Bilibili (NASDAQ:BILI) is a Chinese online long-form video-sharing entertainment platform recognized for its anime, comics, and gaming / ACG content, which has gained popularity among Generation Z / Gen Z users. The company has four revenue streams – advertising, mobile games, VAS / value-added services, and IP derivative/e-commerce merchandising.

Overall, BILI appears to be an interesting business that is well-positioned to capture the growth of the video-based industry in China. The focus on Gen Z is also a compelling factor. There are +450 million of the Gen Z population in China alone, and the group has been the key consumption driver of video-based content.

BILI has been a fast-growing company since its founding. However, revenue growth has been declining as profitable growth has become the key focus going forward. Growth may decline further to +9.6% in FY 2023, though losses will narrow.

The management has set a target to reach breakeven in 2024, and I expect the stock to benefit from some catalysts that will drive continuing growth as well as margin expansions in FY 2023, getting the business closer to the objective.

I give BILI an overweight rating in this first coverage. Trading at ~$15 per share at the time of writing, my FY 2023 target price model suggests that there is a 15% upside.

Catalyst

There are a few initiatives that may continue driving growth and margin expansion for BILI. First, the focus shift towards daily active user / DAU-oriented (instead of the monthly active user / MAU-oriented historically) growth and the live streaming e-commerce, which was just launched in 2022, should bring a positive impact on advertising and VAS businesses through the expected higher engagement and time spent on the platform.

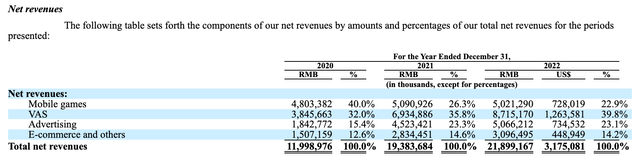

While BILI has historically generated most of its revenues from VAS and mobile gaming businesses, advertising has been growing rapidly over the last two years, and as of 2022, it stood as one of the top two revenue drivers for BILI. The fact that BILI has been gaining a reputation in China’s online advertising market since last year, coupled with the above-industry growth today suggest that there is still a lot of room for expansion.

BILI 20F

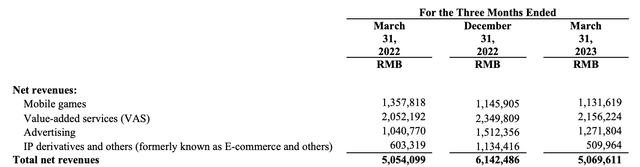

Advertising made up only ~15% of BILI’s revenue in 2020. Fast forward to Q1 2023, it was the second-biggest revenue stream after VAS with ~23% of revenue. With 22% YoY growth in Q1, advertising revenue even grew faster than the industry average, demonstrating demand for BILI’s advertising offering. As such, I think that it is quite possible for the advertising business to see a steady +20% growth throughout FY 2023.

BILI presentation

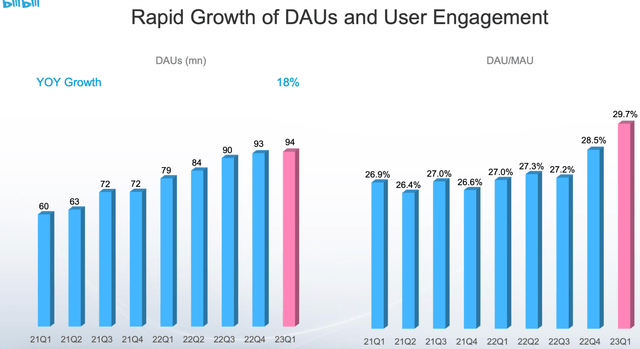

The success in advertising growth may also stem from BILI’s shift of focus towards driving DAU, instead of MAU growth, since last year, which has been driving higher engagement and time spent on the platform – both attractive metrics for advertisers to gauge audience quality and potential ROI. Total time spent on the platform was up 19% YoY in Q1, while DAU/MAU ratio has been on an uptrend and was at ~30% in Q1, even as BILI made a considerable 11% cut on operating expenses to improve its bottom line.

