In the past few days, I have written two articles on REITs. In both cases, I mentioned that I prefer REITs that come with a great mix of value and growth. While I do have a number of REITs on my watchlist, I currently own only two REITs. Both are self-storage operators.

One of them is Extra Space Storage (NYSE:EXR), which is now my third-largest investment, as I have kept buying its shares rather aggressively.

Unfortunately, the EXR stock price isn’t doing so well. Shares are down 4% year-to-date and roughly 38% below their all-time high.

I believe we’re dealing with a case of throwing the baby out with the bathwater. We’re seeing that rising rates and tremendous pressure on commercial real estate are causing investors to dump everything in the industry.

While that isn’t great for my current investment, which is down 9%, I’m happy that the market keeps giving me opportunities to buy this REIT at a yield of almost 5%.

In this article, I will update my bull case using favorable industry reports and the company’s strong earnings and comments, which include favorable credit developments.

So, let’s get to it!

Buying High-Quality Dividends On Weakness

While I still maintain a relatively small trading portfolio, more than 90% of my net worth is invested in long-term investments.

When dealing with trades, I usually cut my losses early using stop losses. I have a different approach when it comes to my long-term investments.

Whenever I find an investment I like, I use stock price declines to expand my position. I cannot stand chasing a chart during an uptrend, which means I usually buy new investments rather aggressively whenever the economy is weakening.

Since last year, this applied to a number of stocks, including Extra Space Storage.

While it’s not the best thing ever that my EXR position is down 9%, it’s a high-conviction investment of mine that I love buying at a juicy yield. After all, the company is a great value/growth hybrid with strong long-term growth potential.

Buying a long-term compounder with a high yield is the best thing I can do in the current economic environment.

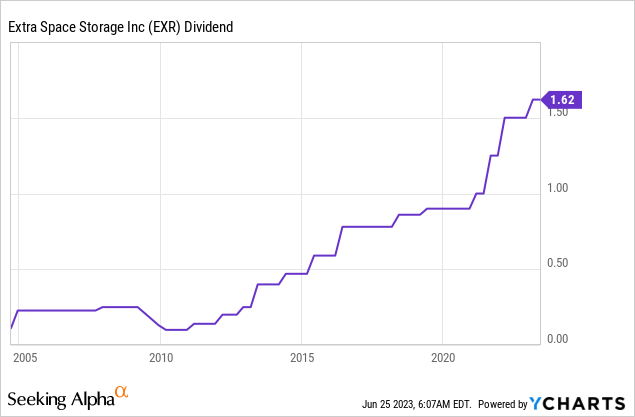

With that said, EXR currently yields 4.6%. The company has an AFFO (adjusted funds from operations) payout ratio of 74%, which is in line with the sector median.

Furthermore, over the past ten years, the dividend has been hiked by 19.0% per year – on average. That number has declined to 14.3% per year over the past five years. The three-year average is 20.0%, as the pandemic caused a steep surge in rents.

Data by YCharts

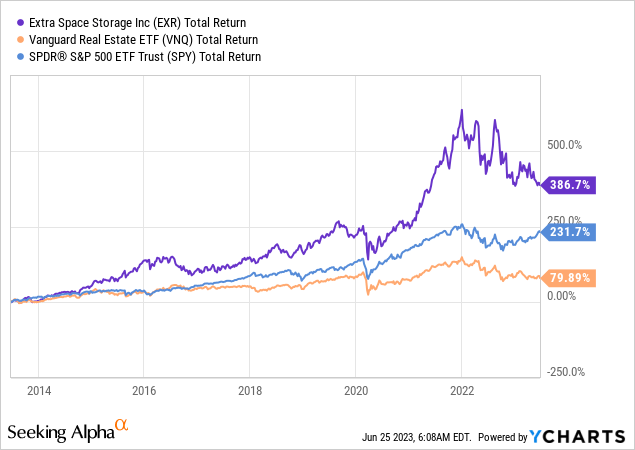

Thanks to strong dividend growth and a business model that made sustainable dividend growth possible, the stock has been an excellent wealth compounder in the past.

Since June 2013, EXR shares have returned almost 390%. Despite the recent sell-off and underperformance, EXR has outperformed the S&P 500 by a wide margin. The Vanguard Real Estate ETF (VNQ) returned just 80%. This ETF currently yields 4.3%, which gives EXR another advantage over the average REIT.

Data by YCharts

With that in mind, it makes sense that real estate is weakening. After all, higher rates are an issue in a sector that depends on affordable leverage to take on bigger projects and service existing debt.

The moment rates rise, operating cash flow is pressured – this applies to most companies. Not just real estate operators.

