Introduction

In the midst of Block Inc’s (NYSE:SQ) Q2 earnings report, I have analyzed this favorite holding of mine, from the ground up, through the 10-bagger scale. This company is the largest holding in my “$10,000 ‘Importance’ Portfolio: The Start Of A New Series“, which may present a hint of bias, though I attempt to keep my analysis balanced with well-grounded data. In all, the company scored the highest rating on the 10-bagger scale as of yet which makes this company an exciting buy for the long term. If you enjoy, disagree with the article, or want to discuss more then drop a comment and follow for more analyses of potential 10x companies!

The 10-Bagger Rating List

Check out the start of this series in “The Hunt For Potential 10x Returns: 2 Software Giants” where I have calculated the required annualized return to gain 10x returns over different time horizons. The power and influence 10x returns can have on your portfolio is immense, and I believe there are certain factors that correlate with this outcome. In short, this is what the series is all about:

In this series, I will be rating one/two companies based on pre-determined criteria which have been found to increase the chance of a stock becoming a 10-bagger. My goal in this series is hence to give investors a quick checklist of 10-bagger factors for a multitude of different companies to compare with over time. Furthermore, I will be cumulatively adding to a scatterplot each company’s 10-bagger rating and Seeking Alpha Quant rating which we can track over time.

With inspiration from Christopher Mayer and Peter Lynch, as well as my own experience with investing, I have created the following rating list, which ranges from 1-10, with what I believe are the most important factors that contribute to a potential 10-bagger status. (if you have any recommendations for new factors, please let me know in the comments!)

Rating List

- Profitability (“ROIC”), (“ROE”) or (“ROCE”)

- Insider Ownership

- Share Repurchases

- Gross Profit Margin

- Intangibles.

Profitability: Ex. Returns on Invested Capital (“ROIC”), Return on Equity (“ROE”), Return on Capital Employed (“ROCE”).

| Rating | Level |

| 1-2 | <(0)-2% |

| 3-4 | 3-6% |

| 5-6 | 7-9% |

| 7-8 | 10-15% |

| 9-10 | 15%+ |

Insider Ownership

| Rating | Level |

| 1-2 | 0-5% |

| 3-4 | 5-10% |

| 5-6 | 10-25% |

| 7-8 |

25-50% |

| 9-10 |

50%+ |

Share Repurchase (yearly % purchase of outstanding shares)

| Rating | Level |

| 1-2 | <(-5%) |

| 3-4 | (-5)-(0%) |

| 5-6 | ±0% |

| 7-8 | 1-5% |

| 9-10 | 5%+ |

Gross Profit Margin

| Rating | Level |

| 1-2 | Compressing |

| 3-6 | Steady |

| 7-10 | Expanding |

Intangibles

| Rating | Intangible Asset |

| 1-10 | Company Culture |

| 1-10 | Industry Potential |

| 1-10 | Operating Leverage |

Block Inc: $ billion Market Cap

($ billion for 10-bagger status)

| Characteristic | Level | Rating |

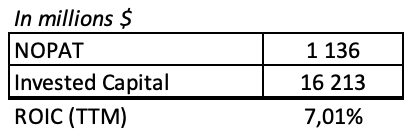

| Returns on Invested Capital (“ROIC”) | 7.01% | 5 |

| Insider Ownership | 10.39% | 10 |

| Share Repurchases | (31.3%) | 1 |

| Gross Profit Margin | Expanding | 10 |

| Intangibles | Exceptional | 8.7 |

Total Points: 34.7/50

Returns on Invested Capital (“ROIC”)