BILI presentation

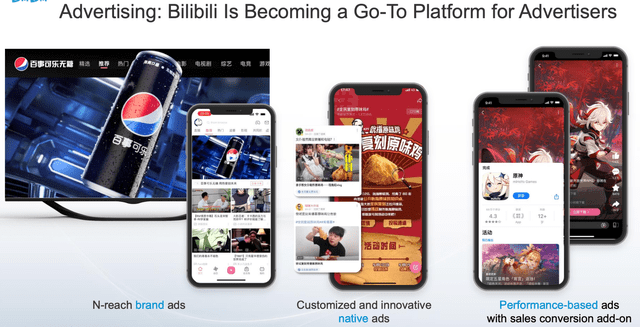

Moreover, the recently-launched live streaming-based e-commerce should also facilitate further ad inventory expansion, creating opportunities for advertisers to buy up more ad space and increase spend on BILI’s platform. In particular, I expect performance-based ads to benefit from this new feature. Performance ads saw a 50% growth in Q1, with 30% of the total spend on performance ads already coming from this new live-streaming e-commerce business.

As I expect advertising revenue to continue growing its share in the revenue mix, it may also potentially surpass VAS as the largest revenue stream in the next few years. In Q1, VAS only saw a 5% revenue growth though it has been the core business and the largest revenue stream.

VAS’ revenues come primarily from the premium membership subscription as well as sales of virtual items such as gifts for live broadcasters/content creators. I think that as BILI continues to integrate e-commerce into live broadcasting and therefore provides a new way for content creators to monetize, such as through live product promotion, sales of virtual items may potentially decline while advertising revenue picks up.

On the other hand, I also expect BILI to see margin expansions in FY 2023, though it will potentially still generate an operating loss. This will be driven by the growth in the higher-margin revenue streams such as VAS and advertising. Meanwhile, IP derivative, which is a lower-margin business, will continue to decline as the management suggested that it would prioritize profitability over growth in that segment. The segment already saw a decline of 15% in Q1.

BILI presentation

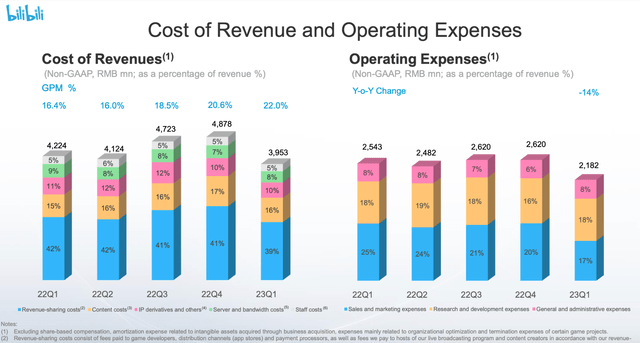

As a result, there seems to be room for more cost efficiencies, especially in content sharing, bandwidth, and IP derivative costs.

The growth in live-streaming activities should enable BILI to expand bandwidth capacity at a lower cost per Mbps / megabyte per second. The content-sharing cost reduction will primarily be helped by BILI’s commitment to be more selective in its partnership strategy with content creators. BILI has historically spent over 40% of its revenue on subsidizing and paying content creators to produce content on its platform. In Q1, the figure declined to 39% of revenue, and given the early stage of the initiative, it may potentially see a further drop in Q2 and beyond.

Finally, while the gross margin expansion to 22% in Q1 in just over a year was already above expectation, I believe that expansion to the +25% range is also possible as the IP derivative business continues its decline as BILI seeks a more controlled growth here, lowering its cost of revenue from 10% to maybe +7% of revenues.

Risk

I think that some of the key risk factors on BILI are the hit-or-miss nature of its gaming business, China’s regulatory uncertainty, and competition around e-commerce live streaming.

reuters

In general, I view the gaming business and China’s regulatory environment to be on par in terms of their uncertainties. Regulatory risk, in particular, has been quite a concern for companies in the gaming space in China. The less favorable regulatory outlook in 2021 and 2022, in particular, has negatively affected BILI’s gaming business.

BILI’s 20-F

Despite its high margin, BILI’s mobile gaming growth has been flat and even on a slight downtrend in recent times. As the crackdown eased in March 2023, BILI announced that it would launch 13 new games in 2023 and aim for a better outlook than in 2022. However, given the long development time as well as the hit-or-miss nature of the gaming industry, it is still relatively risky to base revenue expectations on the business.

The management has set an expectation for the gaming business to see +20% growth in FY 2023, which I consider a very ambitious and high-risk high-reward sort of expectation, given the unpredictability of the revenue stream.

Additionally, I expect the tight competition in the live streaming business in China to continue to add pressure on BILI from time to time, which may affect its profitable growth and breakeven goal in 2024.

For instance, BILI relies a lot on its content creators for platform growth. BILI spent on average +40% of its revenue towards content-related activities, such as subsidies to content creators with followers below 10,000 and revenue-share payment to revenue-generating content creators. However, given BILI’s more selective approach with its content investment to drive bottom line expansion going forward, the risk of these content creators leaving BILI’s platform to join other live-streaming platforms may increase.

