If it looks like an office. If it’s occupied like an office. Is it an office? Activist Investor and founder of Land and Buildings, Jonathan Litt, apparently thinks so.

In a recent segment on CNBC’s Fast Money, Litt elaborated on his short position in Alexandria Real Estate (NYSE:ARE), which is a life-science-focused REIT that is a trusted landlord to some of the largest pharmaceutical companies, including Bristol-Myers Squibb Company (BMY), Moderna (MRNA), and Eli Lilly (LLY).

The main premise of his short position is that ARE is no different than any other office operator and should be valued as such. To support this, he pointed to in-house research that analyzed cell phone data of those entering and leaving ARE’s properties.

The dataset showed that physical occupancy across the portfolio is down 50%. This is telling and notable because it cuts against one of the main selling points about ARE’s portfolio. Being that their space is primarily medical labs, one would reasonably expect that the portfolio would be insulated from the secular risks of remote/hybrid working arrangements. Litt’s data seems to say otherwise.

Building on the data, Litt warned about their lease expiration schedule and the threat of new incoming supply. And given current trading values, he views the stock as at least 40% overvalued to their office-based peers. While his argument has merit, I don’t view it as a profitable one.

Jonathan Litt’s Concerns On ARE’s Physical Occupancy Levels

Physical traffic levels aside, ARE’s current occupancy rates are running north of 90%. Others are struggling to even reach the 90% mark. Boston Properties (BXP), for example, ended Q1 with total in-service occupancy of 88.6%. SL Green’s (SLG) rates were in the same ballpark. ARE’s stronger portfolio already warrants a premium to peers.

The physical cell data also requires extra attention.

CNBC Fast Money – Snippet Of CNBC’s Interview With Jonathan Litt

By nature, there’s more movement in a lab than there is in a typical office. For example, in an accounting firm, someone can sit at the same desk all day long. In a lab, on the other hand, scientists may shuttle from one location to another. How does the cell data account for this movement?

Another point worth consideration is the sensitivity around lab work. In research environments, cell phones are often prohibited from entry due to either the proprietary nature of the work or simply because of the damage it may cause to the underlying experiment. What if cell phones aren’t on hand when the space is occupied?

Litt’s data is capturing the amount of time being sent in the labs. More specifically, those that are spending at least an hour, which is important because it filters out those that may be simply visiting or delivering goods, a nuisance that is often improperly reflected in other datasets. In my view, I sense that more administrative functions are being performed remotely, while the lab aspects are being performed on site. If that’s the case, there’s nothing wrong with that because there remains an underlying demand for the lab itself.

Litt stated that those that are spending time in the buildings aren’t staying for a full workday. Instead, they are present for an average of just under six hours. I’d say, “so what?” to that. It doesn’t change the fact that lab experiments simply cannot be performed at home.

The lab aspect and the nature of the sensitive work performed in it is a key consideration, which I believe is being overlooked by Litt.

Jonathan Litt’s Concerns On ARE’s Asking Rents

Litt built upon the lower physical attendance levels by stating that ARE’s asking rents are about $50/psf, which is below the $100/psf that a lab should command. This further reinforced his position that ARE’s portfolio is more typical of an office than a lab. In addition, Litt mentioned that ARE would be at heightened risk upon lease expiration. This makes sense upon first thought. After all, why would a company want to pay 100% asking price on space if it’s only being 50% utilized?

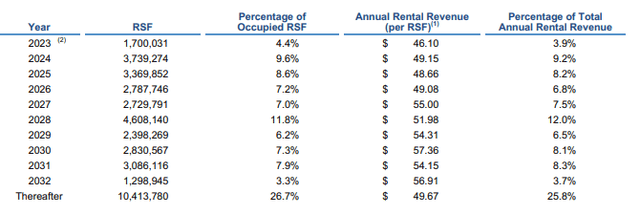

Q1FY23 Investor Supplement – Lease Expiration Schedule

But what he didn’t mention was the rental spreads ARE is commanding upon renewals. In Q1, the company realized cash spreads of 25%. A traditional office would be lucky to command that level of pricing power in today’s environment. ARE’s leasing performance also contradicted his concern regarding the leasing expirations. In Q1, the company leased 1.2 MSF of space. This was the 12th consecutive quarter with leasing volume above 1 MSF. It was also above their five year pre-2021 average.

If their space was truly at secular risk, why would companies be rushing in to sign space at rents 25% above current prices?

Jonathan Litt’s Concerns On ARE’s Construction Activity

Another point made pertained to new construction activity. Given the development pipeline and the threat of new incoming supply, the current thinking is that there will be excess space in relation to demand. This will take time to play out in real time. But I don’t see the doom coming to fruition. ARE reduced guidance for construction spend in 2023 by +$250M in recognition of the uncertain environment.

The reduction was triggered by a pause in some of their projects under construction. And aside from their actions, management also noted a general pullback in the overall sector pipeline due to delays and cost escalations. Incoming supply, therefore, is expected to be less than what most expect.

The pipeline for new drug development, on the other hand, is expected to continue increasing in the years ahead. By 2027, for example, total spending is expected to near 2.0T. To accommodate that level of spending, there will need to be available lab space. If construction is unable to keep up, the supply dynamics could become very favorable to ARE.

Is Shorting ARE Stock A Good Idea?

When considering cell data, current rents, upcoming expirations, and the threat of new supply, Litt views ARE at least 40% overvalued compared to other office operators.

Supposing for a moment this holds water, investors should consider where ARE is currently trading at. At a current price of about $115/share, ARE is trading at about a 6.5% implied cap rate. Other office operators are trading at 10%+.

So Litt does have a point in saying that ARE trades at a 40% premium. But one should also consider that ARE is doing deals in the sub 5.5% range. That’s a testament to the quality of their overall portfolio. Is a 10% implied cap rate, then, realistic for ARE? I’d argue to the contrary.

Prospective investors can debate all day whether ARE is an office or not an office. But in the end, one should ask themselves this: What is a more at-risk property class? A traditional office tailored for more administrative functions? Or a lab which houses cutting edge research equipment used for the development of next generation medications? To lump ARE in with other pure-play office operators is equivalent to disregarding their primary business model.

Jonathan Litt made a bold trade on ARE. But he’s unlikely to post a market beating return on it.

Read the full article here