One of the most fascinating things to watch in the market is a company that continues to achieve attractive fundamental performance but that simultaneously underperforms the market from a share price perspective. This does make sense when the company in question is expensive. But when it is incredibly cheap, it defies logic. One firm that has experienced this kind of illogical price movement in recent months is the small retailer known as Village Super Market (NASDAQ:VLGEA). Revenue, profits, and cash flows are all coming in well. Even so, the stock has underperformed the broader market for more than half a year now. To some investors, this may be viewed as a time to move on and focus on returns elsewhere. But for those who are truly value oriented and who have a long-term investment horizon, it may make more sense to back up the truck and purchase additional units.

Recent performance has been fine

The last article that I wrote about Village Super Market was published in early December of 2022. In that article, I discussed how the company held up well in what was then the current environment. In fact, from the time I had written about the business one year earlier until that date, shares had experienced upside of 9% compared to the 13.5% decline the S&P 500 saw. At the time, there was no evidence that this attractive performance would cease. And when I looked at how cheap the stock was even after rising, I had no reason to rate the company anything worse than a ‘buy’. Since then, we have seen a reversal of fortunes. The S&P 500 has shot up 14.3% while Village Super Market has seen its stock tick down 0.8%.

Author – SEC EDGAR Data

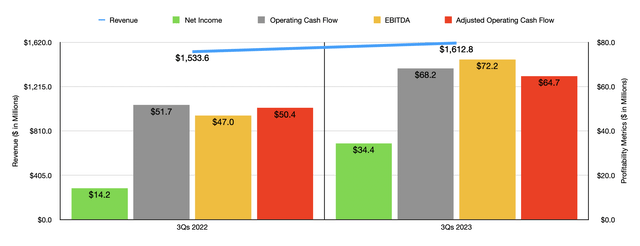

You would think that such a return disparity would have been driven by fundamental reasons. But from what I can tell, that’s not possible. Consider how the company performed during the first nine months of its 2023 fiscal year. During that time, sales for the firm came in at $1.61 billion. That’s 5.2% above the $1.53 billion reported one year earlier. The primary driver of the increase, then, was a 3.6% rise in comparable store sales. The company also benefited from the opening of a Gourmet Garage in the West Village in Manhattan, New York. Plus it enjoyed higher sales due to the remodel and conversion of one of its other locations in New York.

On the bottom line, the picture also improved. Net income more than doubled from $14.2 million to $34.4 million. Although the increase in revenue certainly helped on this front, the biggest driver behind the improvement was a decrease in the company’s operating and administrative costs from 25.1% of sales to 23.8%. This improvement, management said, was driven largely by lower labor costs and fringe benefits, as well as decreased supply spending. Other profitability metrics for the company also showed year over year improvements. Operating cash flow, for instance, grew from $51.7 million to $68.2 million. On an adjusted basis, it expanded from $50.4 million to $64.7 million. And finally, EBITDA for the company jumped from $47 million to $72.2 million.

Author – SEC EDGAR Data

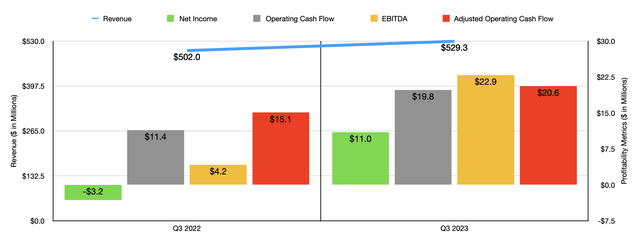

A nine-month window is a long period of time, particularly in this economic environment. So it would be helpful to look at the most recent data to see whether any negative changes have been occurring. So far, they haven’t. Revenue in the third quarter of the 2023 fiscal year, the most recent quarter for which data is available, totaled $529.3 million. That’s an increase of 5.4% over the $502 million reported one year earlier. Again, a comparable store sales increase of 3.4% did the heavy lifting here. But the other aforementioned changes also helped the company. A plunge in the company’s operating and administrative costs from 27.4% of revenue to 24.3%, driven by the same factors that helped the company for the nine months as a whole, pushed the business from generating a net loss of $3.2 million in the third quarter of 2022 to generating a profit of $11 million the same time this year. Operating cash flow almost doubled from $11.4 million to $19.8 million, while the adjusted figure for this expanded from $15.1 million to $20.6 million. And finally, EBITDA for the company grew from $4.2 million to $22.9 million.

Author – SEC EDGAR Data

We don’t know what to expect for the rest of the fiscal year. But if we annualize results experienced so far, we would expect net income of $64.9 million, adjusted operating cash flow of $93.1 million, and EBITDA of $113.2 million. Using these figures, we can easily value the company. In the chart above, you can see that the firm is trading at a forward price to earnings multiple of 5.3. The forward price to adjusted operating cash flow multiple is 3.7, while the EV to EBITDA multiple is 2.9. These numbers are all more attractive than if we were to use the data from 2022. As I do with other companies that I analyze, I also decided to compare Village Super Market to five similar firms. These can be seen in the table below. Using the price to earnings approach, the price to operating cash flow approach, and the EV to EBITDA approach, I found that Village Super Market was the cheapest of the six firms across the board.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Village Super Market | 5.3 | 3.7 | 2.9 |

| Natural Grocers by Vitamin Cottage (NGVC) | 17.6 | 6.1 | 5.3 |

| The Kroger Co (KR) | 13.5 | 5.4 | 4.0 |

| Grocery Outlet Holding Corp (GO) | 48.5 | 13.8 | 18.9 |

| Sprouts Farmers Market (SFM) | 16.5 | 10.3 | 6.5 |

| Casey’s General Stores (CASY) | 20.4 | 10.3 | 10.9 |

Takeaway

Based on all the data that I have in front of me, I remain perplexed. I don’t frankly understand why shares of the company are currently underperforming the broader market by such a large extent. That stock is cheap, both on an absolute basis and relative to similar firms. Even though I didn’t mention this earlier in the article, the company also has cash that exceeds debt by $16.4 million. That makes it a very low risk prospect from a solvency perspective. Revenue, profits, and cash flows are all climbing year over year. Everything is lining up nicely. My own view is that this is just one example of the market being irrational. And for those who don’t mind experiencing volatility in the near term, I would argue that the reward on the other end of the trade will likely prove to be quite attractive.

Read the full article here