With the war in Ukraine, defense names have been in the spotlights for well over a year now, but realistically, not all names are attractive. Some defense stocks even got ahead of themselves and corrected accordingly. Next to that, while the defense equipment deployed in Ukraine has a broad base, there are some platform types that seem to be somewhat higher in demand than others.

The Battlefield In Ukraine

In the early days of the invasion, the focus was primarily on defensive weapons such as the NLAW, which stands for Next-generation Light Anti-tank Weapon. As the war progressed, we saw a rather quick deployment of the Bayraktar drones to counter the Russian advance, while Russia utilized Iranian-built killer drones. From there, the deployment evolved in with more advanced air and missile defense systems such as the Patriot and advanced main battle tanks such as the Leopard A2, the Challenger and the M1 Abrams planned for later this year. Ukraine, in the meantime, has continuously requested F-16 fighter jets and in recent days, there seems to have been more willingness to provide training and eventually fighters to Ukraine.

Nevertheless, the importance of drones in this war is clear, and that makes UAV specialists interesting for investment research. I previously looked into Kratos and found that while it specializes in various drones and unmanned platforms, it is an expensive stock, while General Atomics, which produces the MQ Reaper drones that have been offered to Ukraine is not a public company, which brings us to AeroVironment (NASDAQ:AVAV).

AeroVironment: The Small UAV Specialist

AeroVironment

AeroVironment, Inc. designs, develops, produces, delivers and supports a technologically-advanced portfolio of intelligent, multi-domain robotic systems and related services for government agencies and businesses. The Small Unmanned Aircraft Systems segment is focused primarily on products designed to operate reliably at very low altitudes in a range of environmental conditions. The Tactical Missile Systems segment focuses primarily on tube-launched aircraft that deploy with the push of a button. The Medium Unmanned Aircraft Systems focuses on designs, engineers, tools, and manufacturing of unmanned aerial and aircraft systems, including airborne platforms, payloads and payload integration, ground control systems, and ground support equipment. This segment also integrates flight autonomy solutions. The High Altitude Pseudo-Satellite Unmanned Aircraft Systems segment consists of the Company’s existing development of High Altitude Pseudo-Satellite systems in conjunction with SoftBank.

The drone solutions for Ukraine are actually quite simple: The Puma 3 AE can be used to identify threats, after which Switchblade 600 kamikaze drones can be deployed to neutralize the threat. Next to that, the unmanned ground vehicles could also be of interest in Ukraine. With the focus seemingly shifting towards fighter jets, I don’t expect a slowdown in drone deliveries to Ukraine. F-16 training normally takes nine months, so in those nine months, pilots need to be trained, and ideally fighter jets are sent to Ukraine. It seems that in four to six months, the training can be completed, meaning that training time is slashed in half.

Even if today the training starts, which is not the case, the first F-16 actions in Ukraine are not expected until next year on the normal timeline and late 2023 if the shortened timeline is adopted with training commencing imminently. Deploying the F-16s to Ukraine is going to be highly complex, as the F-16s are completely different compared to the MiG-29s Ukraine is familiar with and beyond that you need an entire logistics chain to be able to effectively deploy the F-16s and you are realistically looking at 2024 before we see those fighter jets in action. Until then, the UAVs play an important role and even beyond the nine months mark, the small UAV solutions likely will remain critical due to easy deployability and usability next to the F-16s.