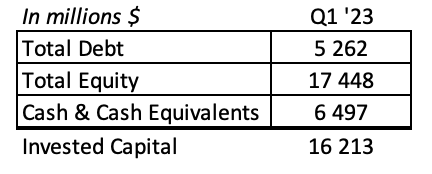

Block Inc’s balance sheet comprises of unprecedented components, that the average investor may look over when analyzing the company. To begin with, Block has $5.2 billion in convertible note debt, in six different installments, due between 2023-2031. As a result of the raised debt, positive free cash flow since 2017 (Seeking Alpha Cash Flow Statement), as well as investing customer funds in short-term debt, the company has accumulated a $6.5 billion cash and cash equivalents position. The last part about customer funds may be overlooked by investors. Block has $3.8 billion worth of customer funds on its balance sheet (Q1 2023) from stored balances in Square and on the Cash App. According to the company’s most recent 10K, it is not allowed to use this cash for its own operations but it may invest these deposits in short-term debt securities (2022 10K), which show up “as a component of subscription and services-based revenue” on the company’s income statement. Apart from this, Block has recently purchased Afterpay which increased the company’s goodwill position to a whopping $11.9 billion. Hence, in sum, Block has a total invested capital as of the previous quarter of $16.2 billion.

The Author

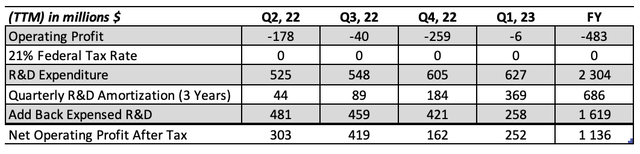

For the sake of this calculation, and in line with my previous articles, I will use twelve trailing months figures and I will adjust “NOPAT” by capitalizing R&D costs for an assumed 3 years. Block spent around 12.5% of revenue on product development during the latest quarter (including Bitcoin (BTC-USD) revenue). When excluding Bitcoin revenue, the company spent an extraordinary 22.1% of revenue on product development. This is an average amount compared to, for example, Palantir and Snowflake that I analyzed at the beginning of this series in “The Hunt For Potential 10x Returns: 2 Software Giants”, where the companies spent 17.1% and 43.3% of sales on R&D in Q1, respectively. However, in general, Block has a high rate of reinvestment in internal development. Hence, when adding back expensed R&D, I find that Block has an adjusted “NOPAT” of $1.14 billion (“TTM”).

The Author

When dividing “NOPAT” by invested capital, I find that Block has a “ROIC” of 7.01%. This places the company in the middle range of the 10-bagger scale, which earns it a 5/10 in profitability. While “ROIC” was 7% for the trailing twelve months, I have noticed that Block’s profitability is trending in a more positive direction. For example, the 1% “YoY” decrease in sales and marketing expenditures and the nearly 3% “YoY” decrease in general and administration costs helped the company achieve near-net profitability in the latest quarter. I expect the company to continue cost reductions and as a result, increase its returns on invested capital.

The Author

Insider Ownership

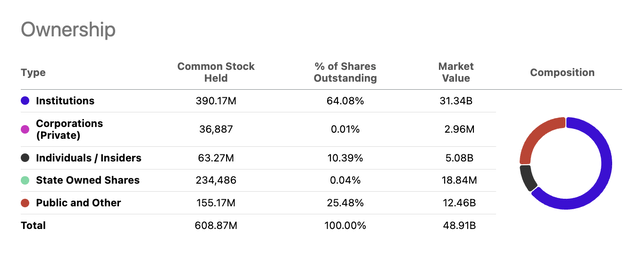

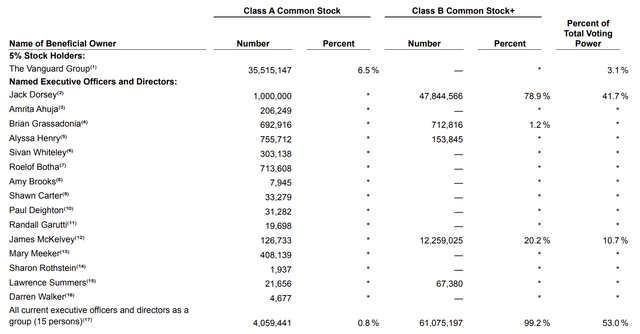

According to Seeking Alpha’s estimate, insiders own 10.39% of the outstanding shares of Block Inc. The two largest insiders are by far, in order, Jack Dorsey and James McKelvey. These two entrepreneurs started Square as a solution for merchants to accept credit card payments. The company quickly scaled in the following way:

“The early iPhone dongle quickly evolved into an iPad app to get rid of the need for cash registers. Square struck a deal with Apple to sell its hardware in stores, and later with Starbucks, becoming its official card processor. From there, Square started focusing on all things small business, including loans and payroll. It bought food delivery service Caviar, then a few years later sold it to DoorDash.”

