Dear readers/followers,

To say that I massively added shares of Rolls-Royce (OTCPK:RYCEY) would be wrong and a lie. I added shares, establishing a small position when I last covered the company. That was back in October, after a 50% drop, though at the time it dropped, I did not hold a positive thesis on the company. That “BUY” rating did not come until October. As you know, I’m a long-term investor – and since that particular time, the company has jumped.

And by jumped, I mean jumped.

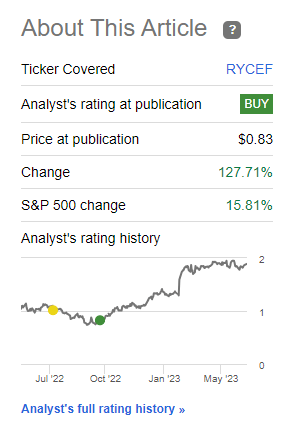

This is my RoR for my position since that time. That’s beating the S&P500 by more than 8x since that particular article.

Seeking Alpha Rolls-Royce (Seeking Alpha)

So, all in all, it’s fair to say that Rolls-Royce has been an absolutely amazing investment. One of my best investments on a TTM basis. The reason I haven’t highlighted it more, and used it as my poster case for why you should pay attention to my stances, is really that I didn’t buy much of the company at the time. I bought some – but not much.

A 127% RoR for a $10 position is only so much – and I’m not saying my position was $10, but it wasn’t a full percent or 3% of my portfolio. Rolls-Royce was, as I saw it, too risky for that.

It remains a tricky sort of turnaround case.

Let’s look at what Rolls-Royce can offer us going forward.

Rolls-Royce – Results and trends are good, let’s see what the company offers.

There’s one other image that I want to show you that at least somewhat confirms that I “know” somewhat of what I am talking about. Prior to shifting my stance on Rolls-Royce, I had a long-published and held stance of avoiding RYCEF. Take a look.

Seeking Alpha Rolls-Royce (Seeking Alpha)

The fact that I went positive was no fluke. It was that the company finally reached a long-held level of undervaluation that I pretty much since day one viewed as the turning point for the company and where it would become appealing.

I only wish I had the courage to really stake a solid claim in the tens of thousands, as this would have lifted my results even further. And it wasn’t that I was unclear in my last article, either – here’s specifically what I said.

That is, I’ve never switched my stance up until now.

Because now it’s time to go “BUY” on Rolls-Royce.

(Source: Rolls-Royce Article)

After this massive climb, and especially since the bounce, all sorts of Rolls-Royce-positive investors have come out of the woodwork. People that did not consider the company a “BUY” when they were cheap, suddenly now consider the company one of the best things since sliced bread. This is neither strange nor the first time this has happened.

If you’re a valuation-oriented investor with a contrarian streak, you have to get used to the discomfort of owning companies that 99% of the market tells you are not “good”. Provided you’ve done your research, things can work out okay, or as you can see here, much, much better than okay.

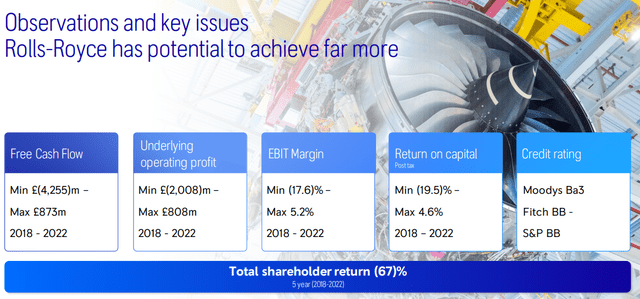

And it’s not that the current share price means that RYCEF has suddenly turned everything around. The company is still in a negative spiral with a 5-year TSR of negative 67%. Its FCF is slowly recovering, as is EBIT margin and ROCE/ROIC, but it’s going too far to say that there are massive signs of a new dawn for the company.

It’s also still BB-rated.

Rolls-Royce IR (Rolls-Royce IR)

Some investors that went positive now will argue that it couldn’t have been foreseen, these business successes resulted in the share price bounce. And they’re right – not those specifically. But unless you believed that RYCEF was essentially ready to be chopped up for parts and sold off, then some sort of upside was, as I saw it at the time, almost a given at some future point. That future point just happened to come now.

Positive changes have been visible for a long time for those who know where to look – like myself. If you read down deeply into the reports, you’ve been able to see that much of the company’s issues for some time have been external – like SCM.

