Designer Brands Inc. (NYSE:DBI) has seen its stock price jump by 28% over the last five days after reporting its Q1 2023 Earnings earlier this week. While exciting, this is an exaggerated market response to the news of a potential $100 million share repurchase based on debt approval and excitement around a renewed emphasis on its Nike (NKE) partnership. Designer Brands missed revenue and EPS expectations for Q1 2023 and lowered its FY 2023 guidance due to consumer discretionary headwinds, pushing a promotional environment across the retail industry.

Stock Trend Post Q1 2023 Earnings Report (seekingalpha.com)

Designer Brands has been redeveloping its business by increasing its in-house brand sales through strategic acquisitions and increasing its presence in casual and athletic footwear growth categories. Although Designer Brands remains an attractive long-term play, investors should be cautious of the high short interest in the stock and the negative impact of consumer discretionary headwinds predicted to continue into the next few quarters. Therefore, I recommend a hold position until the industry shows signs of recovery.

Designer Brands Overview

In my earlier articles, I give an overview of Designer Brands and its growing in-house brand strategy and move into the casual and athletic footwear category. In Q1, own-brand penetration increased to 27% of net sales. While we see retailers across the industry take a hit due to strong headwinds, Designer Brands is managing to create a long-term strategy showing resilience in more challenging economic times. Although sales decreased year-on-year, there has been an increase in total sales across the last two years.

Designer Brands has made significant acquisitions in the past year, adding three new brands to its portfolio in the casual and athletic categories. These brands include Keds, Le Tigre, and Topo Athletic. Keds has already been successfully integrated into the company and has shown a notable increase in wholesale growth compared to its previous performance under Wolverine. It is anticipated that Keds will contribute approximately $75 million to $85 million in net sales across various channels, including wholesale, DTC, International, and Canada.

Acquisition of Keds (sec.gov)

Le Tigre, an economically priced fashion-forward athletic footwear brand, is scheduled to launch in the late summer to benefit from the back-to-school season. Finally, Topo Athletic, a specialty athletic brand, will be integrated across wholesale and direct-to-consumer channels.

Acquisition of Topo (sec.gov)

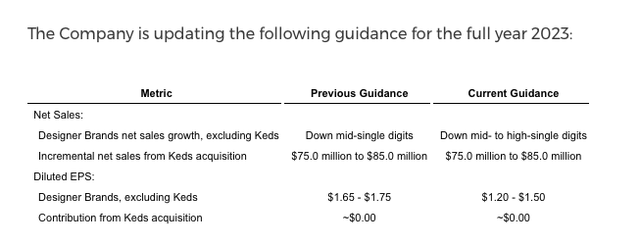

In addition, Designer Brands will have sole permission to use the Hush Puppies brand in the United States and Canada. Nike’s partnership with the company has been increased, covering men’s, women’s, and children’s products. Previously, Nike accounted for 6% of sales. Despite having established plans for growth, sales could be affected by challenges in the consumer market in 2023. As a result, management has revised their earnings per share forecast to range between $1.20 and $1.50, reflecting a higher level of uncertainty.

Designer Brands Q1 2023 Financials

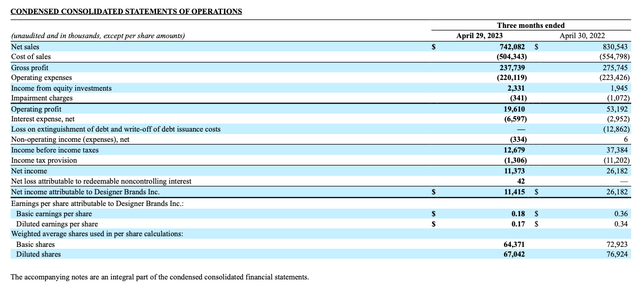

Historically, Q1 is typically one of Designer Brands’ two most significant selling periods of the year. Although sales have grown over two years, due to its promotional and clearance strategy, we saw net sales decline 10.7% YoY to $742.1 million, affected by a constrained discretionary consumer, highly promotional retail environment. Gross profit decreased YoY from $237.7 million to $275.7 million one year prior, and the margin was 32% compared to 33.2% over the same period. Net income reduced from $36.7 million to $14.3 million YoY.

Income Statement Q1 2023 vs Q1 2022 (sec.gov)

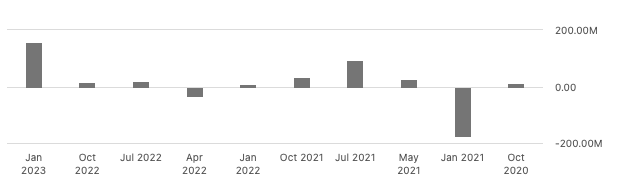

If we look at the balance sheet, we see $50.6 million in cash. Furthermore, the company has $200.3 million in cash in its available revolving credit facility. Levered free cash flow was positive at $160.77 million TTM and has been positive over the last two financial years. Furthermore, Designer Brands authorizes the stock repurchase of up to $100 million, based on acquiring a $135 million loan agreement.

Levered Free Cash Flow by Quarter (seekingalpha.com)

DBI Stock Valuation

Over the past year, Designer Brands stock has had a disappointing performance, decreasing in value by 45.15%. Currently, it is trading below its one-year price target of $9.33 and has been rated as a Hold by Wall Street analysts.

Average Price Target (seekingalpha.com)

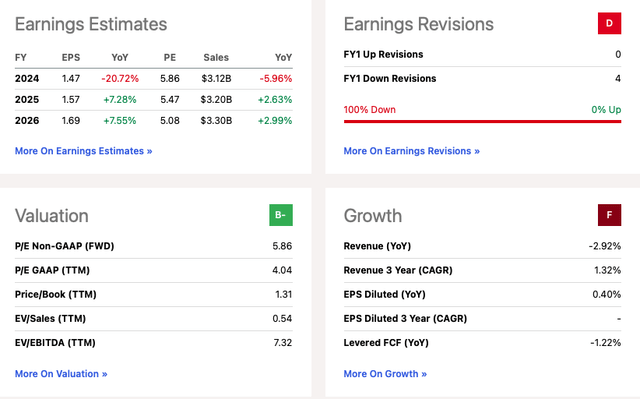

The stock has a low price to earnings ratio of 5.86, which may seem appealing. However, we should be wary of the decrease in sales growth from the previous year, which is expected to continue throughout the rest of the financial year due to the current promotional environment. Additionally, the company has lowered its guidance for earnings and it may take some time for the acquisitions to become profitable.

Earnings and Valuation (seekingalpha.com)

Risks

Designer Brands delivered a weaker-than-expected Q1 2023 amidst strong consumer discretionary headwinds, which have decreased consumer demand and pushed a promotional environment within the retail sector. This can cut into already slim gross margins in a competitive environment and negatively impact the company’s growth performance. Consumer discretionary stocks are sensitive to the economic climate. Therefore, we would require the market to recover before sales can recover.

Final Thoughts

Designer Brands usually performs well in the first quarter, but this year it has not met expectations. This has led to a weaker forecast for FY 2023, and management has lowered their guidance after seeing the results. The company also needs to continue selling items on promotion. While Designer Brands has a promising long-term plan for their own brand growth, I recommend a hold position until consumer demand improves.

FY 2023 Outlook (sec.gov)

Read the full article here