Thesis

Based on my analysis, I recommend a buy rating for Upland (NASDAQ:UPLD) primarily due to its significant undervaluation, evident from its current trading at modest multiples.

Company Overview

Upland Software is a provider of cloud-based enterprise work management software. The company is headquartered in Austin, Texas and was founded in 2010. Upland Software’s solutions are designed to enhance productivity, improve efficiency, and streamline business operations for companies across various industries.

At its core, Upland offers a comprehensive suite of 30+ products and services that empower businesses to manage their work and drive results. The company’s portfolio encompasses a range of solutions tailored to meet the diverse needs of different departments within an organization. In a way, the company reminds me of a mini-HubSpot (NYSE:HUBS), a one-stop cloud shop for all of a businesses’ needs.

In the following sections, I’ll provide an analysis of Upland’s financials, valuation, risks, and potential catalysts. Throughout, I’ll discuss the rationale behind my thesis.

Financials

There are two main things from Upland’s financials that I want to highlight:

- Stagnating Revenue Growth

- Large Cash Position (Acquisitions?)

Stagnating Revenue Growth

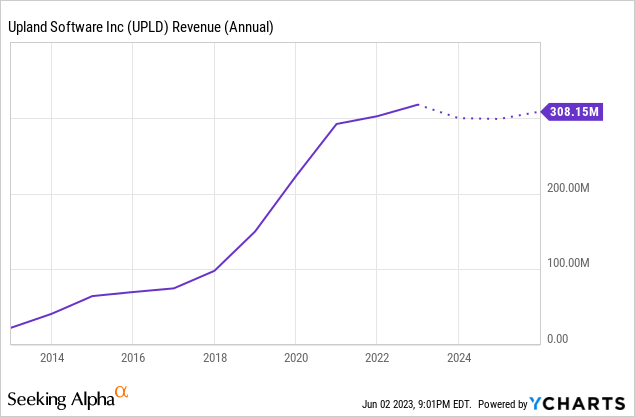

Upland’s financial performance has displayed a notable shift in recent years. After experiencing consistent year-over-year revenue growth of over 30% from 2013 to 2020, the company has struggled to achieve substantial top-line growth in the past couple of years. In 2021, the year-over-year growth was a mere 3.51%, followed by a slightly improved rate of 5.06% in 2022. The graph below illustrates this flattening revenue curve, which is expected to persist throughout 2024.

The stagnation in revenue growth raises concerns for investors, especially considering Upland’s position as a facilitator of businesses’ transition from on-premise, legacy services to cloud-based solutions. One would anticipate significant tailwinds for a company operating in this space, as more businesses seek cloud-based software solutions. However, factors such as intense market competition and Upland’s broad portfolio of 30+ services may be contributing to the slowdown. While Upland aims to be a comprehensive one-stop-shop for businesses, the challenges of excelling in such a wide range of services can result in customers opting for specialized alternatives or sticking with their existing platforms, potentially bypassing Upland entirely. And even if customers are looking for one-stop shop solutions, it would be difficult to choose Upland over larger, more-complete offerings from companies such as HubSpot.

Despite its role in facilitating cloud adoption, the company faces challenges from intense competition and the complexity of offering a broad suite of services. These factors may explain the slower revenue growth and suggest the need for strategic considerations to regain momentum in a highly competitive market.

Large Cash Position

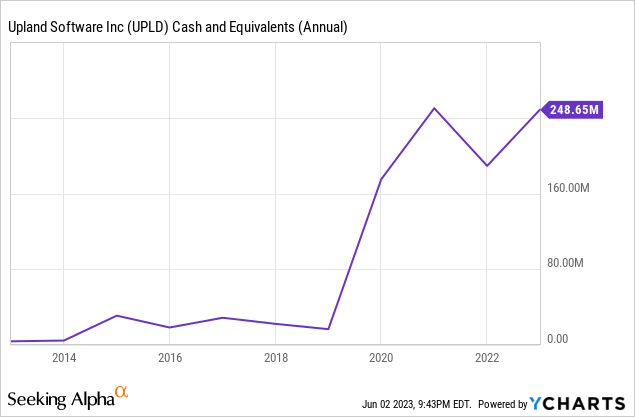

When analyzing Upland Software’s balance sheet, one notable aspect is the company’s substantial cash holdings of approximately $250 million. This sizable cash pile is particularly noteworthy considering Upland’s current market cap is less than $100 million.