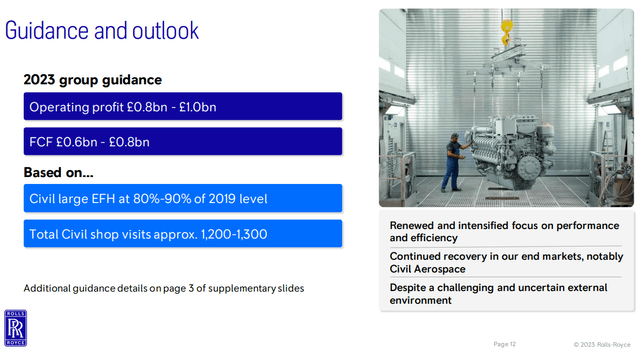

Financial performance has been in line with the full-year results and the company issued guidance for 2023 FCF at £600-£800M, as well as upwards of a billion pounds in operating profit. So Rolls-Royce is no longer “just” negative, it generates positive profit.

Rolls-Royce IR (Rolls-Royce IR)

Specific underlying positive trends came from Civil Aerospace with new wins, including the biggest-ever order of the Trent XWB-97, 68 engines plus 20 options ordered by Air India. The company’s interesting work in defense continues, with the AUKUS sub being powered by RYCEF nuclear reactors. Power systems are seeing aftermarket service demand, and extremely high order intake in 2022, especially for generation solutions, and the company’s new contracts are being awarded and signed at significantly higher margins than legacy, and this is starting to show.

The signs of a turnaround have been clear for some time, but they’re crystallizing now. Half-year 2023E results will come on the 3rd of August, so we’ll get more updates then – and I expect, barring unforeseen events, these to be positive.

The company has been working to bring leverage down, and has been succeeding in doing so, slowly chewing away at that leverage to get down to a level where they are considered “best in class”, and where the company could see a restoration to BBB-rating as a possibility. That lack of an investment-grade credit rating is really hurting the company’s interest costs and institutional investment appeal.

Rolls-Royce IR (Rolls-Royce IR)

Rolls-Royce, in a lot of ways and as odd as this may sound, is actually a very good company – the “perfect” company. What do I mean by this?

I mean that the company combines a very appealing legacy portfolio with plenty of attractive patents, a good aerospace customer base with customer-oriented defense contracts, then supplements this with attractive potential growth markets like SMR. If the company had been able to avoid the catastrophic downturn we’ve seen the past few years, I have no doubt this business could be a stalwart. And currently, I can see the business’ path returning to this sort of stalwart or positive level on a forward basis.

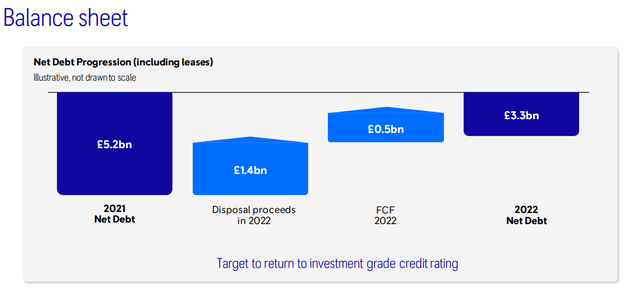

The net debt progression can be characterized as especially impressive, all things considered.

Rolls-Royce IR (Rolls-Royce IR)

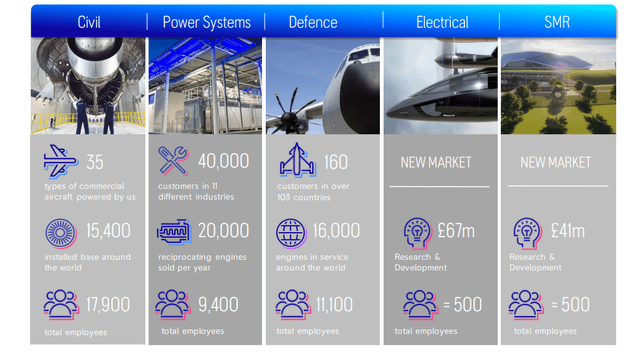

It’s easy to forget what Rolls-Royce actually does, and how much it has. It’s easy to forget all the sectors the company is active in, and how “good” many of its markets and customer bases are. It’s easy to forget that in the right conditions, this company is a business that could be valued 5-10x today’s level – easily in my opinion.

So that you don’t forget those qualities as we move forward here, let me remind you with a quick illustration – from Civil to SMR, the company is found in many attractive fields.

Rolls-Royce IR (Rolls-Royce IR)

Rolls-Royce Valuation – Complex in the face of 100%+ RoR

Whenever a company delivers a triple-digit RoR in less than 8 months, it begs the question of how much we can expect from them in the next 8 months or 12 months. My answer to this, despite positive expectations, is “not much”.

The latest results do not completely take away from over 8 years of what I would euphemistically call “some mismanagement”, with zero current dividend yield. Many analysts actually consider the company to be overvalued at the current valuation, which for the native LSE ticker isn’t even a full quid per share. It’s understandable, because the company has yet to “prove” much of its success, and many of its financial strength metrics are still down.

