Intro

WW International, Inc. (NASDAQ:WW) is a global provider of weight management products and services. The company operates in four segments: North America, Continental Europe, United Kingdom, and Other. It offers a wide range of nutritional, activity, behavioral, and lifestyle tools and approaches to support weight management.

WW also provides digital subscription products, including personalized resources and coaching through its app and web-based products, fostering a supportive community for members on wellness journeys. Additionally, WW offers consumer products like bars, snacks, cookbooks, and kitchen tools. The company also licenses its trademarks and intellectual property in relevant consumer products and services, and provides publishing services. WW’s products are available through e-commerce platforms and partner channels.

In this analysis, we will closely evaluate WW’s financial performance and growth prospects. We’ll delve into the company’s revenue, profitability, and cash flow generation capabilities. By gaining insights into these essential aspects, investors can make a more informed assessment of WW’s potential as a favorable investment in the current market.

Lack of Growth and Profitability

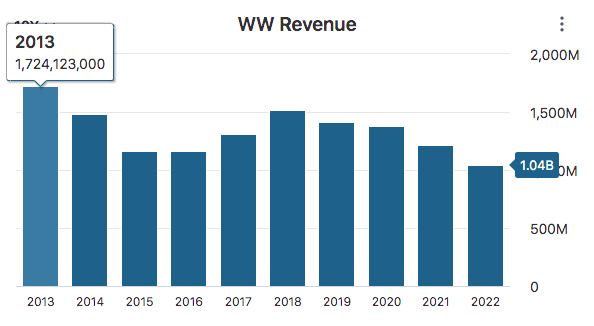

Over the past ten years, WW has faced some significant challenges with its financial performance. The company’s revenue has been decreasing year after year. In 2013, they made around $1.7 billion, but by 2022, that number dropped to only $1 billion. This represents a compounded annual growth rate of -4.92% and total decline in revenue of 39.6% over the decade.

Data by Stock Analysis

Similarly, the company’s free cash flow has also been declining sharply. In 2013, they had about $261 million, but in 2022, it was reduced to just $38 million. This steep decline represents a -17.4% compounded annual growth rate over the last ten years.

Data by Stock Analysis

The negative trends in both revenue and free cash flow for WW can be attributed to several key factors that have impacted the company’s competitive position and appeal to consumers. Firstly, WW has faced stiff competition from other weight loss programs in the market, such as Jenny Craig, Nutrisystem, and Noom. These alternative programs offer similar services to WW but often at more affordable prices. Consequently, WW has struggled to retain and attract customers in the face of this heightened competition which has also affected the company’s overall profitability.

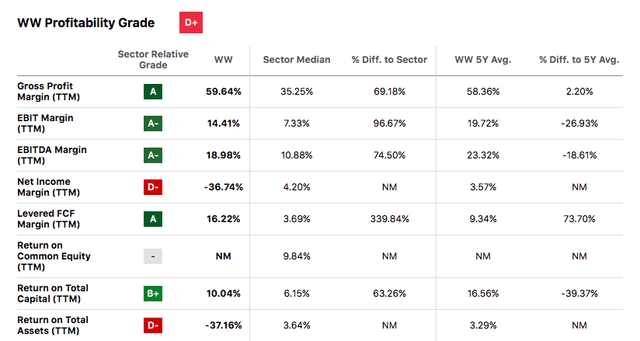

While WW has nice comparisons to consumer discretionary sector median in gross margins, EBIT margin, and EBITDA margins, overall WW is less profitable than its peers, earning a Seeking Alpha profitability grade of D+.

Data by Seeking Alpha

WW’s poor profitability metrics can be attributed to the company’s outdated point system that is losing traction with consumers. Moreover, consumer preferences have been shifting towards personalized and data-driven weight loss programs. For example, other programs like Noom leverage artificial intelligence to track users’ progress and provide personalized recommendations, aligning with the latest trends in weight loss. As a result, WW has faced challenges in keeping up with these evolving consumer demands, impacting its ability to effectively appeal to a broader audience.

