A cooling environment for home improvement, as reflected last week in Home Depot’s (HD) results provided investors with a preview into what earnings could potentially look like for Lowe’s (NYSE:LOW).

Heading in, the two stocks performed largely in-line with each other over the past one month.

Seeking Alpha – 1-Mth Returns Of LOW Compared To HD

But LOW has maintained a sizeable performance gap over the past year.

Seeking Alpha – 1-YR Returns Of LOW Compared To HD

Despite the outperformance, LOW still trades at a discount to HD, with a forward multiple of 15x compared to the 19x commanded by their counterpart. Recent results missed expectations for comparable sales but less so than HD. In addition, though guidance was revised lower, the company is still likely to benefit over the long-term due to favorable demand drivers, such as an aging housing stock, elevated home equity levels, and increased household formation.

What Did LOW Expect Heading Into Their Earnings Release?

Though the long-term outlook for home improvement was viewed favorably at the end of fiscal 2022, CFO, Brandon Sink, did note on their Q4FY22 earnings release that residential investment would be under pressure in 2023, given the state of the overall macroeconomic environment.

With that in mind, total sales were forecasted to land between +$88B and +$90B for the full fiscal year. That would have been down from the +$97.1B generated in fiscal 2022. In addition, comparable sales were seen to be flat or down 2%.

Through 2022, LOW experienced continued strength in sales to their Pro customers. Q4, for example, marked their 11th consecutive quarter that they generated double-digit Pro growth in the U.S. And looking ahead to 2023, expectations are that Pro sales growth will continue to exceed growth in DIY.

On the expense side, the company expected to spend +$350M in incremental wages for their frontline associates. But despite the expected growth, operating margins were still expected to track in-line with 2022 levels, at between 13.6% to 13.8%, due in part to their productivity initiatives.

All considered, full-year EPS was expected to range between $13.60/share and $14.00/share. With lower lumber prices in mind, management did expect Q1 sales to be below their full-year guidance. This, however, was expected to be offset by stronger sales in the second quarter.

Did LOW Meet Expectations?

Leading up to their release, LOW was viewed favorably by several analysts. Jefferies, for example, inputted a $250/share price target on the stock and noted that company initiatives were set to deliver flat YOY comps, resulting in a forward view on EPS that would have been ahead of consensus estimates. In addition, favorable tailwinds resulting from the weather were cited as one catalyst by Wells Fargo.

The stock has also been outperforming its peer, HD, over the past year, but both stocks have been trailing the broader overall markets, which are positive for the year.

In the first fiscal quarter of the year, reported revenues were down 5.5% YOY but above expectations by +$670M. Non-GAAP EPS of $3.67/share also beat by $0.02/share.

Despite the beat on surface level revenues and earnings, comparable sales were down 4.3%, which was more than the 3.3% decrease expected heading in. Similar to HD, LOW was negatively affected by lumber deflation and unfavorable weather, as well as lower DIY discretionary sales.

How Did Results Compare To HD?

In their Q1 release last week, HD reported a 4.5% decline in comparable-store sales. This marked the second consecutive quarter of YOY declines. The metric also came in well below estimates of a 1.7% decline.

LOW, similarly, reported a decline, though the extent of their miss was less significant than HD, at about 100 basis points (“bps”) versus a 280bps miss by HD.

In addition, HD warned that total sales would be down on the year by between 2% and 5%. This didn’t differ all that much from LOW, who guided for a 2% to 4% decline. For both companies, the revision represented a notable pivot away from their guidance in Q4, which called for sales to be flat for the year.

HD also recorded nearly 5% fewer transactions during the quarter. And this would be on average prices that were essentially flat for the period. Despite the softened sales environment, HD was still able to keep operating margins in the 15% range for the quarter.

Nevertheless, that didn’t change HD’s outlook for overall earnings, which are now expected to drop by between 7% and 13% for the year on an expected decline in margins to the 14% to 14.3% range.

LOW, on the other hand, is operating in the 13% range on adjusted margins and sees adjusted earnings at a midpoint of $13.40/share. This would be down about 3% from fiscal 2022.

What Does Lowe’s Expect Moving Forward?

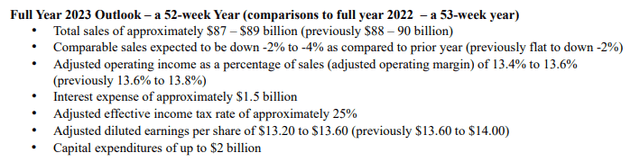

Headwinds in the lumber market and softness in DIY discretionary sales resulted in negative revisions to full year guidance.

Notable updates include a downward revision in comparable sales to an expected decline of between 2% and 4%. This is from expectations of a maximum decline of 2% previously.

Q1FY23 Earnings Release – FY23 Guidance

Expected adjusted operating margin was also revised lower, though the magnitude of this adjustment is less significant due to the synergies derived from their productivity initiatives.

Overall earnings, however, are expected to range from $13.20/share at the low to $13.60/share at the high. This would be shy of consensus estimates of $13.64/share.

What To Do with LOW Following Earnings?

LOW’s first quarter results weren’t markedly different than what HD had reported last week. Comparable sales were down 4.3%. This is about the same decline reported by HD. Expectations were missed in both instances, though LOW was off less than HD.

Looking ahead, guidance was revised lower due to headwinds arising out of the lumber market, as well as softness in their DIY discretionary category. Again, this is similar to the challenges noted by HD on their release.

Presently, LOW trades at around 15x their forward earnings multiple. This compares to 19x for HD. In a sense, the discount is warranted due to their market positioning and their lower adjusted operating margins.

Still, the operational performance between the two isn’t that far off. And LOW has been performing stronger of late and has been generally closer to estimates than HD. For investors in a pick and choose mode, I’d favor LOW over HD due to their relative valuation, stronger forward guidance, and the positive overall long-term outlook.

Read the full article here