The Intro

Deckers Outdoor Corporation (NYSE:DECK) is a company that specializes in footwear, apparel, and accessories for both casual and high-performance purposes. It offers a range of products under various brand names, including UGG, Teva, Hoka, among others. The company sells its products through various channels, such as department stores, specialty retailers, and its own retail stores and e-commerce websites.

With its headquarters in Goleta, California, Deckers Outdoor Corporation was founded in 1973 and operates globally, with a significant presence in the United States, Europe, Asia-Pacific, Canada, and Latin America. As of March 31, 2022, the company had a total of 149 retail stores worldwide.

In this article, we will conduct a thorough assessment of DECK’s financial performance and growth prospects. Our evaluation will include an in-depth analysis of the company’s revenue and profitability trends, its ability to generate free cash flow, and the overall financial stability reflected in its balance sheet. Additionally, we will employ a discounted cash flow analysis to estimate the intrinsic value of DECK, providing valuable insights for investors who are considering DECK as a potential investment opportunity in the current market.

For The Record

DECK has shown consistent growth in both revenue and free cash flow over the last ten years while maintaining a strong return on equity (ROE). Let’s further analyze the company’s financial performance and evaluate its potential as an investment opportunity.

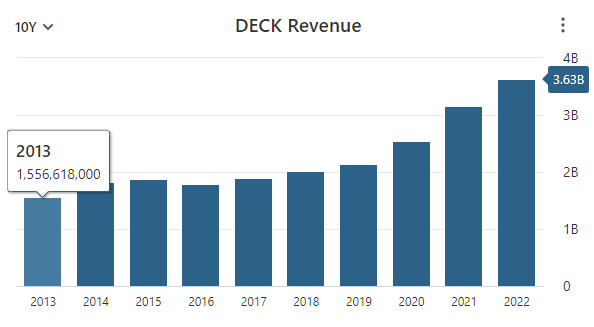

DECK has demonstrated remarkable revenue growth over the past decade, with no decline in revenue since 2016. From 2013 to last year, the company’s revenue increased from $1.55 billion to $3.63 billion, highlighting its ability to expand operations and gain market share. Furthermore, DECK has achieved revenue growth every year except one during this period.

Data by Stock Analysis

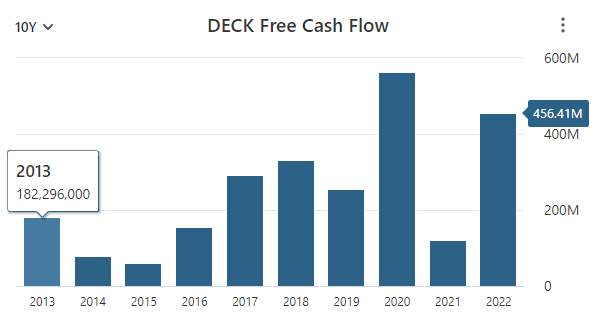

Another important metric to consider is free cash flow, which represents the cash generated by the business that can be utilized for investments, acquisitions, or dividends. DECK’s free cash flow has increased substantially over the past decade from $182 million to $456 million in 2022. These free cash flow results indicate the company’s ability to generate significant cash flows from its operations.

Data by Stock Analysis

Moving on to profitability, return on equity (ROE) is a critical measure for assessing a company’s performance. DECK has maintained an average ROE of 20.66% over the past ten years. A high ROE suggests that the company effectively utilizes its resources to generate profits for shareholders. It is important to compare a company’s ROE against its peers to gauge its performance. DECK’s current ROE of 31.28% surpasses the sector median of 10.18%, indicating that the company is significantly more profitable than its competitors.

Now let’s examine DECK’s balance sheet and evaluate its overall health. The company’s current debt-to-equity ratio is just 0.14 which is a good sign to investors indicating that the company has a conservative financial approach and sound management of capital. Additionally, DECK’s current ratio of 3.84 suggests that it can meet its short-term obligations, such as bills and operational expenses, with a significant margin of safety if something unforeseen should materialize. As an investor, I feel great about this DECK’s financial position, its strong balance sheet indicates that the business is healthy and financial stability, with sufficient assets to cover its liabilities, which can provide a strong foundation for growth and weather economic downturns.

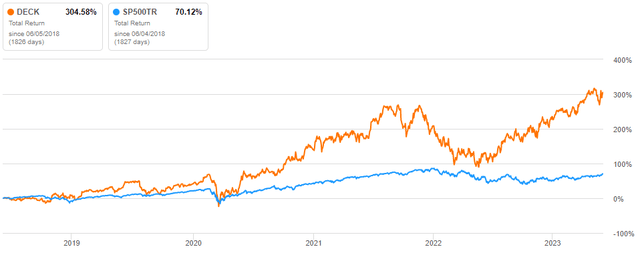

DECK’s strong financial effectiveness has powered its stock to outperform the total return of the S&P 500 over the past five years. While the S&P 500 achieved a total return of 70.1% over the last five years, DECK trounced these results by delivering a total return of 304.6% over the same period. Long-term shareholders of DECK have been delighted by these results but the question on everyone’s mind is whether DECK can continue to outperform the broader market.

Data by Seeking Alpha

What’s Next?

DECK’s outlook appears promising for the next few years, as analysts predict strong earnings growth. It is projected that the company will experience robust earnings of $21.94 per share in 2024 which represents a significant 13.26% gain year over year. The earnings growth is expected to continue in 2025 and beyond with analyst estimating $25.66 per share in 2025, $30.54 in 2026, and $32.21 in 2027, indicating a potential future of substantial growth. While predicting future earnings, especially for a company several years ahead, is challenging and subject to uncertainty, these projections indicate a positive trajectory for DECK based on its current earnings performance.

