Suddenly, amid cooling inflation data and enthusiasm for AI, the mood in the markets seems buoyant again. Investors are willing to bet on risk, and some of last year’s tech laggards are finally starting to see healthy rebounds.

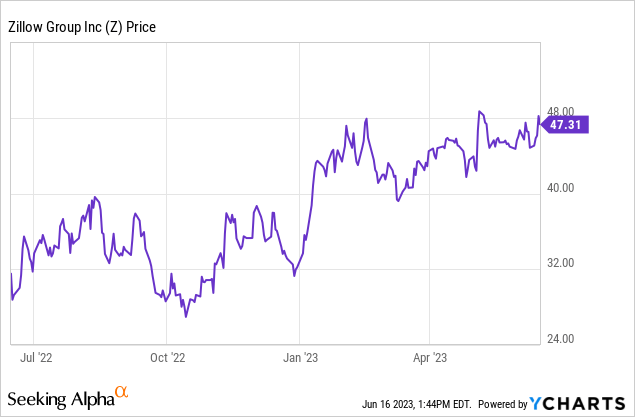

One area that may continue to see a protracted recovery period is real estate, as interest rates do remain high and supply remains tight, capping transaction volumes. Amid this reality, Zillow (NASDAQ:Z) continues to fine-tune its operations and retain its status as the world’s leading real estate site. Already up ~40% year to date, I think Zillow’s recent rally still has plenty of steam left.

I remain firmly bullish on Zillow and am holding onto the stock in my portfolio. In spite of current revenue declines driven by industry softness, I think Zillow’s return to focusing on its core Premier Agent business and lopping off its distracting Zillow Offers subsidiary will push investors to remember that Zillow is a high-margin internet business with a firm moat provided by its incredible brand equity as well as its unmatched data stores.

It’s also worth noting that in spite of double-digit declines in real estate transactions, Zillow reported that traffic to its website and apps was relatively flat year-over-year. The translation here, at least for me: consumers are still very much interested in real estate, and there may be pent-up demand for transactions once interest rates cool down or new housing supply hits the market to reduce pressure on prices.

Here, in my view, is the long-term bull case for Zillow (from previous coverage):

- Exit from iBuying shines the spotlight on margin-rich IMT segment. In 2022, Zillow generated a rich 27% adjusted EBITDA margin in its IMT segment. That indicates a revenue stream that is nearly pure profit and very minimal overhead, and directly correlated with the uptick in real estate activity. To me, removing the distraction from iBuying and its horrendous quarterly losses will have the effect of expanding valuation multiples for Zillow’s profitable core business. Note that this 27% margin already captured the start of a housing recession; in the boom year of 2021, adjusted EBITDA margins in this segment were far higher at 46%.

- Across Zillow, Trulia, StreetEasy, and HotPads, virtually every American consumer thinking about buying or renting a home will come across one of the Zillow Group’s websites. Zillow has built an ecosystem rich with real estate data that has become the forefront of online real estate for users. Zillow traffic reached a record high of 10.5 billion visits (+3% y/y) in 2022.

- Zillow is a platform that can add a whole suite of additional monetizable services. With all this traffic, Zillow’s ability to generate tertiary revenue is broad. Currently, the majority of Zillow’s business comes from advertising fees paid by real estate agents, but the company is also expanding into distributing mortgage products as well. In the future, Zillow could offer a full suite of “after-market” home add-ons, including house insurance, moving services, furnishing/interior decoration services, and others.

- Capital-light internet business. Unlike other digital-age real estate competitors like Redfin (RDFN), Zillow runs its apps only – it doesn’t have to worry about compensating real estate agents or affiliates of its own.

- Substantial cash war chest. Zillow is well-capitalized to power through even an extended recession. On its most recent balance sheet, the company held $3.37 billion of cash (for relative sizing, that’s nearly two years’ worth of revenue for the company) against $1.66 billion of debt.

For a company whose revenue is now purely high-margin ad-based, Zillow’s valuation is also quite modest, in spite of this year’s rally so far. At current share prices near $47, Zillow trades at a market cap of $11.01 billion. After we net off the $3.37 billion of cash and $1.66 billion of debt on Zillow’s balance sheet, the company’s resulting enterprise value is $9.30 billion.

Meanwhile, for next fiscal year FY24, Wall Street analysts are expecting Zillow to generate $2.16 billion in revenue, representing 13% y/y growth. This puts Zillow’s valuation at 4.3x EV/FY24 revenue.