Hence, it’s important to mention that EXR remains in a great spot.

Despite Headwinds: Why I Remain So Optimistic

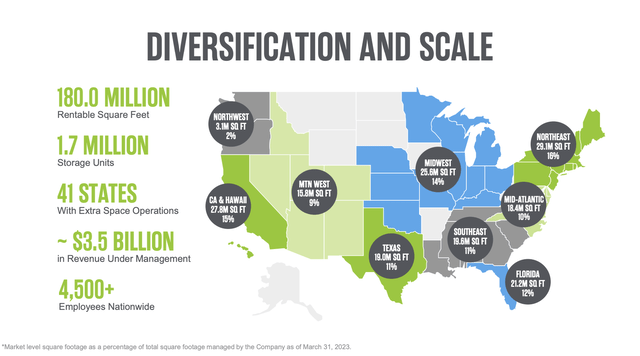

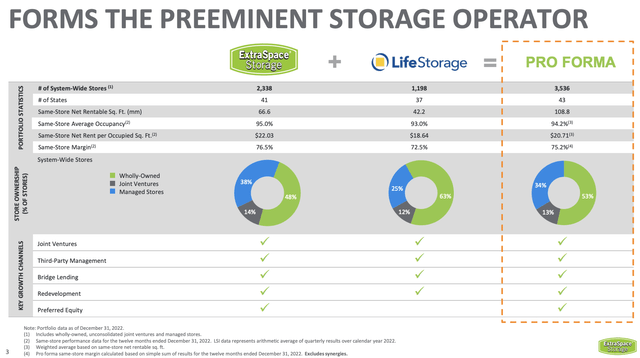

Excluding the pending acquisition of Life Storage (LSI), Extra Space is the second-largest self-storage operator with an 8.8% market share.

The company operates in 41 states. It manages 180 million square feet of rentable self-storage space, which covers 1.7 million units.

Furthermore, the company has a well-diversified portfolio of assets with major exposure in California, the Northeast, and the South.

Extra Space Storage

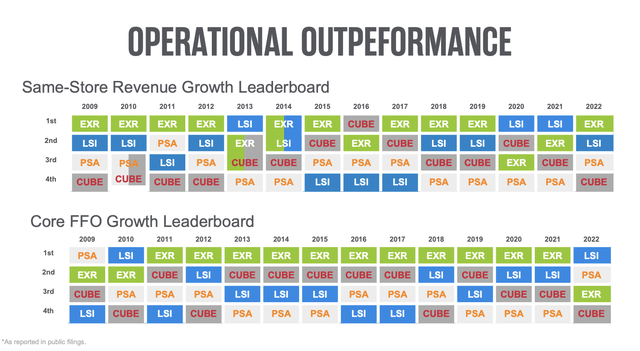

In its business, the company has been among the best performers since the Great Financial Crisis. Since 2009, the company has been the core FFO growth leader for 11 years.

Extra Space Storage

Another top performer, Life Storage, will soon be added to EXR, as the company is to be acquired in an all-stock deal, creating a combined company with an enterprise value close to $50 billion – making it the largest self-storage operator.

Extra Space Storage

Regarding this acquisition, this is what I wrote in my last article on Extra Space Storage:

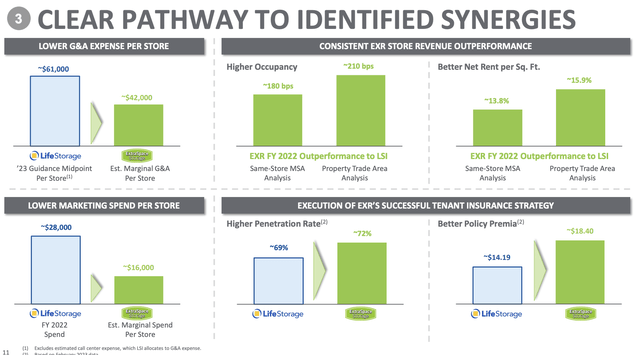

Furthermore, the fact that LSI is less profitable than EXR opens up new opportunities. It’s one of the reasons why EXR bought LSI. It knew it could quickly generate synergies.

EXR aims to generate at least $100 million of run-rate annual operating synergies, which includes improving operating expenses and boosting operating revenue.

As the overview below shows, EXR is a superior self-storage operator. If it applies its system to LSI assets, it should be able to generate synergies on a consistent basis.

