CVS Health (NYSE:CVS) is a leading healthcare company with an extensive network of pharmacies and medical clinics in the United States. CVS Health’s subsidiaries serve tens of millions of Americans every year with access to prescription drugs, counseling, and extensive care for older people, with the ultimate goal of improving their quality of life. Through the acquisition of Aetna in 2018, the company has significantly expanded its presence in the health insurance industry, and about 35 million people have access to a wide range of health plans, including Medicare Supplement and Medicare Advantage plans.

Author’s elaboration, based on 10-Q

On May 3, 2023, CVS Health released financial results for the first three months of 2023, which not only beat analysts’ expectations but were able to demonstrate that demand for services and products from the company’s three core segments is growing at a faster pace, despite a significant decline in COVID-19 and influenza activity.

Since the beginning of 2023, CVS Health’s share price has decreased by about 27%, reaching March 2021 levels. At the same time, share prices of key competitors such as Quest Diagnostics (DGX), Walgreens Boots Alliance (WBA), and Cigna (CI) demonstrated more favorable dynamics.

Author’s elaboration, based on Seeking Alpha

We initiate our coverage of CVS Health with an “outperform” rating for the next 12 months.

CVS Health’s Financial Position

CVS Health’s revenue for the first three months of 2023 was $84.94 billion, up 1.7% from the previous quarter and 10.8% from the first quarter of 2022. Since the beginning of 2022, CVS Health has been beating analyst consensus estimates by a relatively large margin, thanks to the company’s expanding product portfolio, strong sales of consumer health products, and strong demand for medical services during the COVID-19 pandemic and flu season.

Author’s elaboration, based on Seeking Alpha

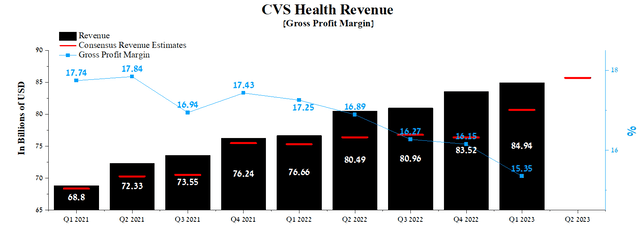

CVS Health’s revenue is expected to continue to show positive dynamics and be $83.09-87.52 billion for the second quarter of 2023, up 6.1% from Wall Street analysts’ expectations for the first quarter of 2023. However, the negative point that Mr. Market did not like is the decline in revenue growth rates. There are several factors contributing to the emerging trend.

The first of these is the decision by the Department of Health and Human Services to end the public health emergency from the end of May 11, 2023. After this date, Medicaid redeterminations resume, which means that the necessary checks will be carried out to ensure that patients meet the requirements of CHIP and Medicaid. As a result, CVS Health’s Medicaid business could see some customers lose coverage, hurting the company’s revenue growth in the next two quarters. In addition, Americans with traditional Medicare will no longer be able to get free COVID-19 tests, which will also reduce services provided by CVS Health subsidiaries.

The second factor is the decline in influenza and COVID-19 activity until mid-autumn. As a result, we expect the US government to reduce spending on these respiratory infections, including vaccinations and population testing. According to the CDC, at week nineteen, only 1.9% of patient visits were related to respiratory illnesses, including fever, cough, and sore throat. In the chart below, you can see a formed trend in recent years that the situation with flu is stable until the end of October.

Centers for Disease Control and Prevention

As a result, we do not expect a sharp increase in the number of prescriptions prescribed in the coming months, which will negatively affect the pace of revenue growth in the Pharmacy & Consumer Wellness segment until the end of the third quarter of 2023.

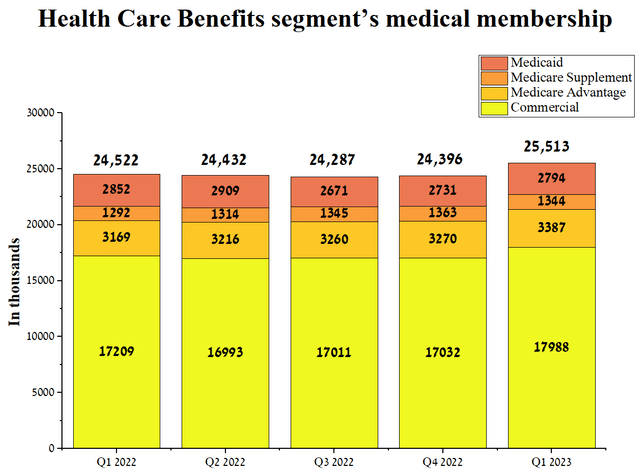

But despite the decline in excessive demand for health products and the decrease in the burden on the healthcare system after the end of the COVID-19 pandemic, the innovative business strategies implemented under the leadership of Karen Lynch are bearing fruit. For example, the Medical Benefits segment continues to grow at a rapid pace, with revenue of $24.34 billion in the first three months of 2023, up 12.6% from Q1 2022. Medical membership was about 25.5 million people in the first quarter of 2023, showing an increase of 991 thousand members from the previous year and 1.12 million from the prior quarter.