Ultimately, BILI would also want to avoid less favorable media coverage about its practice around content creator partnerships, which may potentially create downside risk for the stock. A question about this particular issue was raised in the Q1 earnings call, which was quickly addressed by the management in a rather defensive tone:

Well, I think you’re referring to an article released in April about many — the article claims that many creators on Bilibili stopped uploading new content to the platform. I read it myself, and I think this article is nothing but misleading. And this article mentioned three content creators who paused their update — paused their video content updates. Out of millions of content creators we have on Bilibili, the article mentioned only three. And two of those three actually have released new content since then. And so, I think even though the article has a quite clickbait title, the content and the reasoning in this article was misleading. I think this article was able to start a heated debate. It’s proof that people are paying attention to be Bilibili very closely, and some media even went down to write derivative reports on this article. And that’s why we — and that discussion ended on the hot topic list of Weibo. And internally, we have been making a lot of efforts to improve commercialization for content creators at Bilibili and we have numbers to back that up.

Valuation/Pricing

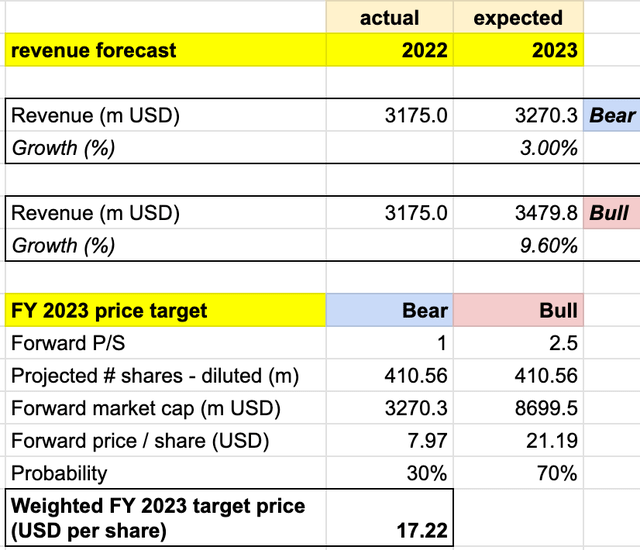

For FY 2023, the management guided to revenue of RMB 24 billion – RMB 26 billion ($3.37 billion – $3.65 million). To estimate the target price for BILI in FY 2023, I assume the following bull vs bear scenario:

- Bull scenario (70%) – BILI to finish FY 2023 with $3.37 million of revenue (~9.6% YoY growth), at the lower end of its guidance, considering the management’s relatively aggressive expectation for the mobile gaming business. I assume that BILI will see a -20% decline in the IP derivative business, but will see a +20% growth in the advertising business, ~15% growth in the VAS business, and single-digit growth of 5% in the mobile gaming business. Furthermore, I expect the gross margin to expand to ~20% and the operating loss to narrow.

- Bear scenario (30%) – BILI to miss the FY 2023 estimate and end the year with RMB 22.5 billion ($3.16 billion) of revenue, which is a ~3% YoY growth. I assume that BILI will see a -25% decline in the IP derivative business, +15% growth in the advertising business, 5% growth in the VAS business, and single-digit growth of 5% in the mobile gaming business. Furthermore, I expect the gross margin to expand slightly, though operating margin remains at the same level as FY 2022’s.

I assign a P/S of 2.5x for BILI under the bull scenario, the level last seen between late last year and early this year when gross margin saw an expansion. Over the same period, growth had also been decelerating to end up at ~13% YoY in FY 2022, with P/S between 1.6x – 3.3x. As such, the outlook appears to be quite similar to the current expectation for FY 2023. The 2.5x P/S for the bull scenario reflects the midpoint of that range. Furthermore, I conservatively assign a P/S of 1x for the bear scenario, which is an all-time low P/S for BILI last seen in October 2022.

author’s own analysis

I also assume that BILI will not do any further ADS / American depositary share repurchase, and will end up with ~410 million of ADS on a diluted basis at the end of FY 2023. Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of $17.22 per share. At ~$14.97 per share today, the target price reflects a 15% upside potential.

Conclusion

BILI is a promising business poised to benefit from China’s video-based industry growth, with a strong focus on Gen Z. I expect revenue growth to slow down further from ~13% in FY 2022 to ~9.6% YoY in FY 2023 as the management aims to bring the company closer to its breakeven goal in 2024.

There are some moderate risk factors on the stock, though as I account for the catalysts for growth and margin expansion in FY 2023, I give BILI an overweight rating. Currently trading at ~$15, my FY 2023 target price suggests a 15% upside.

Read the full article here