(CNBC)

Since then, as I have written about in my previous article “Block’s Start-Up Ecosystem Will Drive Growth”, the company has expanded to the Cash App, TBD, Bitkey, the Mining Development Kit, C=, and more with Jack Dorsey still serving as “Block Head”.

Seeking Alpha

Not only do the founders own a significant amount of shares, but they also have a majority voting power. Combined, Dorsey and McKelvey have a voting power of 52.4%. The dual-class share structure significantly increases the founder control or founder “energy” within the company, which could be the leading factor as to why Square changed its name to Block and why Block is now pursuing several Bitcoin-related startups.

Three more notable mentions from the list below are Amrita Ahuja, Brian Grassadonia, and Alyssa Henry. Amrita owns around 206k class A shares and she is the company’s CFO and even more recently CFO + COO (Seeking Alpha Transcripts). Brian leads the Cash App business and he owns a total of ~1.4 million shares outstanding, of which more than half of the shares have class B voting power. Lastly, Alyssa owns a total of ~909k shares of which around 17% have class B voting power. Both Alyssa and Brian have worked at Block Inc for more than 9 years and almost 13 years respectively, while Amrita has worked for almost 5 years. This is most likely the reason why the COO/CFO has a smaller number of outstanding shares, though this is likely to grow over time.

Block Inc Proxy Filing 2022

To conclude, I rate Block Inc a 9/10 on the insider ownership scale because of its owner-driven nature as well as the very long tenures of the company’s senior executives. To me, both of these are good signs, especially the latter. The only downside, however, is that the two founders 2.5% of shares outstanding away from losing majority voting rights which poses a risk for the company to continue pursuing innovative startups from within.

Share Repurchases

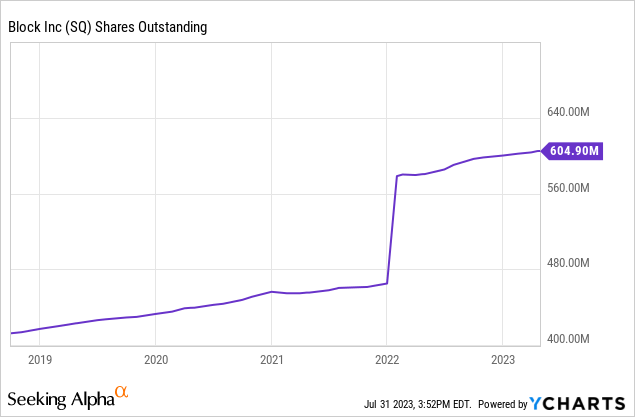

Block Inc’s shareholders have been diluted by a huge 40.5% since 2019 and about 31.3% since 2021. The company’s share count evidently spiked upward on the beginning of 2022, and this is due to Block’s acquisition of Afterpay.

“In connection with the acquisition, the Company issued 113,617,352 shares of the Company’s Class A common stock… The aggregate fair value of the shares issued was $13.8 billion based on the closing price of the Company’s Class A common stock on the acquisition date”

(2022 10K)

In essence, investors should think about the share issuance as trading ownership for a new larger organization. If an investor thinks that the acquisition will improve the company’s future performance and product offering, then he/she can be happy with the acquisition with this type of financing structure. However, if he/she is not satisfied then this method can be seen as exceptionally costly. One particularly worrisome metric regarding this acquisition is that 84.7% of the purchase price was allocated to goodwill, a.k.a the residual intangible value paid. In a research paper, which I co-authored, we found in aggregate that the more purchased goodwill an acquirer pays for the worse its one-, two-, and four-year stock returns. In our sample of over 700 acquisitions from various industries in the U.S., the mean goodwill percentage of the purchase price was 50% – well below Block Inc’s purchase premium (Does Purchased Goodwill Create Shareholder Value?). Hence, I am skeptical with regard to large goodwill premiums on average. But, since Block Inc’s own stock was incredibly highly valued during the time of acquisition it did not need to sacrifice as many shares to purchase Afterpay as it would have otherwise done. In conclusion, with the rigid guidelines of the 10-bagger rating list, Block scores the lowest yet 1/10 with regard to share repurchases.

