Genius Sports (NYSE:GENI) is a leading global provider of digital technology, data, and media solutions to the sports, sports betting, and sports media industry.

The company went public through a SPAC in 2021, and shares performance has been underwhelming since then. The share price reached ~$25 per share at one point and saw a steep decline in 2021 before gradually declining and reaching +$6 per share at present.

Despite that, I believe that the business fundamentals have been relatively solid. GENI has a good balance sheet, double-digit growth, and a moderately strong moat. Based on the latest progress in Q1, it remains on track to see a further increase in adjusted EBITDA as it is also well-positioned to benefit from some catalysts driving growth and profitability.

In this coverage, I would rate GENI a buy. My modeled target price indicates that the stock is significantly undervalued at its current price of approximately $6 per share.

Catalyst

I think that GENI’s fundamentals have remained relatively solid up to date, and should even improve due to several catalysts, primarily the legalization of sports betting in the US market as well as new technology implementation on the platform driving win rates.

GENI’s quarterly report

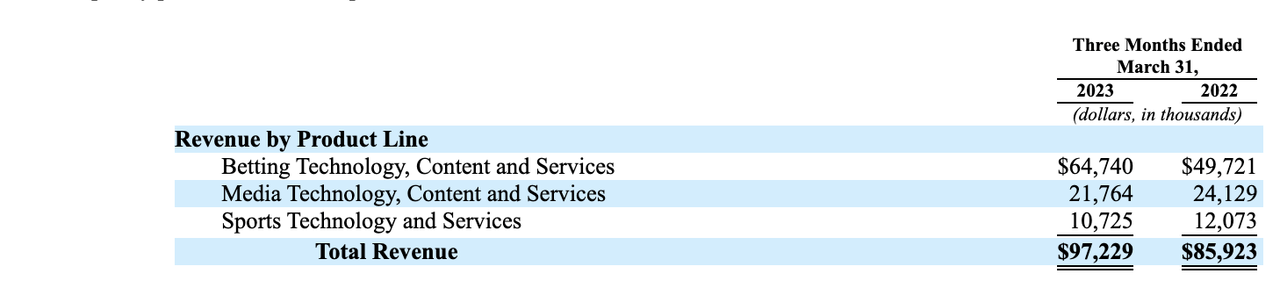

The majority of GENI’s ~$97 million revenue comes from its betting technology, content, and services / BTCS business. The outlook here remains solid, with GENI reporting a ~30% YoY growth in Q1. I believe that BTCS is fundamentally a robust revenue stream with good visibility because it comes from long-term contracts with sports federations/leagues and bookmakers that entail fixed guaranteed minimum payment based on the number of sports events.

In addition to that, GENI also derives revenue from GGR / gross gaming revenue as part of its revenue share agreement with sports bookmakers. Based on its 20-F, half of GENI’s FY 2022 revenue was derived from the fixed minimum payment scheme. Because of the mission-criticality of the solution, I also found it unlikely for churns to occur on either the sports federations or bookmakers’ side.

GENI’s presentation

Moreover, I believe that the increasing legalization of sports betting, primarily in the US, will continue driving growth in GGR, and subsequently GENI’s BTCS and overall revenue growth in Q2 and beyond. This was driven by new state launches, as we have seen in Ohio and Massachusetts in Q1, which I expect to continue in Q2 and beyond across more states. As a result, the company estimates that the US sports betting market will become an $18 billion market in 2027, a significant increase from $7 billion in 2022.

Because of the BTCS’ strong performance, GENI still reported a relatively solid 13% YoY growth in Q1 despite the media and sports technology services / MTCS and STS experiencing a ~9.5% and ~11% decline respectively.

