Investment Thesis

Principal Financial Group, Inc. (NASDAQ:PFG) is one of the leading American financial services groups. The company has a diverse portfolio in diverse geographical locations. Besides helping it mitigate risks, it helps grow its client base by reaching different target markets with different offerings. Some of its products and services include insurance, retirement solutions, wellness programs, and investment and banking products.

I believe this diversity and its new approach to having an integrated business model will be key drivers to its financial success in the long term. With these strong fundamentals and a management commitment to its shareholders, as exhibited by the share buybacks and consistent dividend payments, I believe PFG is a compelling investment opportunity. However, the company trades almost at its fair value, attracting a hold rating for value-oriented investors.

Financials Stability

A financially stable company, in my view, will always be the ideal option for any potential investor as it, to some extent, dictates the safety of their investment. It is for this reason that I examine the financial stability of PFG.

Over the last three quarters, its total operating expenses average at about $3B, while the company’s current cash position of $5.53B can cover the average total operating expenses at 1.8x. In other words, the company has enough cash to cover its operating expenses for the next two quarters. Further, with a current ratio of 1.43x, PFG can adequately cover its short-term liabilities.

With a total debt of $5.13, it is 0.3x its market cap of $16.26, which makes me consider the company deleveraged, minimizing debt-related challenges. To make it even more attractive, the current cash position can pay off the entire outstanding debt of the company without depletion. In my view, I believe this is a very assuring liquidity position which is backed by a strong cash flow from operation [TTM] of $3.84B and a levered free cash flow of $328.38M. In my opinion, the strong cash flow from operations expresses the company’s strong ability to generate cash and therefore also helps speak volumes on the company’s solid financial status.

Considering this evaluation, I find this company’s financial status very stable. I believe it can leverage its strong financial footing to exploit any opportunity in the market and weather economic storms.

Diversity and Integrated Business Model

1. Diversity

As mentioned earlier, this company offers a wide range of diverse products and services, including but not limited to; pension risk transfer services, individual variable annuities, retirement, related financial products and services, bank products, and trust and custody services. Besides diversifying its offering, the company has also diversified its geographical reach and offers its products and service in a number of states such as the US, China, Brazil, Mexico, Chile, Hong Kong Special Administrative Region, and Southeast Asia

This diversity has been critical in ensuring the company’s success, as shown by the numbers in the MRQ. The company generated an international net cash flow of $800 million in the first quarter of 2023.

CEO Daniel Houston stated,

We also drove strong quarterly net cash flow of $800 million in Principal International. These flows were well diversified across Southeast Asia, Brazil, Mexico and Hong Kong as we continue to execute on our strategy, building upon our market leadership and key joint venture relationships. Specific to Brazil, we remain a market leader in pension AUM, deposits as well as net cash flow. Bottom line, we are very excited about the growth opportunities which lie ahead. I’m confident we have the right product mix, the right market focus and the right distribution channels to drive value for our customers and our shareholders.

I believe these sentiments from the CEO are a testament to how diversification is key to the company’s success and also believe that this strategy will be a long-term growth driver that this company should leverage.

2. Integrated Business Model

In a bid to efficiently provide local and global investing capabilities and client assistance across more than 80 markets, generating greater benefits for customers and shareholders, PFG integrated its global asset management and international pension businesses. Principal’s expansion has largely been fueled by its global asset management services.

Its regional distribution and customer engagement strategy will help the company better understand local markets and tailor its product offering to meet the needs of a growing number of niche customers. Under the new organizational framework, regional teams in Asia, the Middle East, the Americas, and Latin America will work together to serve a wider variety of clients better and provide a wider choice of investment, retirement, and pension options. Principal will maintain its strong leadership in local markets through its country heads, who will oversee the company’s interactions with its most important customers, government officials, and business partners.

The company has already started reaping the fruits of this new business model. In Q1 2023, the CEO seemed to appreciate how this integrated model has helped them overcome economic headwinds. Below are his remarks on the same.

Our integrated business model remains resilient during periods of macroeconomic volatility, as shown on our strong first quarter results. While we are not immune to credit and market pressures, we are well positioned for a variety of economic conditions.

In terms of concrete benefits, consider that the firm had $660 billion in total AUM managed by the firm as of the end of the first quarter of 2023, an increase of 4% from the end of 2022. They also had a positive net cash flow of $600 million for the company, an impressive figure considering the industry was experiencing outflows. They credit the success to their diversified and integrated business model, which I agree with and am confident, will continue to yield positive outcomes.

Earnings And Dividends: My Investment Case

Typically, dividends are paid from a company’s earnings. If a company pays out more dividends than it earns in profit, the dividend may not be sustainable. Principal Financial Group’s payout ratio is approximately 39%, which is fairly low and conservative.

Another evaluation criterion is whether the company’s earnings and dividends have been growing. Companies whose earnings per share keep going up are usually the best dividend stocks because it’s usually easier for them to keep increasing their payouts per share. If the company doesn’t make enough money, it might have to cut its dividends.

Fortunately, PFG EPS has had a 3-5 year CAGR of 8.75%. Most investors will look at the historical dividend growth rate when evaluating a company’s dividend prospects. The dividend increase rate for Principal Financial Group over the previous ten years has been about 12% annually on average. It’s encouraging to note how earnings and dividends per share have increased significantly in recent years.

Given these statistics, I form my investment case of whether PFG is a good investment. When firms grow quickly and keep most of their profits, it’s generally a sign that reinvesting profits creates more value than giving dividends to shareholders. Perhaps even more importantly, this can sometimes indicate that management is focused on the company’s long-term future. This analysis demonstrates that this company appears to be a dividend stock with potential, and I believe it is worth investing in it.

Valuation

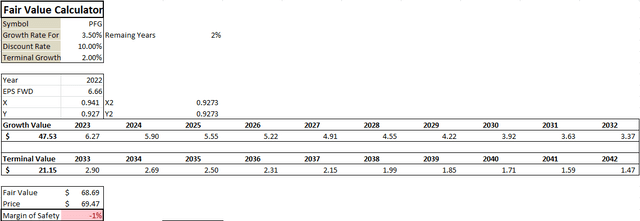

Looking at the overall valuation grade B- assigned to this company by Seeking Alpha, it appears that this company is almost trading near its fair value. With that in mind, I ran an EPS-based DCF model to determine the company’s fair value. Below are the assumptions and the output of the model.

Author’s Computation

Looking at the output of my model, I estimated a fair value of $68.69, slightly lower than the current share price. Given this data, it is apparent that this company is trading near its fair value. Therefore, value-oriented investors can hold until the stock offers a good value according to their targeted profits.

Risks

Like any other investment, Principal Financial carries risks. One of the most significant risks is the competitive environment. Principal Financial operates in a highly competitive market, and the company faces fierce competition from established players and new entrants. The company needs to be continually innovative and respond to market trends to maintain its competitive position.

Another risk to take note of is regulatory risk. Financial institutions have come under much scrutiny and pressure in recent years following a series of scandals and mishaps in the industry. Regulatory changes such as interest rate adjustments, new reporting requirements, or changing tax laws can significantly affect the company’s operations and profitability.

Finally, market risks could lead to a decline in the company’s stock price, including fluctuations in interest rates, foreign exchange rates, and inflation.

Bottom Line

Generally, PFG is a compelling investment given its brilliant business model and good earnings and dividend trends. I think the company is a buy for dividend-oriented investors, but I rate it a hold for value investors.

Read the full article here