Trade Thesis

As rates go higher and it seems that the “everything” bubble is going to die down. Because of that, I’ve been looking for canaries in the coal mine. One of these areas is bearish positions on zombie companies that have no true underlying business value. MicroStrategy (NASDAQ:MSTR) came to mind as I believe at this point it is essentially a levered Bitcoin fund masking itself as a company. I don’t have anything against Bitcoin as I’m agnostic to it when doing analyses like this, but my view is that if investors want to own Bitcoin then they can just buy it themselves. I find that there’s no reason to buy it through a company and my opinion is that if the management of a company thinks it has a lot of extra cash, rather than buying something speculative like Bitcoin (which is not fit for the risk tolerance of many investors) it could just pay out a dividend to its shareholders, and if the shareholders wanted, they could purchase bitcoin themselves. On top of this, MicroStrategy has levered up on Bitcoin to the point where I’m worried that it might not be able to pay back its creditors. I’m also worried that this is turning into a cult-like speculation; what I mean when I say this is that it’s never appropriate to put all your eggs in one basket and even worse to leverage it as much as possible, regardless of how bullish one is. In my opinion, Bitcoin Maximalists as they are commonly known treat Bitcoin like a religion doing exactly what I mean when I say “cult-like speculation” where they treat it as if it is the best thing since sliced bread with no downsides; in my opinion, this is the sense that I’m getting from both Chairman Michael Saylor, who is very bullish on Bitcoin, and the shareholders of this company who I will often find very vocal on different stock forums talking about how they are using the stock as a proxy play on Bitcoin.

I think the best way to go about analyzing MicroStrategy is to do a pot odds analysis and then work out the potential risks of the analysis and bearish thesis from there.

Pot Odds Analysis

Simply put, A pot odds analysis looks at the max downside, the max upside, and the statistical probability of both playing out. A great long position for example would be one with little downside, a lot of upside, and a higher probability of upside than downside. This analysis, while it sounds easy it’s actually difficult as it is hard to actually find out the downside or upside that something has. On paper, stocks have unlimited upside and the lowest they can go is zero, but in reality of course the chance of a stock going to the moon or zero is low, so instead I like to use option payouts to get a better view. This is because options unlike stocks have an expiration and strike prices, so this allows us to find out the exact time in which something must play out and the exact price to which it must go.

The first thing I would look at would be the bankruptcy risk for the company. This is essentially how low Bitcoin would have to go for the company to not be able to pay off creditors.

To get this figure we’d have to first look at their capital stack to see how their debt is structured.

Reorg

Source

Above is a detailed look at the debt stack for MicroStrategy. First, there are convertible bonds due in 2025 and in 2027. $650mm due in 2025 and $1.050bn due in 2027. Then there’s $705mm of secured debt due in 2028. None of this debt is callable meaning that the creditors can’t ask for the debt to be repaid early if the price of bitcoin goes down.

MicroStrategy has about 138k of Bitcoin which at current prices is worth $3.588 billion. The amount of debt due in 2025 and 2027 is about half the value of Bitcoin. But, since the 2028 bonds are secured by 15k of Bitcoin holdings, which can’t be sold, that has to be subtracted out of the 138k of Bitcoin when calculating a breakeven price.

A key thing to keep in mind is that because there are two different maturities for the debt the price of Bitcoin would have to go down in 2025 and stay down till 2027 for MicroStrategy to not be able to pay its debt. This is a smart decision by management not to get them into a tough situation where they have to sell large amounts of Bitcoin all at once to pay back debt.