GENI’s presentation

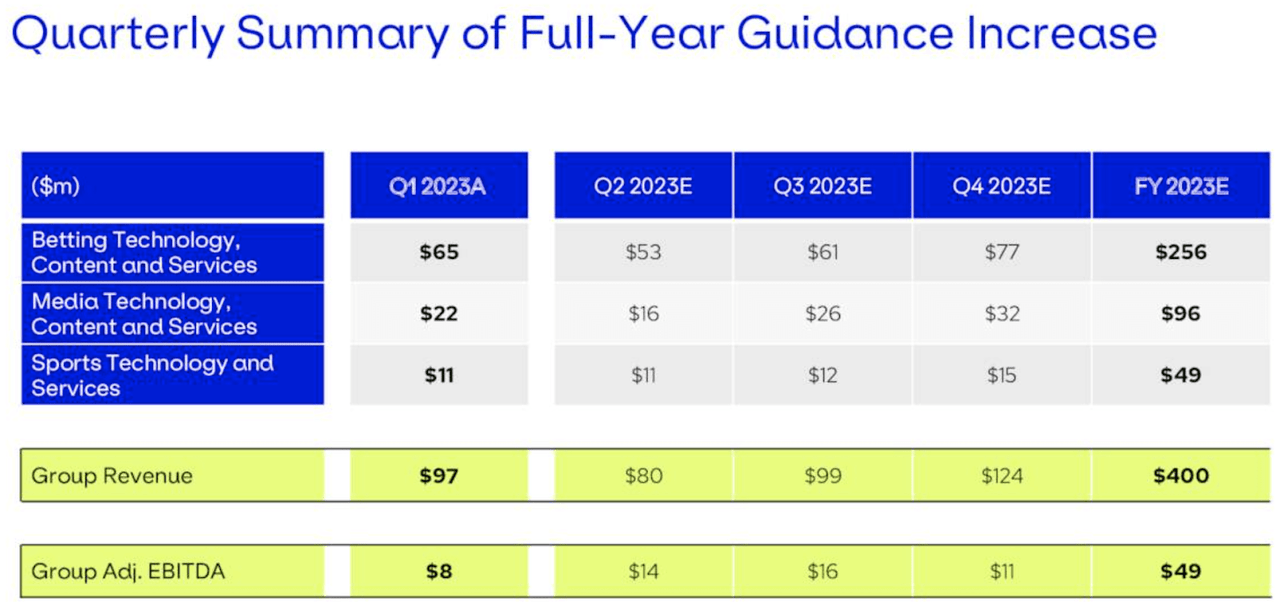

The decline in MTCS business reflects the overall industry-wide challenge in the marketing and advertising sector due to the ongoing macroeconomic slowdown. Looking at the company’s FY 2023 guidance, which expects ~17% growth in MTCS despite the decline in Q1, I feel that there seems to be a bit of optimism that the slowdown should subside in the next 12 months. I think that the projection here is probably slightly aggressive.

Meanwhile, I expect that the volatility in STS revenue growth will be relatively normal. As per its 20-F, GENI sometimes does not generate cash-based revenue from providing its STS solutions to its clients. Instead, it sometimes receives streaming rights and official sports data, typically from non-tier 1 federations, as an exchange. As a result, STS appears to be a part-strategic, part-financial revenue stream for GENI.

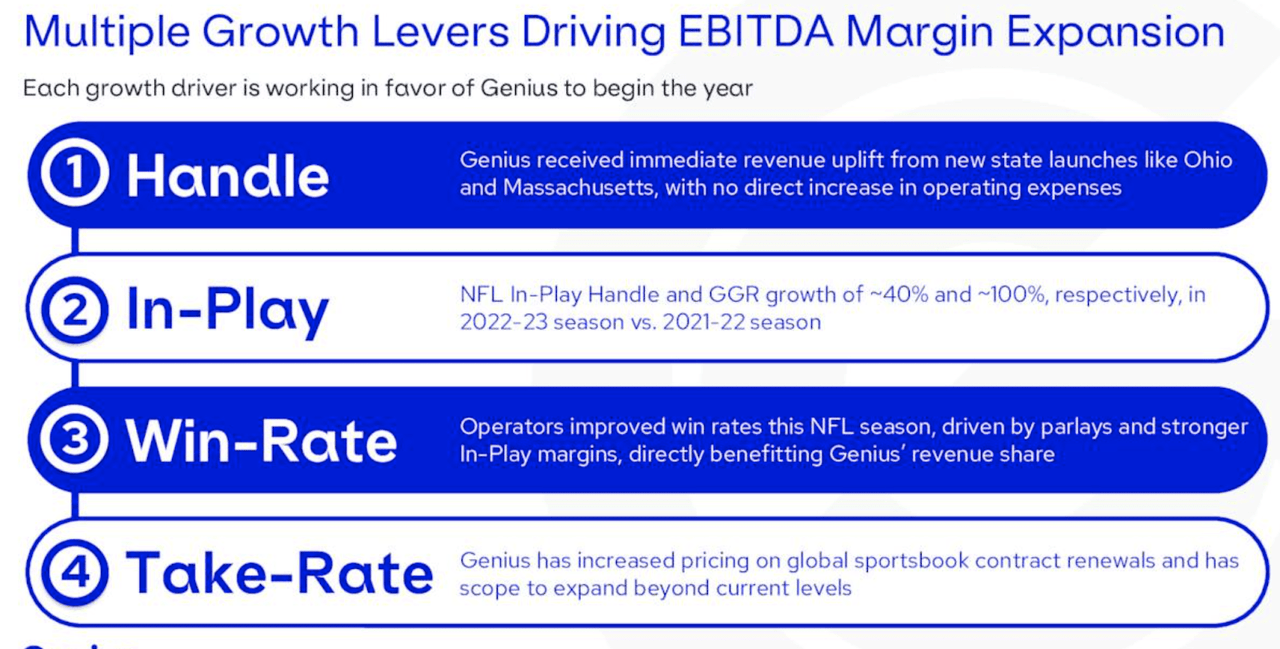

Furthermore, the same new state launch catalysts will benefit GENI’s profitability quite significantly. As suggested by the management, the launch of betting services in more states by its existing sports bookmaker partners presents a revenue growth opportunity at a relatively low marginal cost, expanding the adjusted EBITDA margin.