Outlook

The earnings estimates for WW suggest that the company is likely to face financial challenges throughout the rest of 2023. WW is projected to report negative earnings per share (EPS) of $-0.10. This would be the second consecutive year that WW reports negative earnings, highlighting the struggles the company has been going through.

In terms of revenue estimates, WW is expected to generate around $919.41 million for the same fiscal period ending in December 2023. However, there is a negative year-over-year (YoY) growth projection of -11.67% for revenue.

Data by Seeking Alpha

There are a number of risks associated with investing in WW that are contributing to this negative outlook, namely the increase in competition and changing consumer preference. The weight loss industry faces challenges due to increasing competition and changing consumer preferences. New companies entering the market and existing players expanding operations have led to pricing pressure for weight loss companies like WW.

However, it’s worth noting that WW has a strong reputation in the weight loss industry. Their program has been consistently ranked as the number one best diet for weight loss by US News and World Report for 13 consecutive years. This credibility provides a solid foundation for the business to build upon.

WW is making ambitious plans to turn around the company’s performance in 2023. They have identified key initiatives to shape the future of their product experience, operating model, and financial trajectory.

One of these important initiatives is the company’s focus on digital transformation. WW’s shift to digital has expanded its subscriber base, with 80% of members accessing their services via a mobile-first experience. By enhancing the digital experience, WW aims to bring people together in new ways, reach a broader audience, and provide immediate support and inspiration.

The company’s efforts have shown promising results. In the first quarter of 2023, WW achieved nearly 500,000 net additions of subscribers, while also optimizing marketing expenses with 18% less spend compared to the prior year.

Furthermore, WW’s recent acquisition of Sequence, a digital health platform offering clinical access to prescription weight management medication, represents an opportunity for significant growth in improving health outcomes. We believe this strategic move allows WW to expand its offerings and positively impact more lives in the future.

Valuation

To assess WW’s intrinsic value, we will use the discounted cash flow (DCF) analysis. Beginning with WW’s starting free cash flow of $38.39 million, we will apply an initial growth rate of -11.67% for 2023, followed by growth rates of 12.21% for 2024 and 13.32% for 2025 based on the average analyst estimates of revenue growth for WW over the next few years.

For the subsequent period, we will use a conservative growth rate of 5.00% for years 4-10, considering potential industry trends and WW’s strategic initiatives. With a discount rate of 10%, based on the average return of the market with dividends reinvested, and a conservative perpetual growth rate of 2.5%, we calculate the intrinsic value of WW to be $8.62. This suggests that WW might be currently priced at fair value, presenting investors with neither a potential return or loss compared to the company’s current market price.

Author’s Work

Final Thoughts

Based on the analysis, it is advisable for investors to hold their current positions in WW and wait for a more attractive price before considering buying additional shares. The company has faced challenges in its financial performance, with declining revenue and profitability over the past decade. Increased competition and changing consumer preferences have impacted WW’s ability to retain customers and remain profitable.

The earnings outlook for 2023 indicates that the company is likely to face continued financial challenges, with negative earnings per share and a decline in revenue projected. While WW has a strong reputation in the weight loss industry, it has struggled to keep up with evolving consumer demands, particularly in the digital space.

WW’s strategic initiatives aim to address these concerns, with its focus on digital transformation and recent acquisition of Sequence, there is potential for growth and improvement. However, the current valuation analysis suggests that the stock may be priced at fair value, offering neither significant upside potential nor substantial downside risk.

As a result, holding the stock at its current market price and closely monitoring WW’s performance and strategic developments for signs of improved growth and profitability may be a prudent decision for investors. Waiting for a more attractive price and more promising growth prospects before considering further investment may lead to a more favorable risk-reward profile for potential shareholders.

Read the full article here