CAE Inc. (NYSE:CAE) reported its FY2023 earnings on the 31st of May and its adjusted EPS for the quarter was ahead of expectations. As a provider of simulators, modeling technologies, and training services to airlines, aircraft manufacturers, defense customers, and healthcare specialists, I believe that CAE Inc. is positioned extremely well to play a meaningful role in supporting the increasing demand for air travel and pilot training.

In this report, I will be having a look at the results for CAE Inc., the outlook, and provide a price target for the stock.

Amounts mentioned in this report are in Canadian dollars, unless mentioned otherwise.

CAE Stock: Civil Aviation Strength Propels Earnings Growth

CAE Inc.

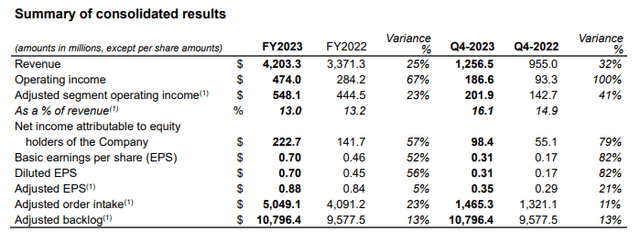

I could focus on the quarterly figures. However, I am somewhat more interested in the longer-term trajectory and not so much in any year-over-year fluctuations in quarterly numbers. Revenues were up 25% beating the $4.16 billion that analysts were expecting. So, we see a strong topline growth number that exceeded market expectations.

The Civil Aviation Segment booked a 34% increase in sales, while defense sales were up 15% and healthcare sales were up 27%. From an earnings perspective, the operating income growth of 67% or 23% was also driven by Civil Aviation, which saw a 92% jump in income as utilization of flight simulators grew 12 percentage points to 72% and the number of simulator deliveries to customers and inside the network of CAE Inc. grew. So, CAE Inc. without a doubt is benefiting from increased pilot hiring and I wouldn’t really expect that to significantly slow down as I believe that airlines are more than ever aware that it requires a continued effort to keep pilot shortages manageable over the longer run. Furthermore, the company had some benefits on timing of revenue recognition for already delivered simulators. The Civil Aviation adjusted backlog grew 16.5% to $5.7 billion.

Defense tends to be the stable factor in the earnings of many companies, but that wasn’t visible in the operating income of the defense segment, which was 36% and 55% lower on an adjusted basis caused by negative contract adjustments on two US Defense programs in the first quarter this year and higher costs as the company aims to increase its Defense footprint. The adjusted backlog stands at $5.1 billion, up 9% year-over-year.

The Healthcare segment saw its operating income increase to $8 million from $3.9 million driven by a favorable mix and lower restructuring and integration costs, but on an adjusted basis, the earnings were 8% lower reflecting higher net R&D costs.

So, the business booked revenue growth in all segments, but its adjusted earnings show that the Civil Aviation segment provided the earnings growth. That is not a huge surprise, but one could be hoping to have seen some more stability in the other segments.

The Outlook For CAE

CAE aims to grow its EPS between FY22 and FY25 by a compound growth rate of mid-20% supported by continued strength in the Civil Aviation segment, a transformation in Defense, and a larger scale of Healthcare. Civil Aviation is expected to grow above market rate as the recovery in air travel in Asia continues, while Defense supply chain issues are expected to ease to some degree. Unfortunately, there were no target numbers presented, but the mindset and strategy should position the company for growth.

Is CAE Stock A Buy?

The Aerospace Forum

I have little doubt that CAE is a buy. The company is a market leader for simulators and training services, and demand for those services will not decline in the foreseeable future. I recently launched a stock valuation for subscribers of The Aerospace Forum and I put the numbers for CAE in that tool and the tool essentially shows that based on its FY2023 earnings, the company is undervalued by around 12.5% and projecting roughly 12 months forward, the stock should have another 33% upside based on industry median enterprise to EBITDA multiples.

Conclusion: CAE Is A Simulator Market Leader With Upside

CAE’s results were somewhat mixed for FY2023. All segments saw topline growth, but only Civil Aviation saw appreciable income growth. Defense and Healthcare are where CAE wants to scale up and get healthier contracts and a process that will unfold, so projecting forward is not useful there. The company is working diligently on better utilizing its strengths and capacities to serve all segments efficiently, and that should result in value creation for shareholders.

Read the full article here