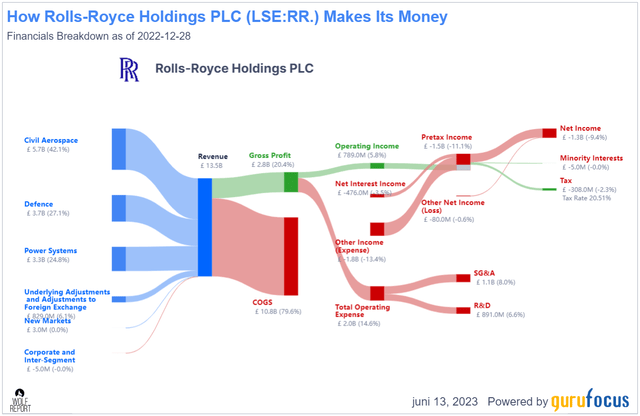

If you look at its revenue/net for 2022, that’s not a pretty picture – yet.

Rolls-Royce revenue/net (GuruFocus)

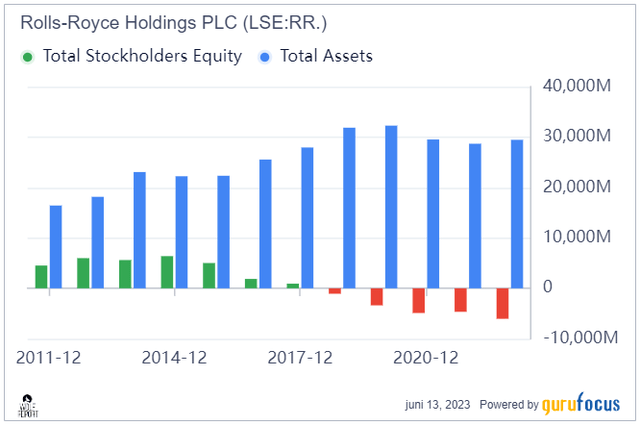

However, improvements are very clear. From pure fundamentals, it’s fair to say I believe that the company bottomed sometime in 2020. Since then, it’s been an upward trajectory, and I believe the company’s ROIC is indicative here of a significant fundamental turnaround sometime in the next few years. That turnaround isn’t there yet. SE is still deeply negative, and it will take time to turn around. Hopefully, we’ll see positive FCF this year, and I would be extremely surprised if that isn’t the case.

Rolls-Royce IR (Rolls-Royce IR)

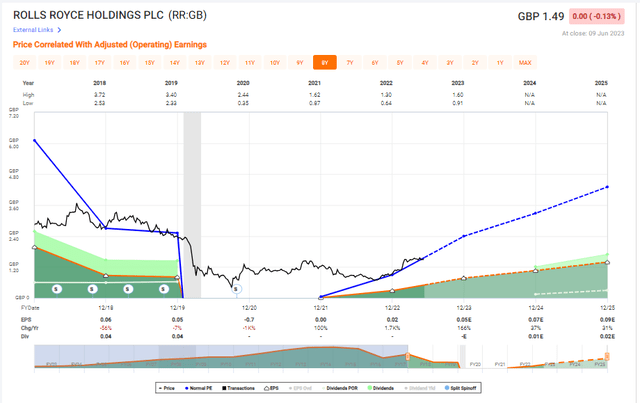

From a valuation perspective, Rolls-Royce, and by that I mean the native ticker, currently trades at a ridiculous P/E – but this is due to, you guessed it, missing earnings. For 2023E, the estimate is an EPS on an adjusted basis of $0.05/share, and growth from there, restoring the company dividend at a pence per share in 2024E.

Rolls-Royce Valuation (F.A.S.T graphs)

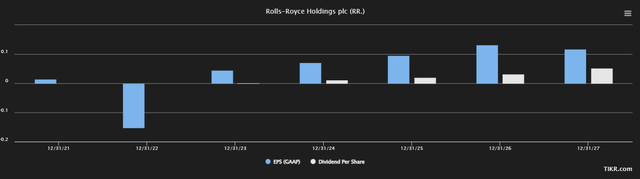

S&P Global analysts agree with this assessment, with GAAP turning positive this year, and a climb from here on, to a 2027E EPS of £0.12/share.

RR EPS/Dividend forecast (TIKR.com)

That’s what I base my positive Rolls-Royce thesis on. That eventual turnaround. That being said, I consider the company expensive for where it currently is. My last PT for the company was $0.85/share for the ADR. Even if I were to increase this to $1/share, which I think is fair given the recent results, I think more than that is unrealistic at this point.

Based on that, this is my thesis for the company as it currently stands.

Thesis

For now, this is my Rolls-Royce thesis.

- Great business, great exposures, great duopoly player with some really nice fundamentals – but with the pressures we’re seeing, and the Ukraine war, things aren’t looking better except for the defense sector.

- No yield and low visibility make this a no-go at all but pennies on the dollar. Specifically, I’d want to pay no more than 0.5X-0.6X to NAV with a normalized EBIT as a base, which comes to around $1/share for the ADR.

- Because of that, I’m moving to a “HOLD” at this time.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Thank you for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here