as follows:

Global markets for [Apple’s] products and services are highly competitive and subject to rapid technological change, and [Apple] may be unable to compete effectively in these markets.

This point is the essence of the previous discussion of Apple’s growth prospects – and the substantial impact those prospects have on a fair valuation of Apple and thus potential investor returns. With Apple shares trading at almost 30 times earnings, growth is needed to justify the price demanded by the market. Couple this with strong competition on several fronts – Samsung for smartphones, Microsoft, Alphabet, Amazon etc. for cloud and so forth – and it becomes evident that Apple must keep innovating to stay ahead. Apple is doing a lot – in terms of financial services in particular. Only time will tell if enough is being done.

Conclusion

In conclusion, I think Apple is a high-quality business with future growth potential in it. I believe growth will mostly come from the Services segment.

In terms of shareholder cash returns, Apple has been consistently buying back its shares since 2013 and increased its dividend for several years. The dividend was raised again on 4 May 2023, and a new buyback program was authorized the same day. In my opinion, Apple’s history of consistent direct cash returns to shareholders have increased the value of each Apple stock.

I believe the main risks associated with buying Apple stock are the company’s reliance on foreign manufacturers and the geopolitical environment, and the fact that the company is entirely dependent on continuous technological innovation against strong competition. Apple is managing these risks by diversifying manufacturer locations and by launching new products and services.

When valuing the stock based on growth assumptions for the hardware/services segments, the modelled value displays current undervaluation by the market.

For the reasons stated above, I rate Apple a Buy.

Read the full article here