The significant cash reserves held by Upland reiterate their longstanding focus on acquisitions as part of their growth strategy. The company has a track record of completing 31 acquisitions to date and actively seeks additional opportunities in various areas.

On their website, Upland outlines their acquisition strategy and criteria, expressing interest in sectors such as business operations, IT, marketing, project management, sales, CRM, and HR. They have also established five financial criteria for potential acquisitions, including revenue ranging from $5 million to $25 million or more, a net dollar retention exceeding 90%, gross margins over 70%, organic growth of 10-20%, and an average annual recurring revenue per major account surpassing $25,000.

However, it is worth noting that Upland has not completed any acquisitions in over a year. Their last transaction occurred when they acquired BA Insight in February 2022. This lack of recent acquisitions may be a contributing factor to the company’s slowdown in revenue growth, as organic growth alone appears to be insufficient to drive improved financial performance.

Considering the current market conditions, where many companies are valued significantly lower than they were just a couple of years ago, it appears to be an opportune time for Upland to be proactive in pursuing acquisitions. With a substantial cash position, I would have expected Upland to have been more active in the M&A space in the past year.

In their most recent earnings call, management addressed this situation when asked by an analyst during the question and answer portion of the call. Jack McDonald, Upland’s CEO, said, “We’re definitely still looking at deals. We’re actively in the market. I haven’t seen the price adjustment and private market values that I’d want to see. And of course, we’ve got capital, and we control the timing. So we’re going to be patient and move when it makes sense. But as of right now, I haven’t seen enough of a price adjustment to make us super excited, but I’m sure it’s coming.”

Part of me wants to buy into what Mr. McDonald said here, but the other part of me wants to lean towards approaching his comments with skepticism. For context, Upland completed one acquisition in 2020, three in 2021, and two in the early months of 2022. These years comprise a period when company valuations were certainly not cheap. In some cases, valuations were astronomically high. And yet, Upland made six total acquisitions during this time period. Contrast this with management now, who are saying that they are still waiting for valuations to come down. I think that management may be simply riding the wave, rather than trying to be contrarians in the market.

As I see it, the pursuit of strategic acquisitions could potentially reignite growth and address the revenue stagnation that Upland has experienced. Looking forward, I believe that this should be something on the forefront of management’s priorities. Although, it remains to be seen how much initiative they will take on this front in the near future.

Valuation

Upland’s valuation shines bright for investors amidst recent stagnation in the growth of their business. Despite the challenges they have faced, Upland’s valuation not only factors in their current performance but also leaves substantial room for potential upside, making it an intriguing prospect for investors.

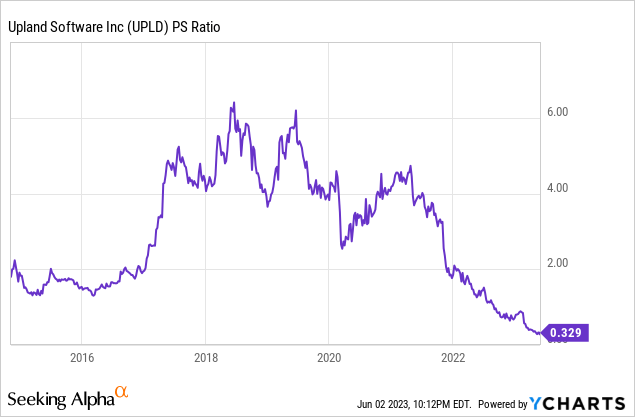

Currently, Upland is trading at remarkably low valuation multiples. Their Non-GAAP P/E ratio stands at 1.7x, significantly below the sector median of 18.75x. Similarly, their TTM Price/Sales ratio is only 0.3x, compared to the sector median of 2.8x. As I write this, Upland is trading at a FWD P/E of 3.19. Overall, the SeekingAlpha factor grades give Upland’s valuation a solid “A,” which seems reasonable based on all of their relative valuations.