Extra Space Storage

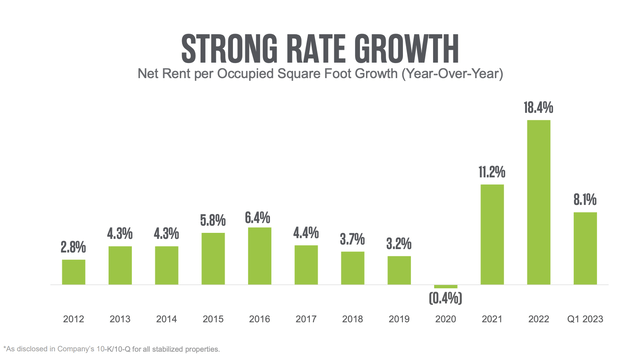

With that said, the industry remains in great shape – despite headwinds. According to the Yardi Matrix self-storage report for the month of May, the self-storage market continues to demonstrate resilience, even in the face of a slowing housing market.

Although there have been headwinds affecting demand, overall street rates remained stable in May, with a slight increase observed for 10×10 units.

While year-over-year street rate growth has turned negative, net operating income is still on the rise as operators raise rates for existing customers.

However, this has resulted in a slight decrease in occupancy rates.

Despite these concerns, storage demand remains above pre-pandemic levels, and the outlook for the sector remains optimistic.

In May, the national average rate for 10×10 NON-CC units was $128, exceeding the average over the previous 36 months by 1.8%. The national rate for 10×10 CC units was $143, which is 0.5% higher than the three-year average.

Furthermore, this low-moat industry is getting support from subdued supply growth.

The national new-supply pipeline experienced a ten basis point growth in May, with properties under construction representing 3.6% of completed inventory. While development activity remains consistent, rising development costs, particularly the escalating cost of debt, are expected to limit new supply in the coming years.

These developments are confirmed by Extra Space Storage.

In its first quarter, the company demonstrated strong operational performance, with occupancy reaching 93.5%, the highest first-quarter result outside of the COVID years.

Extra Space Storage

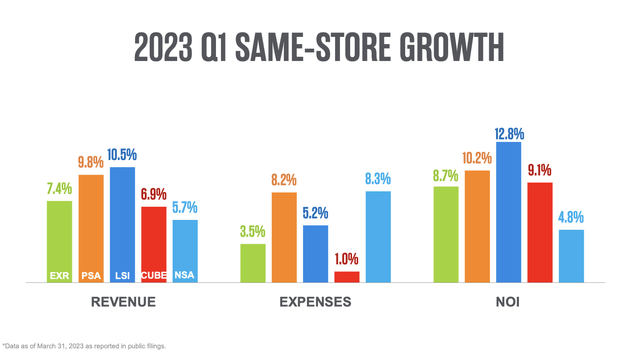

Sequentially increasing rates for new and existing customers contributed to a 7.4% growth in same-store revenue.

Same-store expenses were lower than expected due to normalized payroll expenses and year-over-year savings from repairs, maintenance, and property taxes.

The same-store NOI growth rate moderated from the fourth quarter but remained ahead of internal projections at 8.7%.

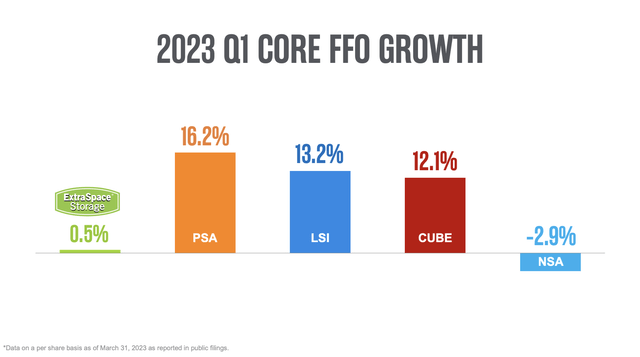

Extra Space Storage exceeded its internal projections for FFO in the first quarter, driven by better-than-expected property net operating income (NOI), lower general and administrative expenses (G&A), and increased management fees and tenant insurance.

Extra Space Storage

The company also experienced significant external growth, including the net addition of 44 stores to its third-party management platform, the acquisition of six stores in joint venture structures, and the approval of three remote model acquisitions as part of the company’s remote storage strategy.

Extra Space Storage

Furthermore, with regard to rent increases, the company has seen no significant pushback from existing customers. The number of move-outs from customers who received Early Communication of Rate Increases (ECRIs) peaked at around 800 basis points higher than those who didn’t receive ECRIs but has since stabilized at a slightly higher but manageable rate.

The company maintained a low bad debt rate (meaning tenants who do not pay) of under 2% and observed a willingness among customers to meet the demand for storage in the first quarter.