For a company that has continued to generate positive adjusted EBITDA even in this year’s tough macro climate, and with potential pent-up demand for housing driving a rebound, I’d say Zillow still remains at a great entry point. Stay long here and continue to ride the upward rebound.

Q1 download

Let’s now go through Zillow’s latest quarterly results in greater detail. The Q1 earnings highlights are shown below:

Zillow Q1 highlights (Zillow Q1 earnings release)

Zillow’s total revenue declined -13% y/y to $469 million. Though this sounds relatively dire, there are a number of points that make this outcome much brighter than at face value.

First: Zillow beat its internal expectations of $404-$437 million (-25% y/y to -19% y/y) by a wide mile; versus even the high end of its original Q4 expectations, the company came in 7% stronger. Consensus, too, had only expected Zillow to generate $426 million in revenue (-20% y/y).

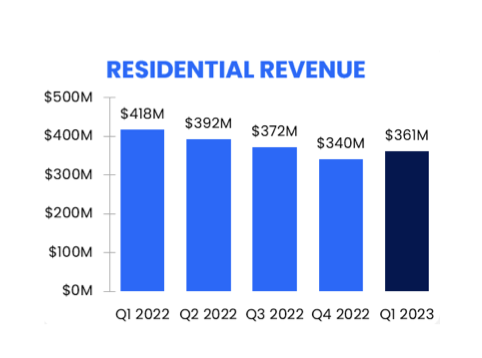

Second: Zillow’s residential segment, which is the biggest driver of revenue and includes the Premier Agent business, saw revenue rebound sequentially by 6% even in spite of macro headwinds. On a year-over-year basis, the Premier Agent business also accelerated from -20% y/y in Q4 to -16% y/y in Q1.

Zillow residential revenue trends (Zillow Q1 earnings release)

Note as well that Zillow is trending well above market declines. Per Zillow, the housing industry saw a -27% y/y reduction in transaction dollars in the first quarter – which means the Premier Agent business is trending ten points better than the underlying market. The company notes that funnel marketing investments that it made in mid-2022 are starting to pay off and yield higher conversion rates, despite the reality of low housing inventory and high interest rates.

Here is further commentary from CEO Rich Barton’s remarks on the Q1 earnings call, including his expectation that Zillow will continue to track ahead of real estate market trends in Q2:

Since the beginning of 2022, we have made significant investments in improving our customer funnel, capturing more customer demand and connecting more of that demand to our strengthening partner network, resulting in increased conversion rates in Premier Agent. We have focused on many improvements in our customer funnel experience by offering clear call to action that quickly and efficiently help solve customer needs. These numerous incremental changes collectively have been adding up to make a real impact on our business. The most tangible example we made over the last year is providing easier ways for buyers to request home tours on Zillow apps and sites. This has resulted in less drop-off in our funnel, which is a key driver behind improved expected lead volumes of higher intent customers, which does not yet even account for the benefits I’ll discuss shortly from real-time touring. Overall, it has been nice to see our focus and investments begin to pay off, with our year-over-year residential revenue outpacing the broader real estate market by 1,300 basis points and an expectation that we will see continued relative gains in Q2.”

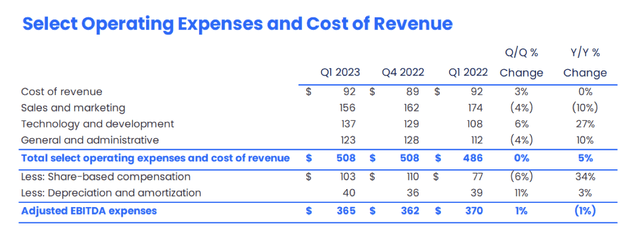

And amid weaker top-line trends, Zillow has also done a good job at balancing costs as well. The company sliced sales and marketing costs down by -10% y/y, which offsets a 27% y/y jump in technology and development costs.

Zillow Q1 opex (Zillow Q1 earnings release)

As shown in the chart above, total adjusted EBITDA-based expenses declined -1% y/y. The company generated $104 million of adjusted EBITDA in Q1 at a 22% margin, versus a 31% margin in the year-ago Q1.

Key takeaways

With healthy profitability, top-line trends that are tracking above market declines, stable traffic, and one of the most recognizable brands in real estate, Zillow remains a top-notch investment choice. Stick with this stock as it prepares for a real estate rebound.

Read the full article here