Gross Profit Margins

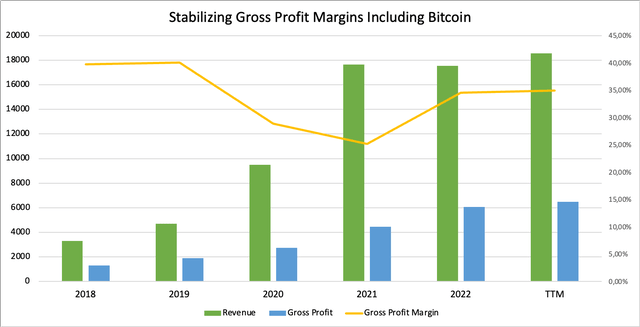

When analyzing Block Inc, analysts typically evaluate financial ratios both including and excluding the company’s profit made from brokering Bitcoin. For some brief context, Cash App began allowing the option to buy and sell Bitcoin on the platform. Cash App takes a fixed 2% fee for customers that wish to buy Bitcoin, which equates approximately to the company’s 2.3% gross margin on Bitcoin sales (Q1 2023). Now, the reason why analysts exclude Bitcoin contributions in the analysis is that it makes up such a large portion of the company’s revenue, for example, 40.6% of the company’s revenue (“TTM”), which distorts all sorts of margins.

When including Bitcoin revenue, Block has seemingly decreased its gross margins by around 5% over the past 5 years. Gross margins experienced especially aggressive declines during 2020 and 2021 when Bitcoin revenue took off. Over time, though, the company’s total gross margins have stabilized.

The Author

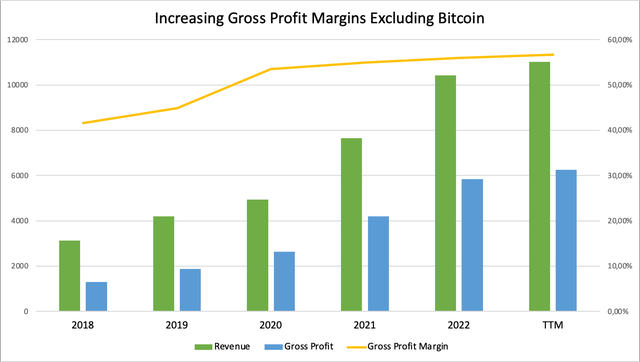

Below is a more accurate graph, representing the underlying trend of Block Inc’s business. The first observation we can make is that revenue is growing more steadily than it first seemed when including Bitcoin sales. Furthermore, in this graph, gross margins have expanded quite dramatically over the past five years. In fact, gross margins have grown from 41.58% in 2018 to 56.72% in the “TTM”, which equals a 15.15% gross margin gain. This is even higher than Enphase’s margin expansion of 13%, discussed in “The Hunt For Potential 10x Returns: Enphase Is Growing Its Market, Very Profitably”, which motivates me to give Block Inc. a 10/10 rating with regard to gross margins.

The Author

Intangibles

| Intangible Asset | Rating |

| Company Culture | 9 |

| Industry Growth Rate | 10 |

| Operating Leverage | 7 |

Average Points: 8.7

1. Company Culture

From following Block for a few years, I have gotten the general impression that Block is a relatively flat organization that promotes innovative projects. It seems that Jack Dorsey takes on roles he enjoys and is interested in developing (currently TBD) and leaves complete autonomy to the company’s business unit leaders. The general guideline that he and other executives have for the business is that all business units are built to work together. Recently, Dorsey was asked what Block Inc’s competitive advantage is and he answered that it was the company’s unique ecosystem – that creates resiliency – and that will one day work very coherently (2023 Shareholder Meeting).

Another impression that I get is that despite the flat organizational structure, employees and executives are guided by stringent financials. Since two quarters back, the company has been shifting toward evaluating its managers based on the rule of 40 and gross profit retention (Seeking Alpha Transcripts). In return, the company wants to be evaluated by its shareholders based on this measure. I speak of this in more detail in my article “Block: What To Look For And What To Disregard In Q1”, but in short the reason for this is as Jack describes:

“The principles that led us to this framework were; Number one, ensure our investments are focused on customer retention and growth. Number two, account for ongoing costs of the business including stock-based compensation. And number three, utilize industry standard conventions that are simple to communicate and understand. We will not be distracted from living up to these principles and building our business according to this framework.”

