S&P Global Ratings lowered Campbell Soup’s Co.’s rating to BBB- from BBB on Monday, placing it one notch above speculative-grade, or junk, status.

The move came after the company announced a $2.7 billion all-cash deal for Sovos Brands, parent of Rao’s pasta sauces and noosa yogurts, that it intends to fund by issuing new debt.

“As a result, we forecast S&P Global Ratings-adjusted pro forma debt leverage will increase to about 4x at close from 2.8x for the 12 months ended April 30, 2023,” the rating agency said in a statement. “We do not forecast the company to restore leverage to the low-3x area until at least fiscal 2026.”

Campbell Soup

CPB,

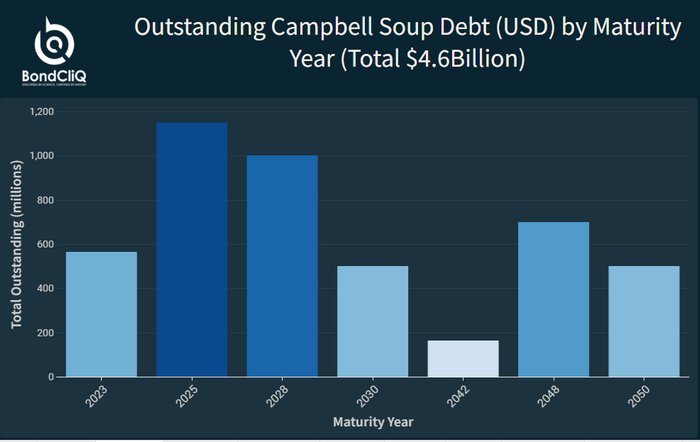

has about $4.7 billion of debt, according to FactSet.

As the following chart from data-as-a-service company BondCliQ Media Services shows, there were only sellers of the bonds after the downgrade although volumes were light in summer trading.

S&P said it expects free operating cash flow, or FOCF, will be weaker over the next two years as Campbell Soup grapples with higher interest costs and increased capex investments, leaving it with less cash for discretionary debt reduction.

“We estimate the company’s interest expense will increase meaningfully with the new debt and the company plans to increase capex with capacity expansion projects over the next three years,” the rating agency noted. “As a result, our base case estimate for FOCF is lower than historical levels.”

S&P is confident that restoring the financial profile will be a priority for Campbell Soup over shareholder returns or other debt-financed deals. The company said it would prioritize debt reduction in the next two years and would limit its share buyback program to restore leverage to closer to 3 times within three years.

The company’s business risk is also satisfactory and believes the deal will benefit its portfolio.

“Rao’s will secure Campbell’s leading market position in the ultra-distinctive Italian sauces category and is highly differentiated from its mainstream Prego brand,” said the agency. “We believe Rao’s will add a sizable brand that could mitigate demand fluctuations in soups.”

The stock was down 1.7% Monday and has fallen 21% in the year to date, while the S&P 500

SPX

has gained 17%.

Read the full article here