Investment Thesis

Cracker Barrel Old Country Store, Inc. (NASDAQ:CBRL) should be able to sustain its topline growth despite the near-term uncertain macroeconomic conditions through price increases as well as increased advertising around its value meal offerings at lower price points to attract the cautious consumer in an inflationary environment. In the medium to long run, CBRL’s revenue should benefit from digital enhancement, growing off-premise business, diversification of customer base, and acceleration of new unit expansion.

On the margin front, the company should benefit from moderating inflation, price increases, the company’s cost-saving initiatives, and productivity gains. The stock is trading at a discount to its historical averages and has a compelling forward dividend yield of 5.7%, and I believe the recent dip in the stock price has provided an attractive entry point to bet on CBRL’s long-term growth prospects.

Q3FY23 Earnings

Last week, Cracker Barrel Old Country Store, Inc. reported earnings for its third quarter of fiscal 2023 that fell below expectations. The company’s revenue reached $817 million, showing a 5.4% year-over-year increase, but it was lower than the consensus estimate of $846 million. The adjusted earnings per share (EPS) was $1.21, reflecting a 6.2% decline compared to the previous year, and it also fell short of the consensus estimate of $1.34. Furthermore, the adjusted operating margin experienced a 20-basis points year-over-year decline, settling at 4.1%.

While revenue saw growth attributed to price increases and value meal offerings, there was a larger-than-anticipated decline in traffic towards the end of the quarter, resulting in a revenue miss. The decline in adjusted EPS and adjusted operating margin can be attributed to rising input costs due to inflation, increased expenses on advertising and maintenance, as well as lower traffic.

Revenue Analysis and Outlook

In my previous article, I emphasized the company’s long-term sales growth prospects and recommended a buy rating on the shares, considering their lower-than-historical valuation. I also acknowledged that while there are near-term uncertainties surrounding traffic count, the company should be able to grow revenues thanks to its price increases. The same phenomenon was apparent in the company’s Q3 results.