Balance Sheet & Outlook

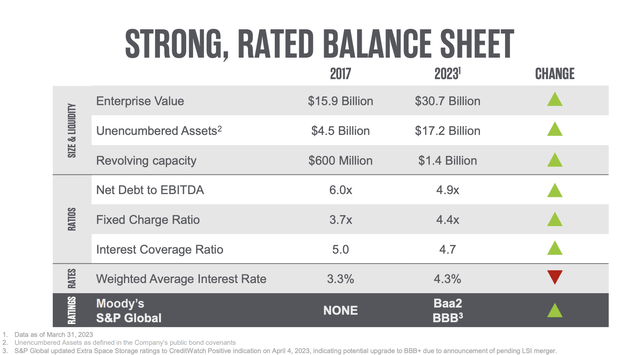

In the first quarter, EXR completed a $500 million bond offering, reducing its revolving balances and leaving over $1 billion in revolving capacity, which is great news for its liquidity.

Floating interest rate exposure was decreased to 22% of total debt, net of variable rate receivables.

Furthermore, S&P Global updated the company’s rating to CreditWatch positive following the announcement of the proposed merger with Life Storage, confirming its view that the transaction is credit-enhancing.

Extra Space Storage

This means that EXR could soon have a BBB+ credit rating, which is one step below the A-range, which I expect the company to enter within the next five years.

Adding to that, the company has a 4.3% weighted average interest rate, a healthy 4.7x coverage ratio, and a sub-5x net leverage ratio.

In light of strong 1Q23 results, the company reaffirmed its guidance ranges for same-store growth expectations and core FFO, excluding the impact of the proposed merger with Life Storage.

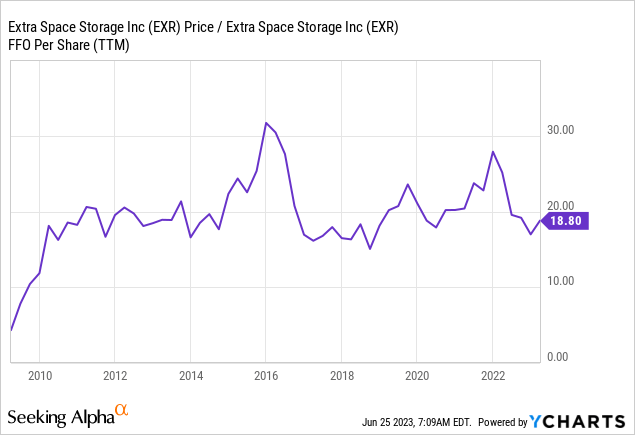

The company sees at least 3% growth in NOI and full-year core FFO between $8.30 and $8.60. Using the midpoint of that guidance, we’re dealing with a 16.8x valuation multiple. The median sector valuation is 12.2x FFO. In my opinion, this premium is justified, as EXR has more growth potential than its average peer.

This valuation is also slightly below its longer-term median, which is roughly 20x FFO.

Data by YCharts

While I cannot make the case that EXR has no room to fall further, I like the risk/reward a lot and will keep buying in the weeks and months ahead.

The biggest risk to EXR is if the Fed keeps rates higher for longer, which is not unlikely. However, EXR has a strong balance sheet and should be able to absorb big economic shocks.

Furthermore, because of its high (and well-covered) dividend yield, I believe that the risk/reward is highly attractive. Once economic headwinds turn into tailwinds, the company is in a fantastic spot to maintain high dividend growth, which would have a major impact on its current dividend yield. It would quickly result in a very high yield on cost for investors.

Pros & Cons

Pros:

Attractive dividend yield of nearly 5%.

Outperformed the S&P 500 and most real estate peers.

Resilient self-storage industry with an optimistic outlook.

Acquisition of Life Storage for potential synergies and growth.

Strong operational performance and consistent growth.

Cons:

Sensitivity to rising interest rates.

The potential impact of economic headwinds.

Takeaway

Despite the recent underperformance of Extra Space Storage and the challenges faced by the real estate sector, I remain optimistic about the company’s long-term prospects.

With its strong operational performance, well-diversified portfolio, and pending acquisition of Life Storage, EXR is positioned to be the largest self-storage operator in the market.

The self-storage industry has shown resilience and continued demand, supported by stable street rates and rising net operating income.

EXR’s history of strong dividend growth and its ability to generate synergies from the acquisition further enhance its value.

While there are risks associated with interest rate fluctuations, EXR’s solid balance sheet and attractive risk/reward profile make it an enticing investment.

Once economic headwinds subside, EXR’s high dividend growth potential could lead to significant yield on cost for investors.