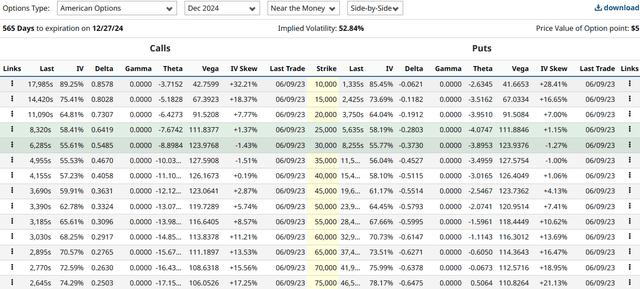

Bitcoin Options (Bar Chart)

Source

This would give MicroStrategy a breakeven at around 15k when the first bond matures. The furthest out the options market goes is December 2024. The 15k strike put option expiring in December 2024 has a delta of -0.12. We can use this to interpret that the market is telling us that MicroStrategy has a 12% chance of bankruptcy based upon options pricing relative to MicroStrategy’s breakeven. I do believe though that the chance is above 12% as this options chain expires in December 2024 prior to the maturity of the bonds and it uses futures pricing not spot; the Bitcoin futures market is in contango so further out contracts are higher in price than current spot. Because of this, I do think that the probability of landing below the breakeven is closer to 15%.

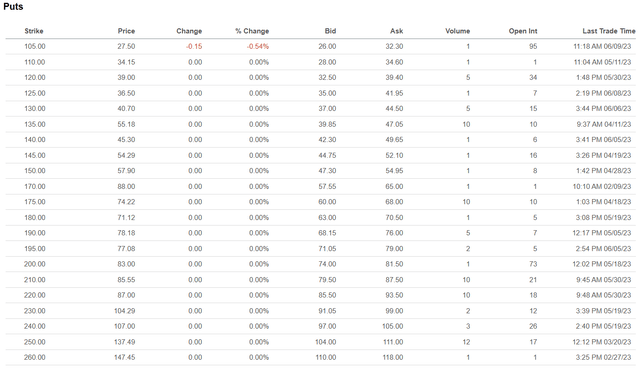

MicroStrategy Put Options (Seeking Alpha)

Source

From here we can see whether the market is pricing this risk of MicroStrategy going bankrupt. A simple way of looking at this is to look at far out, in this case, Jan 2025 put options. Then we can select a deep OTM put option which would be the $20 strike.

If MicroStrategy were to go bankrupt this put option would make $20; in my view, the probability of that happening is 15%. The mid-price for the premium is $1.05. Of course, the bid ask is wide due to the illiquidity of a far-out strike.

In other words, the following is the risk/reward/probability:

Risk: $1.05

Reward: $20

Probability: 15%

To know whether these pot odds are worth it, divide 100 by the probability. In this case 100/15 = 6.67. Since 6.67 is lower than the risk/reward of around 20 fold, this trade would be worth it from a pot odds perspective as the market is underpricing the scenario of bankruptcy. If you disagree with my probability you can plug in your own when doing this pot odds analysis.

The Bigger Immediate Issue Is Stock Dilution

Even though I believe that the risk of MicroStrategy going bankrupt is underpriced by the market, the more immediate issue is the lack of current assets the company has and how it will fund its working capital needs.

Current assets are lower than current liabilities and with consistently negative EBIT(I use EBIT over net income due to the changes in figures that taxes has) the business will continue to burn cash. So how will they fund this cash burn?

With Bitcoin down from its highs along with higher interest rates, it is unlikely that MicroStrategy could issue more debt or at least do so at reasonable terms. Not to mention companies like FTX going under has caused many in the market to distrust any company involved in the crypto space.

I think this leaves MicroStrategy with only one option: stock dilution.

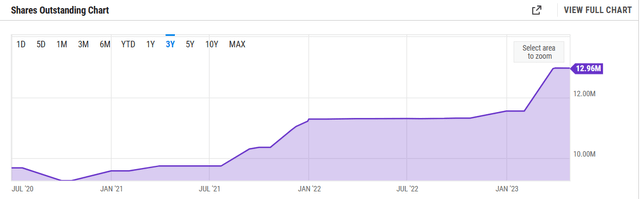

Below are the outstanding shares for MicroStrategy:

Outstanding Shares (Y Charts)

Source

The outstanding shares have already gone up a lot. For now, it hasn’t been that big a deal to the market because there is both demands for the stock and the market capitalization of the company trades well above the NAV of the Bitcoin it owns.