The final impression I would like to mention is the company’s transparency and encouragement of open protocols. First, Block issued very detailed and transparent user data which killed part of Hindenburg’s short report (Seeking Alpha News). Second, the company’s business unit focused on decentralized identity, TBD, continually updates its progress through its website. Lastly, the TBD team is focused on contributing to an open standard for decentralized identity on the web. Currently, the business has easy ways for developers to create decentralized identity stores for its users.

Block’s open, goal-oriented, and compliance-rich culture motivates me to give the company a 9/10 with regard to company culture.

2. Industry Growth Rate

To be honest, it’s not very easy to determine Block’s industry since the company’s scope is broad. One unique industry is merchant acquisition through POS systems – which is easily definable – but already once we try to segment Cash App into a certain industry, things become more difficult. Cash App derives profit from its debit card, direct deposit, consumer loans, business accounts, stock and bitcoin trading, as well as advertising. Furthermore, Block has a developer-oriented business called TBD, a self-custody wallet provider called Bitkey, Tidal, Afterpay, and even more projects in development.

Given the complexity of the company’s business, I have created gross payment volume estimates below for the company based on historical growth rates, coupled with market sizing data made by Block in order to determine its industry growth potential.

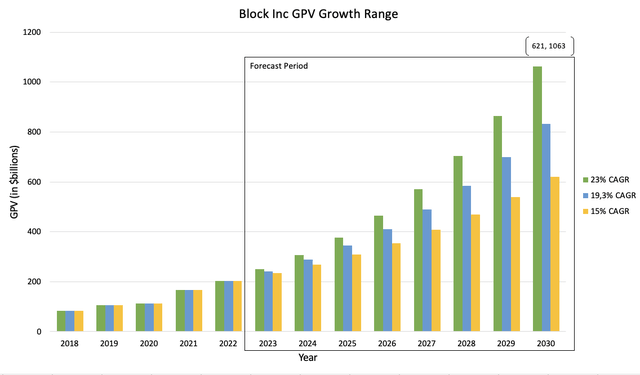

Gross Payment Volume (“GPV”) Estimates

One of the largest drivers of Block Inc’s growth is the gross payment volumes (“GPV”) that flow through its ecosystems. In 2022, the company disclosed a total “GPV” of $203 billion spread between Square ($186.5 billion) and Cash App for business accounts ($16.5 billion).

Since 2018, Block has historically grown its “GPV” at a compounded annual growth rate of 19.3%, which is used to forecast the blue line. Since it is uncertain whether or not the company will continue growing at this rate, I have also included a scenario where compounded annual growth is 15% and 23%. Given this range of scenarios, we can expect Block to achieve a “GPV” of between $621 and $1.063 billion in 2030.

The Author

In the most recent quarter, Block achieved a net take rate (transaction-based gross profit / “GPV”) of 1.135% (Block Q1 Shareholder Letter). This means that the company retains this percentage on the total volumes processed through its Square and Cash App for Business ecosystem. Given the “CAGR” estimates and a constant net take rate, we can expect Block to earn between $7-12 billion in transaction gross profit in 2030. For reference, the company earned $2.4 billion in transaction gross profit for the “TTM”.

The continued growth in “GPV” is dependent upon general growth in spending, and growth in merchant adoption. Given that the company continues expanding abroad and gains a stronger base of mid-size and large sellers, I believe that at least the lower range is achievable. Currently, Block is selling for an 18.75x transaction-based gross profit to market cap multiple. Given that transaction-based gross profit rises to $7 billion in 2030 and the multiple remains constant, the company will trade for around $131.25 billion.

However, “GPV” does not make up the entirety of what drives Block’s valuation. In fact, Block appreciated that Cash App’s total addressable market “TAM” was $70 billion and Square’s “TAM” was $120 billion in 2021 during investor day. These “TAM” figures were not based on revenue, but rather on gross profit. Therefore, $7-12 billion in gross profit in 2030 from transactions seems small in comparison to the company’s goals. For instance, one of the largest income streams for Cash App is its debit card, which is accounted for under subscription revenue.