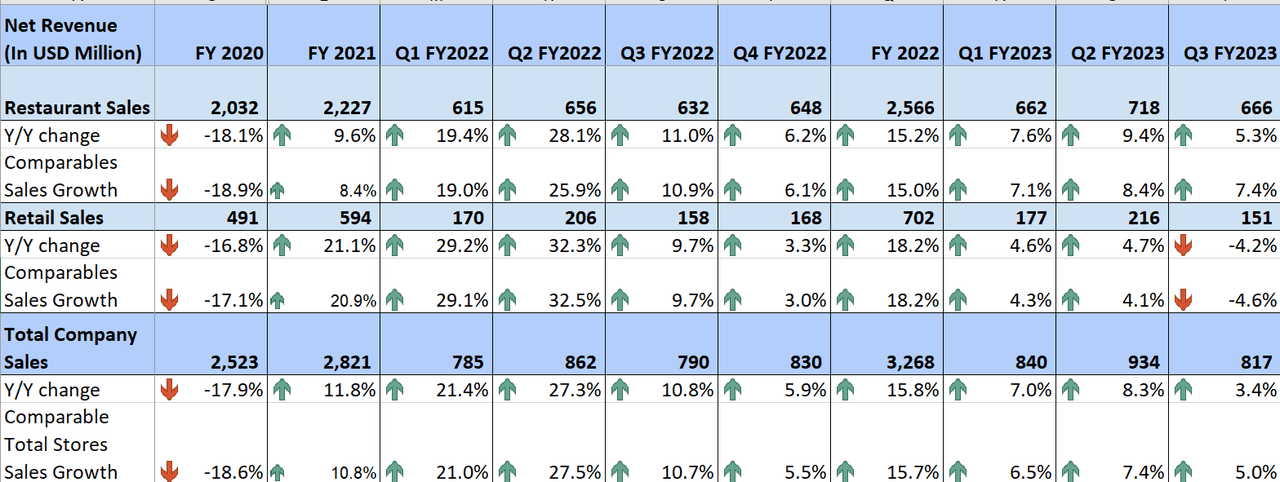

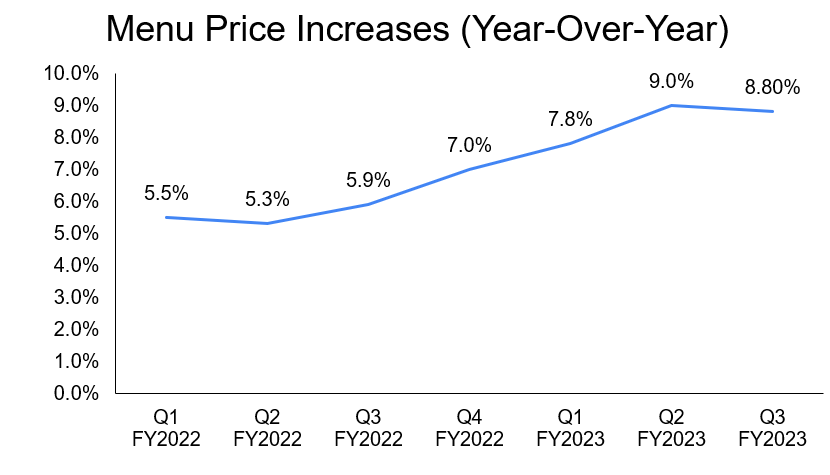

During the third quarter, the company initially experienced an improvement in guest traffic momentum. However, towards the end of March and in April, customers began reducing discretionary spending on activities like dining at casual restaurants and purchasing apparel and gifts, in response to rising inflation and macro uncertainty. This resulted in a larger-than-expected decline in traffic count for the entire quarter. While this decline in guest traffic had a negative impact on the entire casual dining full-service restaurant sector, Cracker Barrel managed to offset the decrease with price increases of 8.8 percentage points, mix improvements of 1.8 percentage points, and its affordable value offerings. As a result, sales grew by 5.4% year-over-year, reaching $817 million. On a comparable sales basis, total company sales increased by 5% year-over-year, reflecting a 7.4% growth in the restaurant segment and a 4.6% decline in comparable sales for the retail segment.

CBRL’s Historical Revenue (Company Data, GS Analytics Research)

Looking ahead, although there are still lingering uncertainties regarding consumer health, I believe that the company is well-positioned to maintain its sales growth in a challenging macroeconomic environment and achieve long-term growth. In the near term, Cracker Barrel should be able to mitigate the impact of lower consumer traffic by implementing price increases and offering attractive value propositions at lower price points. To drive sustained growth over the long term, the company can leverage strategies such as improving its demographic mix, expanding its number of locations, and capitalizing on the growth of off-premise and online platforms.

The company has been implementing pricing actions since the start of 2022 and anticipates further increases in the upcoming quarters. These price adjustments in the latter half of the current fiscal year are expected to support sales growth in the first half of 2024, thanks to their carryover impact.

CBRL’s Historical Price Increases (Company Data, GS Analytics Research)

Furthermore, CBRL has effectively managed its menu offerings by ensuring a balance of items across different price points. The company introduced over 20 items priced under $12, encompassing both signature dishes and new innovations, to provide a diverse range of options for price-conscious customers seeking the experience of casual dining at a lower cost. To attract cautious customers, the company has also ramped up its advertising efforts to promote these everyday value offers on a larger scale. In Q3 FY23, CBRL observed positive traction for these value offerings and expects improved traffic trends during the peak summer months of June and July, when customers typically travel more frequently. This strategic approach should help CBRL combat the impact of softening consumer demand caused by inflation. I believe that price increases and diverse value offerings at various price points will support sales growth in the near term.

The company’s long-term revenue growth prospects also look good. CBRL’s off-premise business, which accounts for 19.1% of its total restaurant sales, is experiencing rapid expansion. This growth is primarily driven by the catering business, which saw a 35% year-over-year increase in Q3. CBRL has doubled its marketing investments in the catering business, aiming to reach a target of 25% of total off-premise sales (currently at 20%) and surpass $100 million in sales by the end of fiscal 2023. This growing off-premise segment should contribute to the company’s long-term growth trajectory.

Additionally, CBRL is enhancing its digital platform by launching a loyalty program in July. Loyalty programs offering discounts, personalized promotions, and engaging online activities have gained popularity since the pandemic. These programs have become key drivers not only for the restaurant sector but also for the broader consumer sector, helping to attract new customers, retain existing ones, and foster brand loyalty. As mentioned in my previous article, CBRL aims to diversify its customer base by attracting young consumers, and the loyalty program can play a crucial role in achieving this objective, appealing to young customers and supporting the company’s efforts to diversify across all age groups. Therefore, I anticipate that the launch of CBRL’s loyalty program on its digital platforms will enhance customer engagement and drive sales growth in the years to come.

