Advance Auto Parts (NYSE:AAP) finds itself in a tough position trying to navigate margin improvement and a tough competitive price environment during a period of still pretty high inflation.

Company Profile

AAP is an aftermarket parts automotive provider that serves both professional and do it yourself (DIY) customers. The company sells brand name, OEM, and its own brand automotive replacement parts through psychical stores and branch locations, as well as through e-commerce sites. Professional customers represented about 59% of its sales in 2022.

The company operates stores and branches under several names. It has over 4,400 stores under the Advance Auto Parts brand, including over 300 hubs. These stores serve both professional and DIY customers and carry about 23,000 SKUs. It also owns 330 Carquest stores and serves over 1,300 independently owned stores that operate under the Carquest name. The concept carries about 25,000 SKUs and caters more to professionals.

Its Worldpac concept, meanwhile, has over 300 branches, some of which are branded as Autopart International. It services primarily professional customers and has over 285,000 SKUs. It specialized in imported OEM parts.

Opportunities and Risks

It’s been a difficult year for AAP, with the stock down over -50% this year. Awful Q1 earnings, reduced guidance, and a slashed dividend led the stock to decline -39.3% the session following its Q1 earnings report.

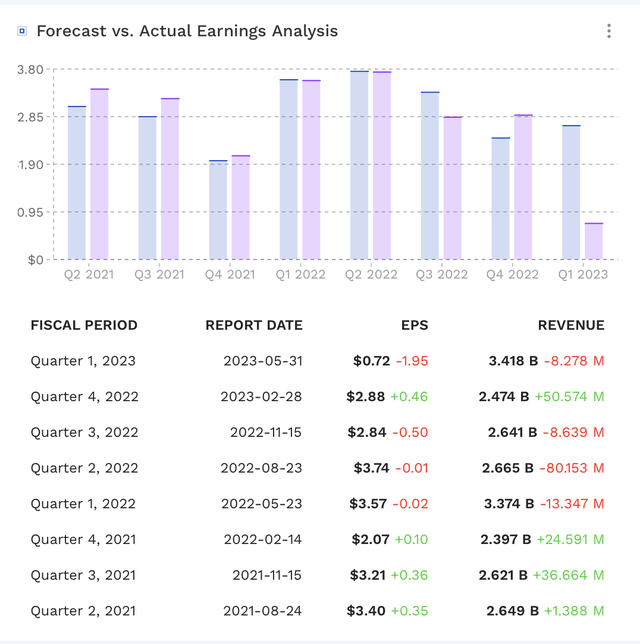

AAP has had difficulties hitting guidance in recent quarters, missing revenue and EPS estimates 4 of the past 5 quarters. From a revenue perspective, the Q1 miss was actually the smallest, missing the consensus by just $8.3 million against $3.4 billion in sales. However, EPS of 72 cents badly missed analyst expectations for EPS of $2.67.

AAP Earnings Vs Estimates (FinBox)

First-quarter sales were a bit disappointing growing 1.3%, with comps down -0.4%. The company blamed lower tax refunds, which hurt the business in March, along with a milder winter which impacted cold weather sales. However, margins were the big culprit, both in Q1 and going forward.

Gross margins fell -162 basis points in the quarter and the company reduced its gross margin guidance by -250 basis points. Competition and pricing appear to be the two main culprits.

Earnings PR

On its Q1 earnings call, outgoing CEO Tomas Greco said:

“In terms of competitive pricing, we’ve talked in the past that based on our research, the most important criteria for an installer to make choices above their parts supplier starts with availability, followed by consistency of delivery and relationship. Pricing has historically been the third or fourth criteria for an installer. However, if the gap between our price and competitors becomes too wide, price becomes a bigger factor. Last year, we saw a relative price position within pro climb to unacceptable levels as a result of changing competitive dynamics surrounding price-related investments. We’ve done considerable work testing different price points across categories and geographies to determine the best approach to drive increased transactions and growth in our pro business. This work helped us refine price targets for each category relative to competition, be it a traditional competitor or wholesale distributor. As a result of improved availability, along with the investments we made within pro to achieve competitive price targets by category, we saw improved performance in both transactions and units relative to the fourth quarter. This was more than offset by less year-over-year growth in average selling price relative to the fourth quarter. In order to sustain our targeted competitive price position in Q1, we had less price realization than planned, which put substantially higher pressure on our product margin rate.”

Improving gross margins and winning back wallet share from customers will be the biggest opportunities for AAP going forward. For the former, the company plans to optimize its inventory. It will sell some products it is carrying in inventory at discounted prices to transition to alternative products that have higher margins. In many cases, this will be moving to higher-margin owned brands. However, this transition should have the opposite effect in the near term if it is discounting lower margin inventory to get rid of it.

To win back customer wallet share, meanwhile, the company’s prices will also have to become more competitive. Moving more to owned brands can also help on this front, and the company also plans to work with suppliers and to take a more holistic approach with strategic sourcing.

AAP will have to walk a fine line to regain margins and stay price competitive. Having pricing issues during a strong inflationary environment, meanwhile, is a double whammy. At the same time, Greco is set to retire at the end of the year, and a new CEO has not yet been named. Taking over in this environment, won’t be an easy task.

It appears that Genuine Parts (GPC), which I wrote about in March, is likely taking it to smaller companies like AAP. GPC has been making a lot of tech and analytics investments to make better decision on pricing. AAP will have to invest in these areas to catch up.

Outside of the competitive price pressure issues, the macro environment remains another potential risk. However, the automotive parts business does tend to be countercyclical, as if the economy weakens, people often tend to hold onto their cars longer, leading to more repairs.

Valuation

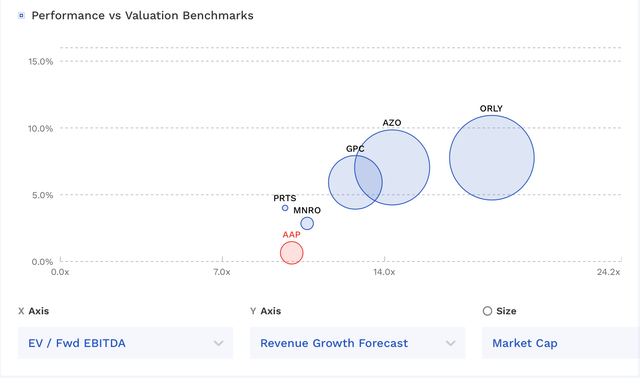

AAP trades at a 9.9x EV/EBITDA multiple based on the 2023 EBITDA consensus of $867.2 million. Based off of the 2024 EBITDA consensus of $905.1 million, it trades at around 9.5x.

On an EV/EBITDAR basis, it trades at 5.5x.

It trades at 12.3x forward EPS, with analysts projecting 2023 EPS of $5.78.

It’s projected to grow revenue under 1% in 2023, increase to 2% growth in 2024.

It’s one of the cheapest stocks among peers, but also one of the slowest growers.

AAP Valuation Vs Peers (FinBox)

Conclusion

AAP’s stock has taken a big hit, but it has a difficult line to walk to be able to compete on price and improve margins. At the same time, there is uncertainty regarding the company’s direction with its current CEO heading into retirement. Meanwhile, leverage is creeping up and the company slashed its dividend by -83%.

At this time, I’d prefer to pay up just a bit to get the larger, better run company in GPC. AAP could become a takeover target down the line, but that’s not something I’m going to bet on at this time. As such, I’m largely neutral on the name.

Read the full article here