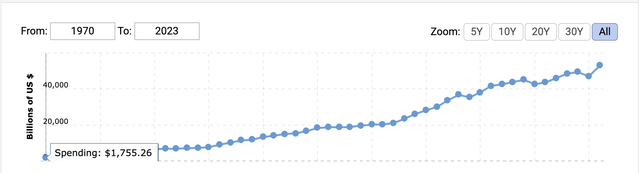

To conclude, I believe that Block has an impressive runway to growth because the majority of its businesses operate within an industry contingent upon consumer spending. Since 1970, worldwide consumer spending has increased from $1,7 trillion to nearly $53 trillion in 2021. A 7% “CAGR” tailwind (the historic growth, which is likely to continue) sets the company up for natural success. Furthermore, the company is known for expanding into new industries – such as Cash App, TBD, Bitkey, etc. – which steadily increases its market potential. For these reasons, I rate the company’s industry growth rate a 10/10.

Macrotrends.net

3. Operating Leverage

History

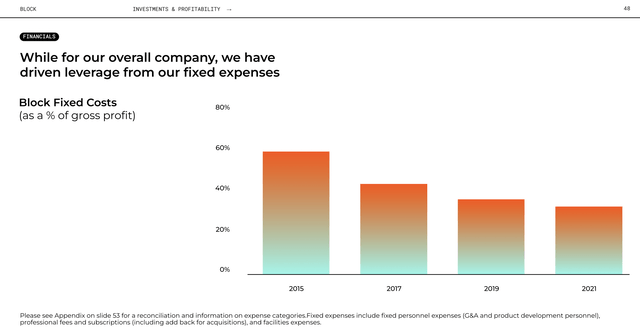

Block Inc has a history of driving operating leverage within the business. Below is a graph displaying Block’s fixed costs as a percentage of gross profit. Since the company’s IPO, fixed costs as a percentage of gross profit have decreased from 59% to 31%.

Block Inc Investor Relations

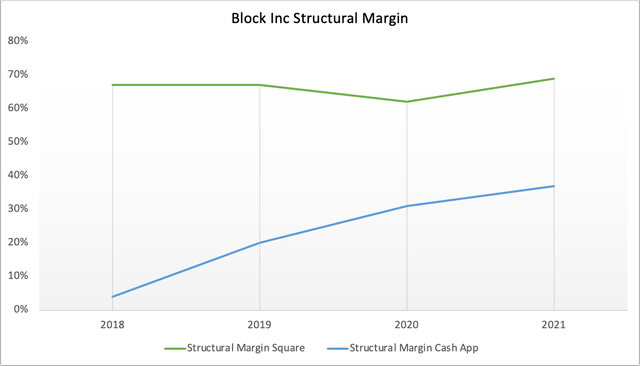

When breaking down Square and Cash App’s ecosystems separately, the company discloses the following: Square’s structural margin (gross profit – variable expenses) was 69% (up from 67% in 2018) and its fully burdened margin (add fixed expenses) was 34% in 2021; Cash App’s structural margin was 37% (up from 4% in 2018) and its fully burdened margin was 12% in 2021 (Block Inc Investor Day: Business Model). Cash App’s ability to grow its structural margin has been proven over these past five years, but unfortunately, the company does not have any historical data on the fully burdened margin. This makes gauging prior operating leverage more difficult, but we can nonetheless see from the above figure that the company has efficiently utilized its fixed investments.

The Author

Looking Forward

Going forward, I believe Block will be able to drive even more operating leverage from within its ecosystems. This will, in the largest part, likely be done with the three following components.