AeroVironment Sees A Surge In Results

AeroVironment

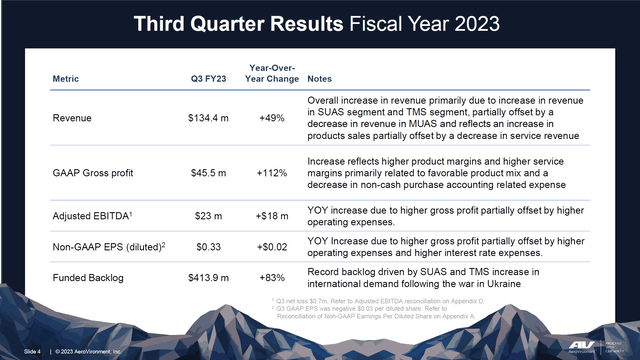

For many advanced defense platforms, we are seeing sales opportunities into 2024. AeroVironment is positioned rather well in that regard. Its product are relatively easy to operate and meaningful on the battlefield, and that puts them in front of the line of companies that are seeing a faster translation from backlog to topline. Revenues grew 49 percent, while gross profit more than doubled and adjusted EBITDA grew $18 million, with backlog surging 83%. Those are stellar numbers, and I believe we are just at the beginning of expanding defense budgets translating to orders and sales for small and medium-sized unmanned aerial vehicles. Interesting to note is that while many companies have services margins exceeding the product margins, for AeroVironment, this is the other way around, and it benefited them in the most recent quarter.

AeroVironment

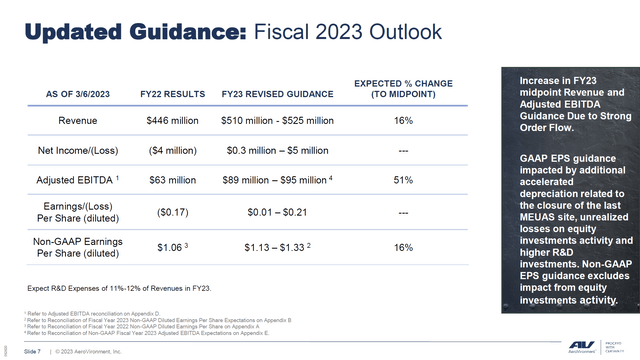

The company has also increased its revenue and EBITDA guide and is now targeting 16% revenue growth and 51% growth in adjusted EBITDA, leading to 16% growth in core earnings per share. All of that is based on appreciable mix and strong order inflow.

Is AeroVironment Stock A Buy?

The Aerospace Forum by evoX

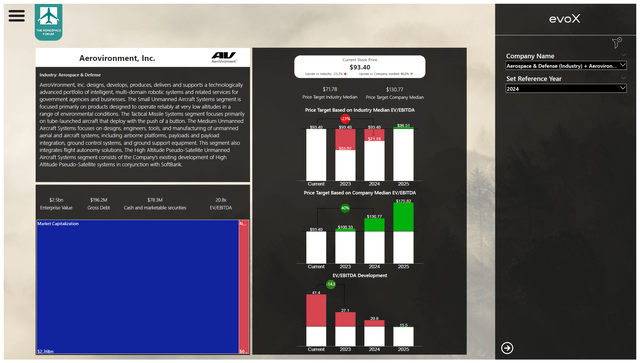

At the time of writing, AeroVironment stock is down nearly 14% as it has been eliminated from the FTUAS (Future Tactical Unmanned Aerial System) program. I think this comes as a surprise to the market as well as AeroVironment as it previously was confident in the Jump 20 that it entered into the competition highlighting that it was the only company selected for all three phases of FTUAS, and it now has been the only company out of five not being selected to compete for the RQ-7B replacement. I entered the expected numbers for AeroVironment into the model I have developed for The Aerospace Forum and will soon be launched for subscribers. We actually see something similar as we saw with Kratos, and that is what seems to be a premium for UAV specialists. That would provide 40% upside with the next financial year earnings in mind. Valuing it in line with the industry, however, provides little upside. For FY2024, I see upside to $130, which is in line with the most bullish Wall Street price target, but with the FTUAS elimination, there are some doubts on sustained growth and value creation.

Conclusion: FTUAS Elimination News Puts Sustained Growth Into Question

At this point, while 40% upside would seemingly be more than enough for a buy rating, I am sticking to hold. The reason is that with the elimination from FTUAS, we really have to see what the ingredients are going to be for sustained revenue growth. Currently, we do see sales driven by UAS demand in Ukraine and I expect that to remain strong, but the big question is how revenue growth can compound beyond that from sustained demand. Demand is there, but the question is really whether that will be enough to offset the significant growth we are seeing currently. AeroVironment is not an ugly name to buy, but I do believe the risks make it a more attractive hold.

Read the full article here