Data by Seeking Alpha

Moreover, analysts are optimistic about DECK’s future revenue, projecting significant growth ahead. The company is estimated to experience robust near-double-digit revenue growth in 2024, reaching $3.99 billion, and further increasing to $5.30 billion by 2027. These encouraging projections come on the heels of DECK surpassing its latest earnings expectations. During the most recent quarter, the company reported earnings of $3.46 per share, exceeding expectations by an impressive $0.76. Additionally, DECK generated $791 million in revenue, surpassing expectations by $68.1 million and representing a year-over-year growth rate of 7.6%. This positive performance demonstrates DECK’s ability to outperform market expectations and signals its potential for continued success in the future.

One of the main reasons why analysts are so bullish on DECK is the strong performance of its standout athletic shoe brand, HOKA. In 2023, the HOKA brought in $1.4 billion in sales globally which increased 58% year over year. This stellar growth was not an anomaly, it’s the fourth consecutive year HOKA has grown by more than 50%.

HOKA’s growth for the year was fueled by multiple factors, including a significant surge of over 30% in global brand awareness during the fall of 2022. This growth in brand awareness can be attributed to the company’s first global marketing campaign for HOKA, called “Fly Human Fly.” The company leveraged connected TV, digital platforms, and out-of-home channels to effectively engage a wider audience by combining emotionally resonant brand messaging with compelling product communication. The investments made in this campaign yielded notable outcomes, as HOKA’s awareness witnessed substantial growth across key markets including the U.S., France, the UK, China, and Germany.

Looking ahead the DECK see’s further opportunities to grow HOKA’s brand with kids which will also spread brand awareness with their parents. Additionally, the company plans to invest in updated “Fly Human Fly” campaign to help boost sales. DECK’s President and Chief Executive Officer David Powers touched on this imitative during the company’s latest earnings call.

We are working to close the awareness gap between the U.S. and international regions to build a more global brand. The HOKA marketing team has done a fantastic job developing insights from the initial campaign to evolve the next iteration of Fly Human Fly, which will focus on the brand’s roots and performance through inclusive storytelling that emphasizes the joy of movement for everybody. Stay tuned for more details on the campaign when it launches next month.

Furthermore, DECK is committed to further expanding the reach of their HOKA brand by making calculated and strategic choices in wholesale distribution, aiming to tap into a broader and more diverse consumer base. They also plan to diversify the HOKA brand’s offerings by venturing into lifestyle, trail, and hiking segments, providing customers with authentic performance footwear choices that cater to their varied preferences and needs.

Name The Price

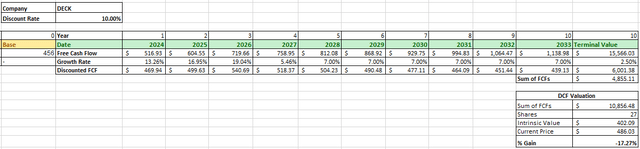

We will utilize the discounted cash flow (DCF) analysis, which is my preferred valuation method, to evaluate DECK’s intrinsic value. The DCF analysis assesses a company’s inherent worth by calculating the present value of its expected future cash flows.

To initiate the analysis, we will begin with DECK’s previous year’s free cash flow of $456 million. For 2024, we will use the average analyst earnings growth rate of 13.26%. Subsequently, based on the average analyst earnings estimates, we will utilize growth rates of 16.95%, 19.04%, and 5.46% for the following three years. However, predicting DECK’s free cash flows beyond this point becomes increasingly challenging. Therefore, we will adopt a growth rate of 7% for the next five years, taking into account the company’s strong historical growth.

To calculate the terminal value, we will apply a more conservative perpetual growth rate of 2.5%. Employing a discount rate of 10%, which considers the S&P 500’s long-term return rate with dividends reinvested, DECK’s intrinsic value is determined to be $402.09. This suggests that DECK may currently be overvalued, indicating a potential loss of 17.27% for investors compared to the company’s current market price.

Author’s Work

Final Word

DECK has demonstrated consistent growth in revenue and free cash flow over the past decade, indicating its ability to expand operations and generate significant cash flows. The company’s strong return on equity (ROE) surpasses the sector median, showcasing its profitability and effective resource utilization. DECK’s financial stability, reflected in its conservative debt-to-equity ratio and current ratio, provides a solid foundation for growth and resilience against economic downturns. The stock has outperformed the S&P 500 over the past five years, delivering impressive returns to long-term shareholders.

Analysts project strong earnings and revenue growth for DECK, driven by the standout performance of its athletic shoe brand, HOKA. HOKA’s remarkable sales growth, fueled by increased brand awareness and effective marketing campaigns, has positioned it as a key driver of future success for DECK. The company plans to further expand HOKA’s brand by targeting the kids’ segment and investing in updated marketing campaigns. Additionally, DECK aims to broaden the reach of HOKA through strategic wholesale distribution and category extensions in lifestyle, trail, and hiking segments.

Considering DECK’s substantial growth opportunities with the HOKA brand and the current high price of the stock, a decision to hold the stock seems appropriate. While the stock may be currently overvalued based on the discounted cash flow analysis, the potential for future growth and the company’s strong performance makes it an attractive long-term investment.

Read the full article here