So-Young International Inc (NASDAQ:SY) operates an online platform connecting consumers with beauty industry professionals in China. Beyond information and reviews on a wide range of treatments, the company’s business model centers on the service providers marketing their procedures with tools for managing online reservations. So-Young also sells equipment including beauty photonic and laser devices for both at-home and clinical settings.

The idea here sounds compelling with data suggesting China’s aesthetic market including medi-spa treatments, cosmetic surgery, and general consumption healthcare remains a high-growth segment.

That being said, the recent results from So-Young have left a lot to be desired. Getting past the pandemic disruptions, revenues are down alongside a decline in key operating metrics from recent years. While there is anticipation for some stronger trends going forward, we’re skeptical of a sustained rally in the stock price and expect shares to remain volatile.

SY Key Metrics

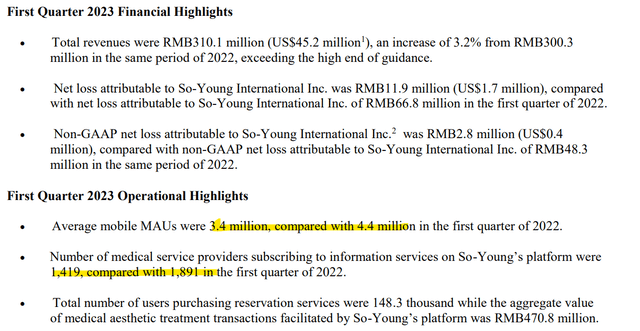

The company last reported its Q1 results in May with a headline GAAP earnings per American Depositary Shares (ADS) loss of -$0.02, representing -$1.7 million in negative net income. Revenue of RMB 310 million, or approximately $45.2 million, climbed by 3.2% from the period last year, but also down sequentially from the prior quarter.

Within the results, core revenues from “Information Services”, contributing about 70% of the business, climbed by 9.2% y/y, which helped balance a -29.9% decline in reservation services. The smaller segment of Equipment Sales posted a 7% increase.

Considering the period in 2022 which was defined by lingering pandemic disruptions at the time, our interpretation is that the figures are soft compared to a stronger rebound in other segments of the Chinese economy.

Management guiding for stronger trends going forward, citing what has been a slow recovery in the surgical transactions, at least within the company platform. For Q2, the company is targeting total revenues between RMB 380 and RMB 400 million, representing an annual increase between 23% and 29% year-over-year. Objectively, that’s a solid growth rate by any measure, but the greater concern comes down to what we see as poor operating metrics, in our opinion.

source: company IR

Soft Operating Trends

Indeed, it appears the company’s “brand momentum” has lost some traction, considering the average monthly mobile users at 3.4 million in Q1 was down from 4.4 million in the period last year. Similarly, the number of service providers’ “business customers” on the platform declined to 1,419 from 1,891 in Q1 2022.

From the company’s annual report, So-Young captured a peak number of average mobile MAUs of 8.1 million, meaning the business is seeing less than half the number of visitors at its peak. Other metrics tell a similar story. The number of users purchasing reservation services in Q1 at 148.3 thousand compares to 173 thousand in Q1 2021, for example.

We bring up the trends because they raise questions regarding why users are leaving and if they will come back. Naturally, there are many other channels for potential aesthetic patients to find service providers, and the challenge for So-Young is to demonstrate their platform offers a compelling service and value proposition.

What’s Next For SY?

When looking at So-Young, it’s clear there are some mixed signals. The history has been poor, and the last quarter was soft, but guidance is turning better. We can also bring up the strong balance sheet, with the company reporting a total liquidity position of $215 million in the last quarter against effectively zero debt. Still, that might not be enough to send the stock higher.