What I do see as a big risk though is that eventually the company issues so much stock that eventually the shares of the company trade below the NAV. In this situation, if MicroStrategy wanted to continue to fund its day-to-day operations it would make a lot more sense to sell Bitcoin, but this would of course lower its NAV and it removes the initial reason for many Bitcoin bulls even buying the stock, which is that it not just owns, but is levered on its Bitcoin.

This really creates a situation where the only way I see MicroStrategy’s stock going up is if we see a large rise in the price of Bitcoin.

SEC Litigation Risk

Another out-of-the-box risk I find with MicroStrategy is SEC Litigation risk. We’ve already seen both Binance and Coinbase get hit with lawsuits from the SEC and I see potential risk for a company like MicroStrategy.

This wouldn’t be the first time that MicroStrategy is hit with a lawsuit. The SEC made MicroStrategy and three executive officers pay large fines in 2000 as part of a settlement for accounting fraud. More recently Michael Saylor was suited by the District of Colombia for tax evasion. Although the judge ended up ruling in favour of Michael Saylor due to a technicality under the False Claims Act, I do believe that lawsuits like this bring the perception of bad public relations and question the ethics of the management.

Why Do So Many Buy This Stock?

This brings up a very obvious question: why in the world does anyone buy this stock?

I’m sure many bulls in the comment section of this article will be able to answer why, and I would encourage them to, as I would be interested in hearing out why they bought this stock.

As I mentioned at the beginning of the article, I’m viewing Bitcoin from an agnostic lens when writing this article. My view is that even if one were very bullish on Bitcoin they could just buy Bitcoin in their own custody. Buying Bitcoin itself removes idiosyncratic risk from MicroStrategy and the whole initial purpose of Bitcoin was to have a bearer asset that only you would have custody of, as other players in the market couldn’t be trusted to hold the Bitcoin for you. Bitcoin now does attract a different audience than it used to attract many years back; many years ago Bitcoin was really only bought by libertarians or anarcho-capitalists who wanted a separate currency that government didn’t have control over. Those days are long gone, and I do find that nowadays the buyers of Bitcoin are primarily retail investors who like the upside potential of Bitcoin, but who have no real philosophical reason for buying it.

This brings me to why I do believe so many bought this stock, which is leverage. While one could buy Bitcoin on their own or through a closed-end fund they wouldn’t get the amount of leverage that MicroStrategy offers. Even though it is possible to buy Bitcoin on margin, there is no way a retail investor can issue non-callable notes the way MicroStrategy did to leverage up while trying to reduce the risk of ruin.

Two Main Risks To The Bearish Thesis

There are two main risks I see in my bearish thesis. The first is that Bitcoin goes higher. This would of course send the stock higher as it is essentially a leveraged play on Bitcoin. One way to hedge this risk is to do a long-short trade, where Bitcoin is bought and MicroStrategy is shorted, which hedges out the risk of Bitcoin going higher. Another way to hedge this risk, and the method I prefer, is to buy far-dated, deep OTM put options.

The second risk which is one that would truly come out of left field is the risk of their software and cloud-based business turning into a legitimate cash cow. I find this unlikely as the business has been struggling for the last three years.

The Bottom Line

In my view, the bottom line here is that MicroStrategy has essentially turned into a levered Bitcoin fund of sorts. I believe the risk of the company not being able to pay back its debt is far higher than what the options market is pricing. On top of this MicroStrategy is now getting into a situation where it has no choice but to dilute shareholders to continue to run the company with the large amount of cash burn it has. I also very much dislike the management of the company, as what management in their right mind would not just buy Bitcoin (an extremely high-risk & high-volatility asset that might not be suited to all shareholders), but leverage it to the moon, all while turning their company into a quasi-Bitcoin fund? In my opinion, any management that does that lacks capital allocation, risk-taking, and risk-management skills.

If one is a Bitcoin bull I believe it makes a lot more sense to buy Bitcoin directly than to buy this stock.

Read the full article here