Rocket Lab (NASDAQ:RKLB) has made notable advancements in the space industry, showcasing its technological capabilities over the past year. With over 40 successful satellite deployments in 2022, the company demonstrated its precision and reliability in delivering payloads to specific orbits.

Beyond Earth’s orbit, Rocket Lab achieved success with the CAPSTONE mission for NASA, effectively delivering the payload to the moon. This achievement was made possible through the Luna Photon, an interplanetary spacecraft developed and constructed by Rocket Lab. The company’s innovative approach included the development of an efficient lunar trajectory, allowing smaller rockets to transport payloads to lunar orbit.

The previous two paragraphs highlight the fact that Rocket Lab’s main focus is to offer reliable and cost-effective launch services for the growing small satellite market. Let’s dissect their main programs and evaluate whether it is a plausible investment option.

Neutron Program

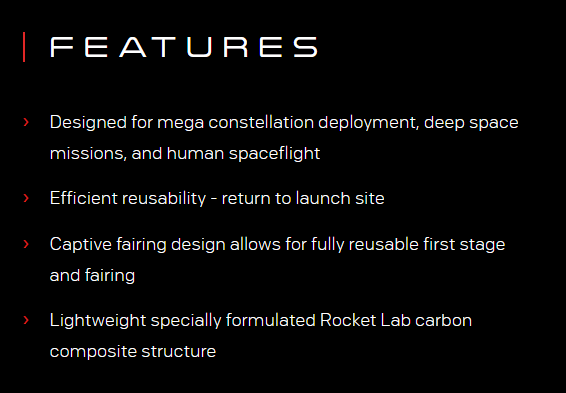

The Neutron program is Rocket Lab’s next-generation launch vehicle, designed to provide reliable and cost-effective launch services for satellite mega-constellations, deep space missions, and human spaceflight.

Rocket Lab

The Neutron rocket will be the world’s first carbon composite large launch vehicle. Rocket Lab’s previous experience with carbon composite structures in the Electron rocket has demonstrated the benefits of this material, such as its lightweight yet strong properties. The carbon composite structure enables the Neutron rocket to withstand the extreme heat and forces of launch and re-entry, allowing for frequent re-flight of the first stage.

The unique tapered shape with a wide base, provides a robust and stable platform for landing that eliminates the need for complex landing mechanisms and legs, simplifying the rocket’s structure. Additionally, the Neutron rocket can stand securely on its own legs for lift-off. After deploying the second stage, the first stage returns to Earth for a propulsive landing at the launch site, reducing costs associated with ocean-based landing platforms.

The Neutron rocket will be powered by the Archimedes engine, an entirely new rocket engine developed in-house by Rocket Lab. This reusable liquid oxygen/methane gas generator cycle engine provides 1 meganewton thrust and 320 seconds of ISP. The lightweight carbon composite structure of the Neutron rocket allows for a simpler engine design with modest performance requirements, accelerating development and testing timelines. The company is leveraging advanced additive manufacturing techniques to develop these engines, an innovative approach that can enhance production efficiency and accuracy.

The unique ‘Hungry Hippo’ fairing design eliminates the need for costly fairing capture at sea, speeds up launch frequency, and enables a lightweight and nimble second stage.

What sets Neutron apart is its focus on reusability, which has the potential to drive down launch costs, improve sustainability, and increase launch frequency. The program has already achieved notable development milestones, including a significant payment milestone from the US Space Force as part of a $24 million contract to develop Neutron’s upper stage.

Electron Program

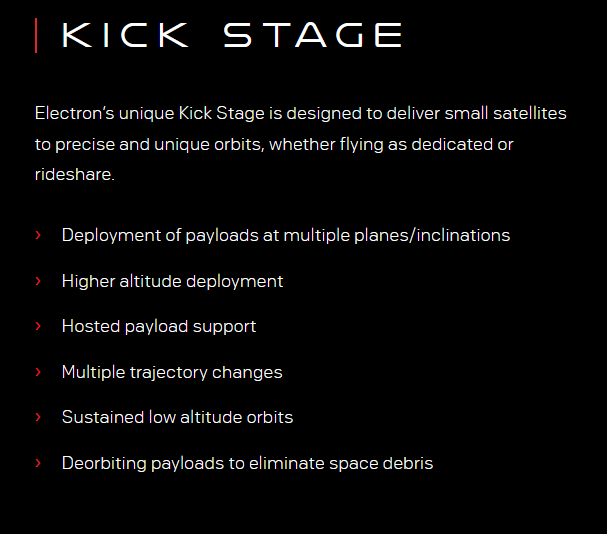

The Electron program centers around the Electron rocket, which is specifically designed to launch small satellites.