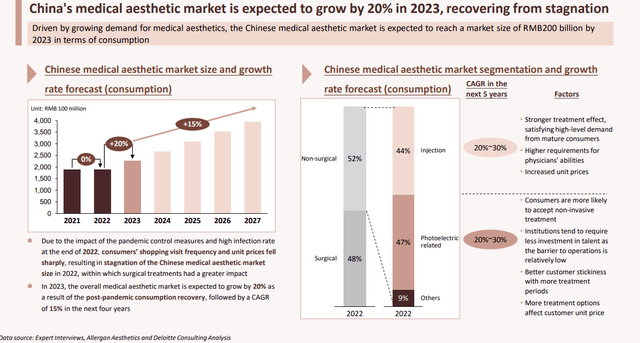

According to the consulting firm “Deloitte”, China’s medical aesthetic market is expected to grow by 20% in 2023 and average an annual rate of 15% through 2027.

The question is where So-Young finds itself within that graph and how successful it will be in capitalizing on those trends next to alternative consumer options. The same report cites favorable country demographics with momentum in non-invasive procedures. That should be right up the company’s alley, but we simply haven’t seen enough to suggest they are benefiting.

source: Deloitte

What we’d like to see is an expanding pie of users with stronger MAUs and transaction volumes as evidence of a healthier ecosystem. In our opinion, the ability of management to turn those operating trends around is more important than short-term sales variance.

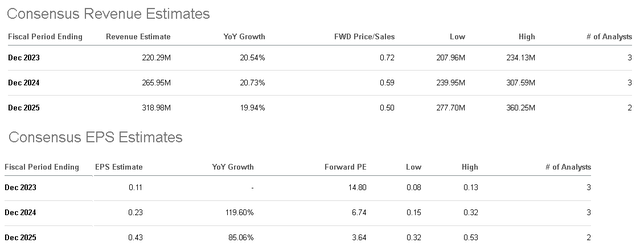

According to the consensus estimates among three published Wall Street analysts, SY is expected to turn profitable by year-end, with sales re-accelerating toward a 20% growth rate through 2025.

While some may look at SY trading at a forward P/E of 15x and even 7X by 2024 as an attractive valuation, our opinion is that the multiples reflect more of a “value trap” taking those projections with a grain of salt. We’ll believe it when we see it.

Seeking Alpha

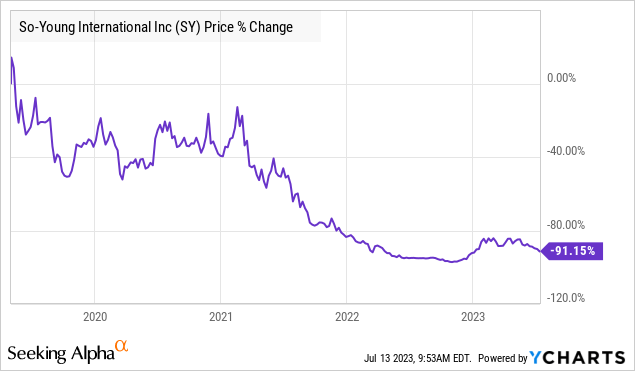

SY Stock Price Forecast

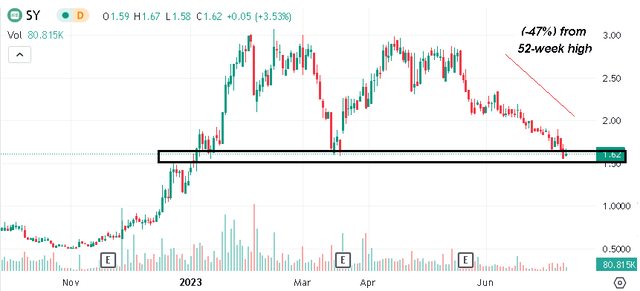

We rate SY as a hold, representing a neutral view of the stock in the near term. The position considers that shares of SY are already down 50% from its recent high in April suggesting technically oversold conditions, approaching an important area of technical support at around $1.50 per share.

While we wouldn’t be surprised at a bounce from here, our full analysis takes a longer-term outlook over the next 6–12 months where the upside is far from certain. What investors can expect is continued extreme volatility given the many uncertainties on the table.

The risk here is that the next few quarters continue to underperform, which could play out depending on shifting macro conditions. Monitoring points include the operating metrics along with profitability margins. On the upside, the ability of the company to confirm a path to sustained profitability and a high growth profile would be bullish for the stock.

Seeking Alpha

Read the full article here