- Higher adoption of closed-loop transactions

- High utilization of Cash App as an advertising platform

- SaaS expansion with Square merchants

Closed-Loop Ecosystem

Currently, each time an out-of-ecosystem transaction is made at a Square terminal or with a Cash App business account, Block is required to pay third parties for interchange, processing, assessment, and bank settlement fees. However, when transactions are all made within the ecosystem, Block is able to avoid these costs and hence retain more profit. In 2022, the company’s net take rate (transaction-based gross profit / “GPV”) was 1.15% – but Ark Invest sees a scenario where close-looped economics drive the net take rate to 2.60%. This would more than double Block’s gross profit, without the company needing to invest in many fixed operating expenditures. In the most recent quarter, the company’s net take rate amounted to 1.135%, a slight decline from the previous year. However, Block has one concrete goal that could accelerate a closed-loop adoption. Namely, Jack Dorsey said, at JPMorgan’s 51st Annual Conference:

“And within the app, we have this new area, which is super clunky right now called Discover that people right now are just using to find the people they previously paid or the people that they want to pay in their address book, but eventually will be the merchants around them, mostly Square merchants around them.”

As the Cash App becomes more fine-tuned, Square merchants will be able to connect with consumers through Cash App. This, in turn, will likely encourage consumers to use the Cash Card or Cash App’s QR code at the checkout of more Square merchants. Block really has a unique opportunity to build a fun app for consumers, where it can offer Boosts (discounts) for example, in order to incentivize closed-loop adoption.

Cash App Advertising

Cash App’s advertising business is still nascent and I believe it can contribute with significant operating leverage. At the same conference mentioned above, Jack Dorsey mentioned his goal for Cash App:

“making it relevant so that people want to go there every single day. And that’s ultimately what we’re going to judge ourselves on is, have we created a new tab that people want to visit every single day because they find something that they want to engage with or they want to purchase. And this is not a new path. This is a well-trodden path. This is a search engine, but mirroring it with our data. And then you can imagine other models within that, including advertising, where I can pay for placement within that?“

(My italics)

The most important part of this is the advertising model mentioned in the end. Once the company removes the ‘clunkiness’ in the app, I believe they will be able to create a great-looking (Cash App is known for its simple user interfaces) Discover tab where retail companies will advertise themselves. Currently, the company works with both fixed fee placements and variable fee payments for traffic that Cash App brings to a retailer’s website. Cash App is off to a good start, giving customers highly relevant deals (Chipotle, McDonalds, Starbucks, Carhartt, etc.) coupled with its new gift card feature. I look forward to seeing further development of the app that will enable a full-fledged advertising business.

SaaS Expansion with Square Merchants

The final driver of operating leverage that I can imagine for the foreseeable future is the expansion of SaaS subscriptions among Square merchants. Currently, Square is moving upmarket to medium and large-size sellers. The company started by selling to small businesses, where the company has a significant market share in the U.S. – 13% micro-businesses & 4% SMBs in 2021 – according to its investor day market opportunity presentation. In stark contrast, the company, at that time, had only penetrated 0.5% of the mid-market. I believe that Square’s focus on larger sellers will be coupled with higher SaaS sales because these larger chains are in need of more robust software tools to drive their businesses successfully. In 2022, Square achieved subscription-based revenue amounting to $1.3 billion, which was a huge jump from $664 million in the year prior. These software products, which range from managing payroll and invoices, and driving marketing campaigns, to enabling customer support and loyalty programs, all have high margins which enable some operating leverage. The caveat with these products, however, is that Block needs to spend a good amount on product development in order to bring these solutions to market. And since competition is so intense within this industry – with Shopify (SHOP), Toast (TOST), Fiserv’s Clover (FI), and PayPal (PYPL) – the company can’t stop spending on product development (Note that product development was the only cost that increased YoY during the previous quarter).

Given the company’s history as well as its modest potential to continue driving operating leverage going forward, I rate the company a 7/10 for this metric.

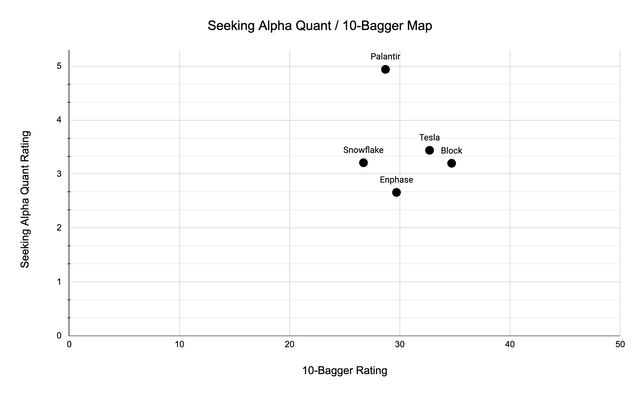

10-Bagger Rating & Seeking Alpha Quant Map

What follows now is a map continuously plotting the companies I analyze based on my 10-bagger rating and Seeking Alpha’s quant rating. This allows us to gauge different companies’ performance over time.