Rocket Lab

The Electron rocket is also built with a carbon composite structure, making it lightweight and strong. This design choice allows for increased payload capacity. The rocket is powered by Rocket Lab’s Rutherford engine, which utilizes LOX/RP-1 as fuels. As we have seen, the engine incorporates innovative technologies, such as electric propulsion cycles and 3D-printed primary components.

Rocket Lab employs a containerized approach to simplify payload processing, where customers encapsulate their satellites in payload fairings provided by the company. This streamlined integration process enables the fairings to be easily attached to the rocket shortly before launch. In addition, Rocket Lab offers a unique pricing model for Electron launches, selling the entire launch vehicle instead of charging based on payload weight. This approach provides customers with a simplified cost structure and greater flexibility in payload selection.

One significant advancement for Rocket Lab is the potential reuse of its Rutherford engines, which power the Electron rocket. Extensive hot fire tests on recovered engines have demonstrated their durability. This indicates the possibility of significant engine reuse, which can lead to substantial cost reductions and enhanced competitiveness for Rocket Lab.

On the manufacturing front, Rocket Lab has optimized its production process, resulting in increased efficiency in building Electron rockets and reduced lead times. This optimization has allowed the company to allocate production resources to support their Neutron and Photon R&D initiatives. While this has led to a decrease in production headcount, the overall total headcount has increased, which might not be as positive as it seemed.

Financials Valuation and Risks

While Rocket Lab has promising programs and innovative strategies such as additive manufacturing for engines, carbon composite structures, and vertical integration, the key question remains whether they can build a profitable business.

Analyzing the company’s financials, there is significant room for margin improvement, particularly in the launch segment. The cadence dynamic, driven by overhead absorption and the number of launches per quarter, presents the largest area for upside. Furthermore, the recovery of the first-stage booster has the potential to significantly increase margins.

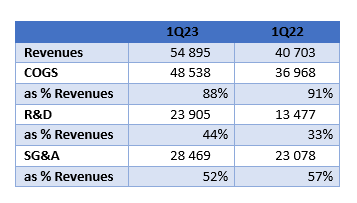

The results for 1Q 2023 provide slightly encouraging signals. Cost of goods sold (COGS) and selling, general, and administrative expenses (SG&A) are declining relative to revenues as sales grow. However, research and development (R&D) costs are the only expense item increasing, which may indicate a justified allocation or potential hidden concerns. Close monitoring is necessary to assess the situation accurately.

Author’s Computations

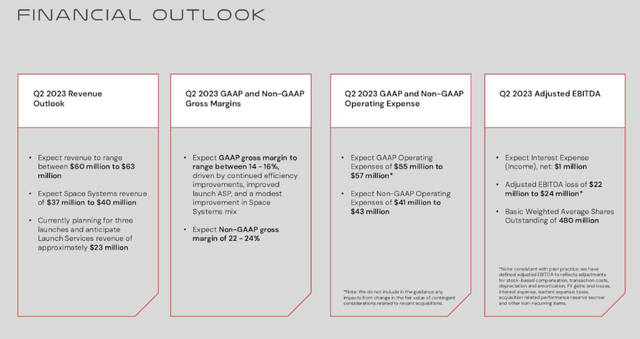

Moving forward to Q2 2023, Rocket Lab is expecting revenue between $60 million and $63 million. The projected gross margin for the quarter is estimated to be between 14% and 16% for GAAP and 22% to 24% for non-GAAP. Operating expenses are anticipated to range between $55 million and $57 million for GAAP and $41 million and $43 million for non-GAAP. The adjusted EBITDA loss is expected to be between $22 million and $24 million, with approximately 480 million basic shares outstanding. If these projections materialize, it would support the ongoing trend of improved cost dilution, which is positive.

Rocket Lab

Examining the balance sheet, the company currently experiences significant cash burn, estimated at around $100 million per year and growing compared to the previous year. Despite this, Rocket Lab has a current ratio above 3 and minimal debt, which suggests the ability to sustain this burn rate for an extended period. However, the cash burn is not linear, and periodic spikes make predictions challenging. Maintaining sufficient cash levels remains critical, potentially leading to further share dilution.

In my opinion, it is premature to assign a proper valuation to the company. There are still doubts surrounding their ability to achieve the necessary margin improvements for long-term success. Additionally, the heavy reliance on experimental technologies like 3D printing poses a significant risk to the company’s long-term prospects.

If Rocket Lab can achieve consistent revenue growth of around 20% annually, demonstrate the effectiveness of its technological approach, execute on margins, and maintain a healthy balance sheet, it could potentially reach $350 million in revenues by 2025, with a valuation around $3.5 billion compared to the current $2.4 billion.

Overall, considering the mentioned dilution risk, the upside appears limited. Therefore, for now, I will remain on the sidelines but closely monitor the company due to its promising technology and strategic direction.

Read the full article here