Investment Thesis

As highlighted in my previous article, Urban Outfitters (NASDAQ:URBN) stock remains a preferred pick as strong operational performance catapults them into top tier growth trajectory. It has performed exceptionally well, up ~20% in a month driven by exceptional results and continued momentum. Its strong brand resonance among its customers, exposure to high income consumers, prudent inventory management and continued improvement in Urban Outfitters have helped them to propel growth and boost earnings in an otherwise dismal environment around the retail segment. We reiterate Buy and increase our target price to xx.

No Signs of Slowdown

URBN reported an exceptionally strong quarter with comp sales growth of 5% YoY significantly higher than the consensus of 2.5% driven by continued strength in Free People (up 17%) and Anthro (up 13%). It was a rare bright spot in an otherwise dismal environment where the other retailers echoed its pains due to slowdown in consumer spends and trade down effects due to inflationary pressures.

We currently see no signs of change in customer behavior. No indication that customers are shopping less frequently, buying fewer items or trading down.

– Richard Hayne, CEO, Urban Outfitters

Sales grew 6% YoY (including -1% FX effect) on the back of digital sales growing HSD while store sales grew LSD. Apparel and accessories continue to outperform at Anthro, which along with new customer acquisition (up 11%) led to an outsized comp growth. Free People Group also reported a strong quarter due to robust consumer response to its summer and spring trends driven by increasing customer base and higher average unit growth fueled by increased full price selling across categories. Urban Outfitters continue to report a negative comp, down 13%, as a result of outsized impact of the macro environment in the US and UK, while the rest of the Europe fared well reporting positive comp. We believe UO will continue to remain under pressure, however, its sequential improvement in the US as well as its ability to defend margins would bode well for the brand going forward. Nuuly’s net sales grew 118% YoY on the back of continued growth in subscriber base at 167,000, up from ~76,000 last year, and remains on course to reach or even exceed their target of 200,000 subscribers by the end of the year.

Earnings Beat and We Raise

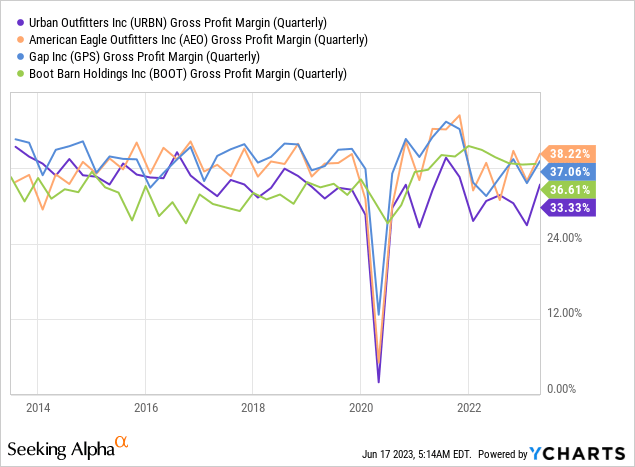

URBN reported a solid improvement in gross margins which improved 260 bps YoY driven by higher IMU at all three brands from lower freight and lower markdown at Anthro and FP. It guided 2Q Gross margins to be higher by 300 bps as a result of lower inbound freight costs and lower markdowns and is on course to reach ~300 bps improvement in IMU by the end of this year. Despite a significant bump in margins, there is still a significant margin upside potential compared to its top-tier peers and its own historical average.

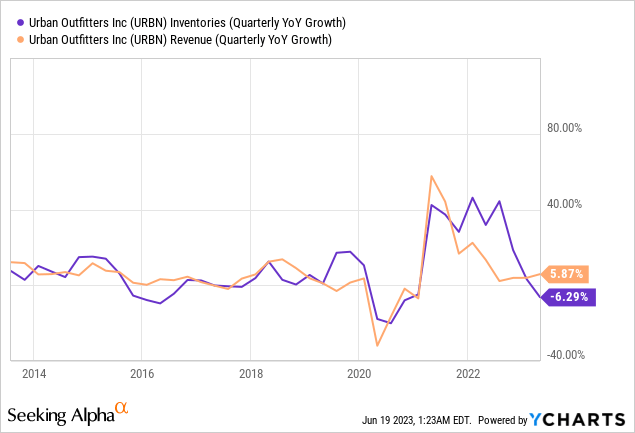

We believe given the execution of the brand around bringing fashion products more closer to customer requirements, category success across the board at all three brands and better product mix creating higher AURs and lower markdowns would provide a boost to its gross margins. As also demonstrated, its inventory to sales spread has continued to improve as URBN has a tighter control on inventory and faster supply chain yielding higher inventory turns.

While SG&A $ growth is expected to increase in double digits driven by higher payroll due to higher incentives as well as marketing spend, it is expected to deleverage as a result of growing sales. It expects to maintain the comp growth in Q2, in line with Q1 with implied EPS of $0.8-0.9 (assuming a 200 bps Gross margin improvement and lower double digit SG&A growth). We raise our EPS estimates for the year to $2.80 driven by stronger beat in Q1 and continued momentum in Q2 and H2.

Balance sheet remains strong with liquidity of $820 mn (cash of ~$470 mn and undrawn credit facilities of $350 mn) with no debt.

Valuation

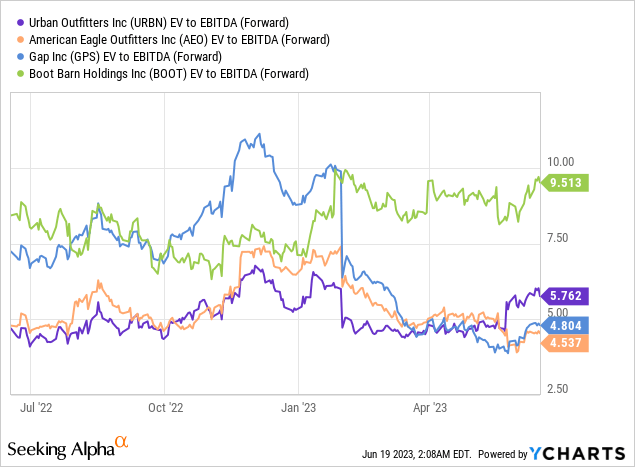

At the time of initiation, we had assigned a target price of $32 (at 5x EV/ EBITDA). We continue to believe that URBN still trades cheaply at 5.8x Fwd EV/ EBITDA given its strong performance and upside potential to gross margins driven by higher inventory turns. We reiterate Buy and raise our target price to $38 (at 7x EV/ EBITDA) on the back if improved performance metrics.

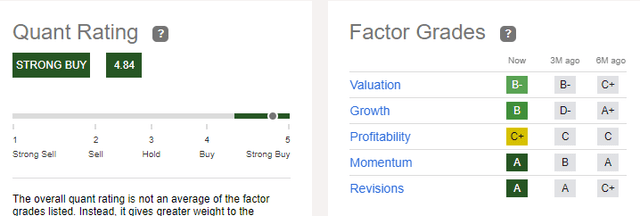

Quant ratings continue to rate this as strong buy on the back of earnings momentum and valuation comfort.

Seeking Alpha

Final Thoughts

URBN has reported record results in an otherwise dismal retail environment and its management citing no change in consumer spend remains a stark contrast to the pain shared by other retailers. We believe the brand resonance and its ability to drive faster inventory turns and bringing fashion products that consumers want have fared well leading to higher sales and lower markdowns boosting margins. We continue to believe its strong execution would continue to fare well and as demonstrated during the 2008 Global Financial Crisis, it has been able to outperform the market by a mile. Reiterate Buy, raising target price to $38.

Read the full article here