GENI’s projection of ~$49 million adjusted EBITDA for FY 2023 means that it expects the figure to double from FY 2022. This is probably not a far-reaching possibility – Benefitting from the catalyst, GENI already generated an ~$8 million of adjusted EBITDA in Q1, meaning that it is already halfway through its FY 2022’s figure in just a single quarter.

Risk

I would consider potential litigation matters related to data rights and competition from international players with a strong reputation in particular sports analytics to be key risks for the stock.

From 2020 to 2022, GENI was involved in a litigation case launched by its competitor Sportradar over data rights in the UK. While this was more of a one-time occurrence, what surprised me the most was the amount of settlement GENI spent to resolve the litigation. GENI spent over $24 million in FY 2022 to settle the case, which materially impacted its bottom line. Accounting for that expense, GENI would have realized a negative $9 million in adjusted EBITDA in FY 2022. I am not sure if a similar event may repeat in the future, though given the potential material impact, I would advise investors to remain cautious about GENI navigating the data rights-related issues.

Furthermore, competitive dynamics from well-equipped and competitors specialized in certain sports such as Opta / Statsperform may in the worst case affect GENI’s contract renewal activities with its clients. The good news is that in Q1, GENI reported no churn so far, and it seems that the new skeleton technology of its recent acquisition, Spectrum, continued to see adoption from one of its key clients, English Premier League / EPL, the most watched sports league in the world. In 2019, GENI inked a 5-year contract with EPL, meaning that the contract renewal discussion should have been happening as of today.

Valuation / Pricing

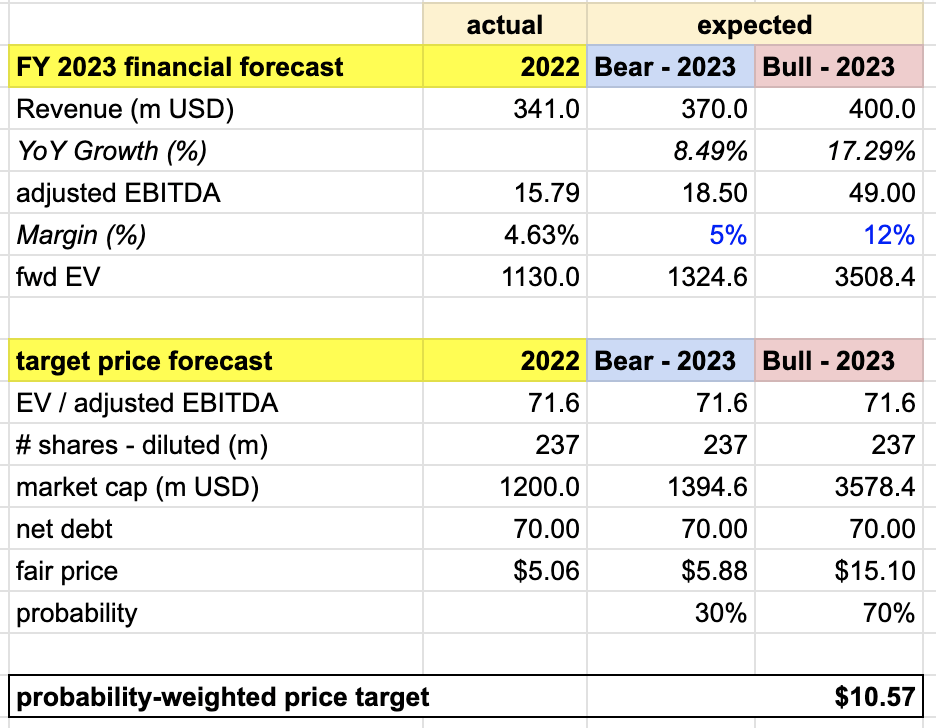

My target price for GENI is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 projection:

-

Bull scenario (70% probability) assumptions – GENI to achieve the high end of its FY 2023 guidance of $400 million of revenue, representing a +17% growth which is a reacceleration from last year, and $49 million of adjusted EBITDA.

-

Bear scenario (30% probability) assumptions – GENI to see $370 million of revenue, an +8% YoY growth, a lower growth outlook than last year. I expect EBITDA margin to stay at ~5%, a similar level to where it is now.

I assign GENI an EV/adjusted EBITDA of 71.6x across both scenarios. I think it is a fair figure, considering that it is based on the latest FY outlook in 2022, where adjusted EBITDA margin is at a similar level to that of the bear scenario. In addition, I expect GENI to see an adjusted EBITDA margin expansion under the bull scenario.

author’s own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of +$10 per share, suggesting a significant ~1.5x upside from the current level.

Conclusion

GENI exhibits solid fundamentals with a strong balance sheet, double-digit growth, and a moderately strong competitive advantage. Q1 progress suggests improvements in adjusted EBITDA and the company’s potential to benefit from growth catalysts. However, litigation risks and competition from established international players in sports analytics should be considered. On the positive side, the increasing legalization of sports betting, particularly in the US, is expected to drive revenue growth. Overall, I rate GENI as a buy, as its current stock price of ~$6 per share appears significantly undervalued based on my target price.

Read the full article here