Author’s elaboration, based on quarterly securities reports

Moreover, we expect CVS Health’s revenue in this segment to continue growing at high single-digit percentages in the coming quarters. However, from 2024, the growth rate will increase even more thanks to the contract concluded with New York for a group Medicare Advantage plan, which will begin to operate from September 1, 2023. Karen Lynch said the following on the Q1 2023 earnings call.

We look forward to providing access to high quality, affordable, and convenient healthcare to the city’s more than 200,000 retirees and their eligible dependents. We now expect approximately 12% membership growth in our Medicare Advantage business for the full year 2023 and are diligently working to improve our competitive position in individual MA to return to market growth in 2024. The recent award of two additional Marquee Group Medicare Advantage contracts serving approximately 45,000 retirees and their eligible dependents will supplement that growth beginning in January of 2024.

CVS Health’s gross margin was 15.35% in Q1 2023, hitting some of the lowest in recent quarters due to rising wages, product costs, and increased competition for government-sponsored health insurance programs like Medicare and Medicaid. However, we forecast that the company’s gross margin will rise to 16.7% by the end of 2023 and 17.8% by 2024, thanks to lower inflation and an improved global supply chain.

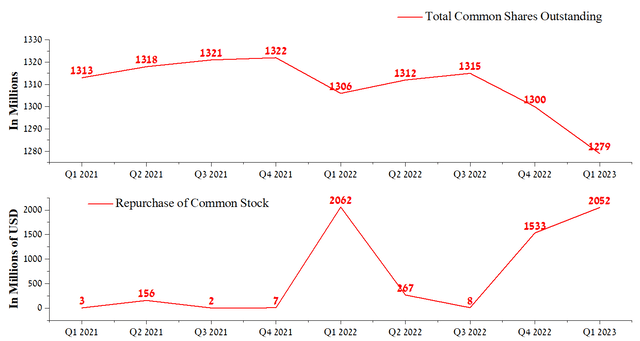

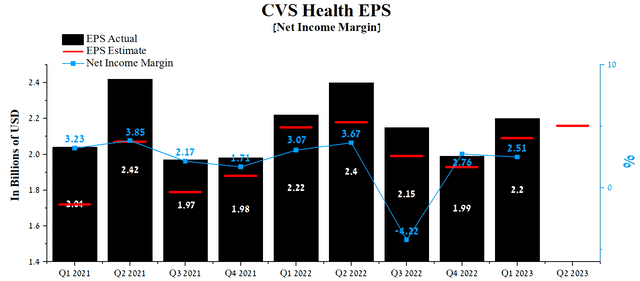

Unlike major CVS Health competitors such as Humana (HUM), Walgreens Boots Alliance, and UnitedHealth Group (UNH), the company’s net income margin is much lower than theirs. In the 1st quarter of 2023, it amounted to 2.51%, slightly decreasing compared to the previous quarter. CVS Health’s earnings per share (EPS) for the first three months of 2023 was $2.2, down 0.9% from Q1 2022, but it continued to beat analyst consensus estimates in recent years. One of the reasons for this emerging positive trend is the active use of the company’s share buyback programs. In the first quarter of 2023, CVS Health repurchased its shares for about $2.05 billion, while Karen Lynch still has the option of repurchasing the company’s shares up to $14.5 billion, which, in our estimation, is enough to support the price of CVS Health’s shares during possible macroeconomic shocks.

Author’s elaboration, based on Seeking Alpha

CVS Health’s Q2 EPS is expected to be in the $2.01-$2.41 range, up 2.9% on average from the Q1 2023 consensus estimate. At the same time, CVS Health’s Non-GAAP P/E (TTM) is 7.94x, which is 57.36% less than the average for the sector and 20.64% less than the average over the past five years, which is one of the factors indicating that Wall Street undervalues the company.

Author’s elaboration, based on Seeking Alpha

We expect the net income margin to ease slightly over the next two quarters due to the acquisitions of Signify Health and Oak Street Health. However, from the end of 2023, CVS Health’s management and investors will begin to feel the benefits of the company’s expansion, thanks to its increase in its share in the rapidly growing market for care and provision of medical services to people at home.

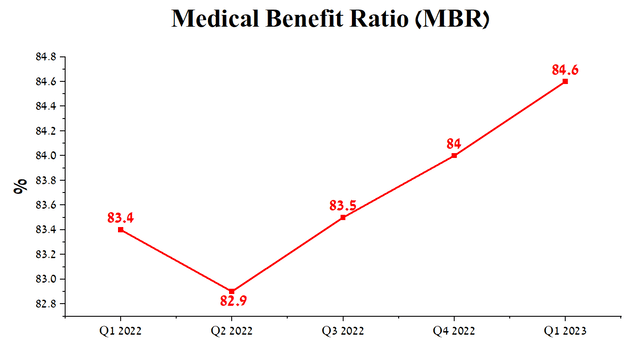

Another factor that, on the one hand, favorably affects CVS Health customers but, on the other hand, puts pressure on the company’s marginality is the growth of the medical benefit ratio (MBR). The medical benefit ratio shows what percentage of premium revenue goes towards paying for medical services for its clients. At the same time, the higher the MBR, the less money CVS Health receives from insurance premiums, which can be spent on administrative costs, marketing, and wages. So, MBR was 84.6% for the first quarter of 2023, an increase of 1.2% from the previous year and 0.6% in the last quarter.