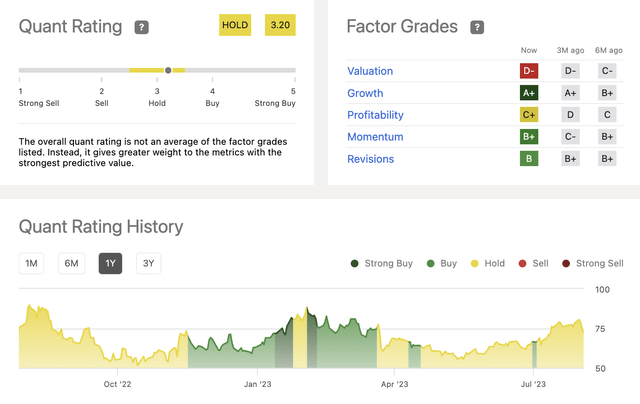

Block Inc. Quant Rating: 3.20/5.00

Seeking Alpha

Rating Map

In this analysis, I find that Block scores a record 34.7/50 on the 10-bagger scale and a 3.20/5.00 with Seeking Alpha’s quant rating. Seeking Alpha finds, like me, that the company has just ok profitability and a relatively crazy valuation (expanded upon below) but has delivered incredible growth (rating it with an A+).

The Author

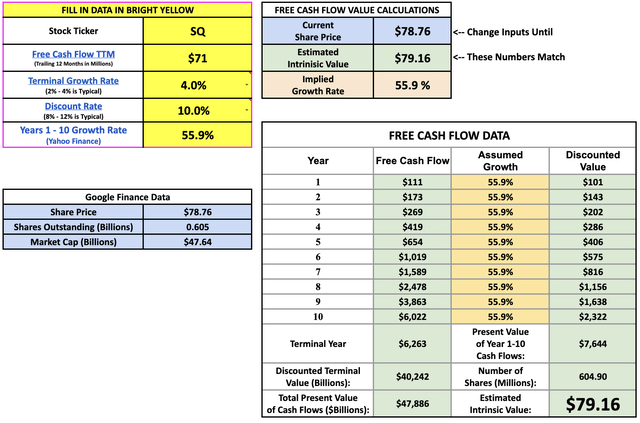

Valuation

At first glance, it seems that Block’s valuation is extremely out of line. This is due to the fact that the company’s “TTM” free cash flows have been unusually low. In contrast, in 2021, Block achieved a free cash flow of $713.5 million, which is 10x the recent amount. For this reason, the company needs to grow free cash flows by 55.9% for the next ten years in order to justify its current valuation.

To make the valuation more concrete, I have summed the first 10 years of cash flows, which amount to $16.4 billion. The question is whether Block is able to achieve these types of cash flow over the next ten years. This would be a daunting task considering the company’s historical free cash flow. However, it could be doable given that Cash App and Square drive further operating leverage and Block’s new business units move from the seed phase to high growth. Although the reverse free cash flow method of valuation may not be generally suitable for this company that is not focused on free cash flow generation – I believe it’s useful from two standpoints. One, it gives some perspective as to what cash flows will be expected for the company in the long term. Second, it seems like Block is moving toward maturing its business through for example the rule of 40, which indicates that cash flow will become more important.

Brian Feroldi/Stoffel/Withers

To conclude, I reiterate my buy rating for Block Inc as it has scored a historically high 34.7/50 on the 10-bagger scale supported largely by strong intangibles, an incredible gross margin expansion, and a founder-led team, though offset by poor share dilution and medium returns on invested capital. Thank you for reading, if you have any comments drop them down below and follow to expect more hunts for potential 10x returns.

Read the full article here