Lastly, the company is focused on accelerating its net unit expansion in the coming years, particularly with the opening of Maple Street Biscuit Company (MSBC) restaurants, which management believes hold significant long-term growth potential for CBRL. In the fourth quarter, CBRL plans to open 5-7 new MSBC restaurants, aiming to achieve a total of approximately 15 new openings in FY23. Overall, I remain optimistic about CBRL’s efforts to sustain its top line in a challenging macroeconomic environment and drive sales growth in the long run.

Margin Analysis and Outlook

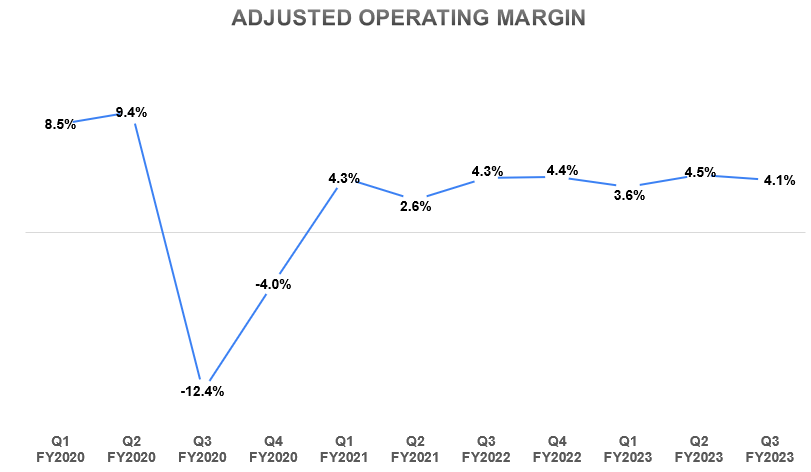

In the third quarter of fiscal 2023, Cracker Barrel, like other restaurant companies, encountered challenges from inflationary pressures, particularly in the increased costs of produce, dairy, and eggs. The company saw a 4.3% Y/Y increase in commodity costs. Additionally, the company faced difficulties due to labor wage inflation, which experienced a year-over-year increase of 5.5%, as well as higher costs associated with advertising and maintenance. However, the impact of these challenges was mitigated to some extent through price increases, resulting in an adjusted operating margin of 4.1%, reflecting a 20-basis points decline compared to the previous year.

CBRL’s Historical Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking ahead, management anticipates that commodity inflation will remain flat year-over-year in the coming quarter, while wage inflation is expected to increase in the mid-single digits. Although this will continue to pose a challenge for margin growth in Q4 FY23, the company expects to offset these costs through price increases in the upcoming quarter. As we enter the next fiscal year, I anticipate a recovery in CBRL’s margins as inflationary comparisons ease with moderating inflation. Furthermore, the carryover pricing from the second half of FY23 is expected to contribute to margin recovery in the first half of FY24. The company is also making progress with its new labor management system, which has been implemented in over 460 restaurants, with completion expected in June for the remaining locations.

This system assists the company in enhancing visibility into labor costs and increasing productivity by optimizing labor allocation based on specific business requirements. For example, catering operations may have different labor demands compared to dine-in services, and the system helps stores match labor resources accordingly. The company now expects cost savings of $30 million (up from the previous estimate of $25 million) in FY23 as the rollout nears completion. These cost savings are also expected to further accelerate in FY24. This will aid the company in margin recovery and expansion. Additionally, Cracker Barrel is experiencing improvements in employee turnover and increased retention rates, which should reduce new hiring costs and enhance productivity among existing employees. Therefore, these cost savings and productivity gains are expected to support margin growth beyond FY23.

Valuation and Conclusion

Cracker Barrel’s current valuation is at 17.03x the consensus EPS estimate for FY23 of $5.35 and 13.83x the consensus EPS estimate for FY24 of $6.59. This valuation is lower than its historical 5-year average forward P/E of 22.97x. I remain optimistic about the company’s long-term growth prospects, which should be driven by digital enhancements, new unit expansion, and a diversifying customer base. I also have confidence in management’s initiatives to navigate the near-term uncertainties surrounding guest traffic slowdown through strategic pricing and value meal offerings across different price points. Additionally, the company’s compelling dividend yield of 5.7% adds to its long-term return potential. With the recent dip in stock price, the valuation has become even more attractive, making it an opportune time to enter a long position. Therefore, I believe the stock is a good buy at the current levels.

Read the full article here