These substantial discounts in Upland’s valuation metrics raise an important question: are they justified, or could the market be potentially overreacting to Upland’s recent challenges?

In my opinion, Upland’s lackluster performance as of late does not necessarily warrant such a significant undervaluation. While it may be unrealistic to expect them to reach the sector median valuation multiples, or come even close, a meager valuation multiple of even 1x TTM revenues (which is still close to only 1/3 of the sector median) would not be unwarranted. Applying such a multiple would value the company at approximately $9-10 per share, which I think would be a fair value of the company.

Risks

The biggest risk for Upland lies in the potential continuation of slowing revenue growth, which could have significant implications. This risk becomes more pronounced if the company continues their recent struggles to identify and execute suitable acquisitions to drive their growth strategy forward. Using their track record of 31 completed acquisitions as an indicator, Upland has obviously relied heavily on inorganic expansion to fuel their business growth, making the absence of suitable acquisition opportunities a concerning factor.

Moreover, Upland operates in a highly competitive landscape. They face intense competition from both established players and emerging startups that offer similar services and solutions. Larger competitors with stronger market presence and resources pose a significant challenge. These competitors not only offer a comprehensive suite of services but also have proven track records of delivering them effectively. Upland’s ability to effectively differentiate themselves and stand out amidst competition becomes crucial for maintaining their market position and sustaining growth. If they simply opt to play catch up to larger competitors, or aim to only copy their offerings, it’s going to be difficult for Upland to attract customers.

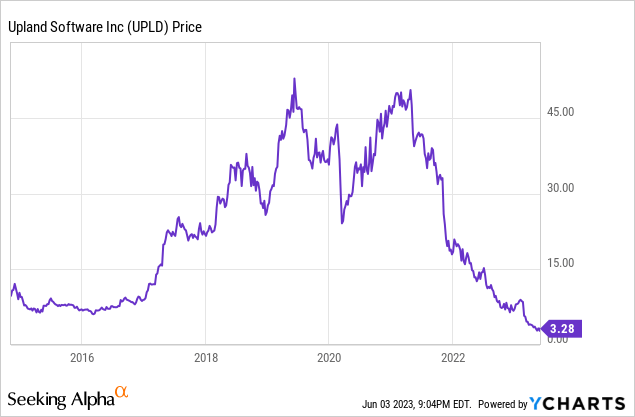

With this being said, I do find it challenging to envision Upland’s stock dropping much further than its current levels. The stock has already experienced a decline of over 90% from its peak in 2019 and is presently trading at significant discounts when evaluated on a multiples basis. Given these factors, I believe that a considerable portion of Upland’s downside risk has already been mitigated for investors.

Catalysts

In my view, Upland is currently undervalued, and the market appears to be gradually recognizing this. Since June 1st, the stock price has already experienced an increase of over 10%, and I anticipate that it may continue to rise. Despite this modest price correction, I believe that the market will not fully acknowledge the company’s value until Upland executes a significant and meaningful acquisition. Such an acquisition has the potential to act as a catalyst for the company’s stock price.

As for the timing of this catalyst, I’m uncertain, particularly in light of recent management comments indicating that valuations have not fallen enough for them to actively pursue mergers and acquisitions. Nevertheless, the current undervaluation of Upland’s stock provides investors with a margin of safety that they can rely on until the market fully recognizes the company’s true worth.

Conclusion

In conclusion, Upland presents an opportunity for investors primarily due to its significant undervaluation, evidenced by its trading at modest multiples. The company’s stagnating revenue growth and lack of recent acquisitions pose risks, but its large cash position provides potential for strategic expansion. Despite the challenges, Upland’s valuation metrics stand at remarkably low levels compared to the sector median, indicating substantial upside potential. While the market has yet to fully recognize the company’s value, recent price movements suggest a gradual acknowledgment. For these reasons, I’m bullish on Upland in the short to medium term.

Read the full article here