Author’s elaboration, based on quarterly securities reports

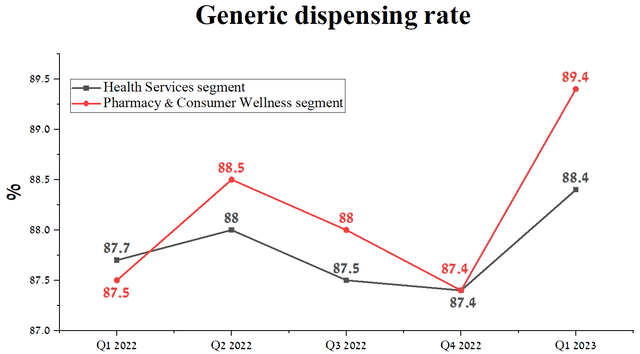

In the first three months of 2023, the generic dispensing rate in two of the company’s core segments, Pharmacy & Consumer Wellness, and Health Services, increased relative to previous quarters.

Author’s elaboration, based on quarterly securities reports

We believe the increase in this share mainly benefits CVS Health’s revenue and has a slightly less noticeable impact on its margins. In most cases, pharmacy benefit managers encourage chain pharmacies to dispense generics and, in return, offer higher reimbursement rates for them than for branded drugs. In addition, dozens of pharmaceutical companies can produce generic versions of patented medicines, and as a result, competition between them is extremely high, which affects the reduction in prices for these drugs. As one of the healthcare segment leaders, CVS Health can purchase generics on more favorable terms, ultimately allowing it to control margins flexibly. In addition, in recent years, an increasing number of generic drugs have appeared on the market that are highly effective, but at the same time, the price for them is several times lower than recently approved medicines. Increasing the share of generic prescriptions reduces Americans’ healthcare costs. Ultimately, this increases the volume of prescriptions filled and improves CVS Health’s reputation as a company that values its customers.

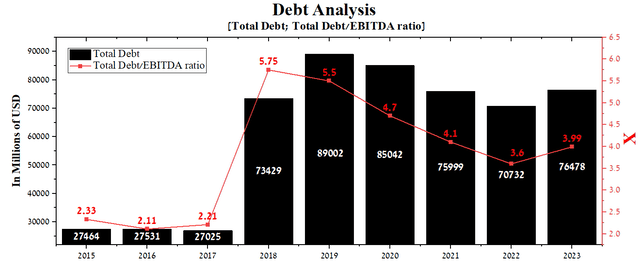

At the end of Q1 2023, CVS Health’s total debt stood at about $76.48 billion, up slightly from 2021 due to the closing of the Signify Health and Oak Street Health acquisitions. However, due to the growth of the company’s EBITDA in recent years, the total debt/EBITDA ratio has decreased from 4.1x to 3.99x.

Author’s elaboration, based on Seeking Alpha

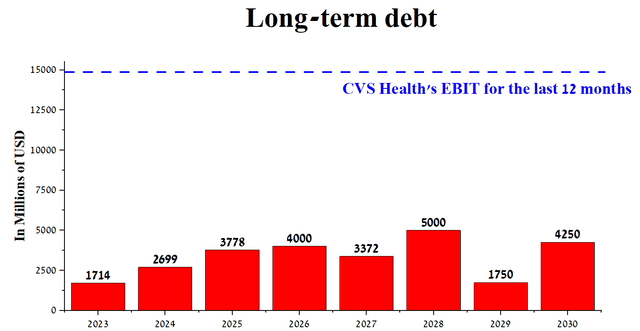

Given the company’s significant amount of cash, we do not expect CVS Health to have problems redeeming its senior notes, and the company will be able to increase dividend payouts further and pursue an active M&A policy.

Author’s elaboration, based on 10-Q

Conclusion

CVS Health is a leading healthcare company with an extensive network of pharmacies and medical clinics in the United States. CVS Health’s subsidiaries serve tens of millions of Americans every year with access to prescription drugs, counseling, and extensive care for older people, with the ultimate goal of improving their quality of life.

Under Karen Lynch’s leadership, CVS Health’s business continues to thrive, despite a temporary decline in its margins after the end of the COVID-19 pandemic and flu season, which contributed to a sharp increase in spending by the US government to combat them.

The next two quarters will be a period of ongoing transformation within CVS Health’s structure following the acquisition of Signify Health and Oak Street Health, which will then significantly contribute to improving the company’s financial position. We expect that during this period, the company’s share price will be in an accumulation phase and will move from $63.5 to $71 per share. And already, from the end of 2024, when we expect the Fed to start cutting interest rates and CVS Health’s gross margin and net margin also begin to improve, many investors will pay attention to it, which is one of the brightest gems among dividend companies.

We initiate our coverage of CVS Health with an “outperform” rating for the next 12 months.

Read the full article here