Investment Thesis

3D Systems Corporation (NYSE:DDD) offers global 3D printing and digital manufacturing solutions. It provides 3D printer technologies, printing materials (nylon, plastic, metal, wax), digital design tools, and software solutions. DDD also provides software, precision health, manufacturing, maintenance, and training services.

The company’s stock price has decreased by around 18.5% during the previous year, partly attributable to its performance. DDD has registered net losses and negative earnings over the trailing twelve months. In response, it has developed initiatives to help improve this situation. On top of that, 3D Systems recently entered a deal to acquire a Swedish 3D manufacturer and has a long-term partnership with TE connectivity. These developments could be instrumental in ensuring the company’s growth.

Its balance sheet is fairly levered and has more cash than its total debt. Like any other company, DDD bears risks, as it is forecasted to remain unprofitable for a few years and is considerably overvalued with respect to its price-to-sales ratio. Despite its optimistic future, the estimated loss-making projections lead me to a hold rating as the company turns things around on its profitability.

Restructuring Initiatives

As mentioned earlier, the company has been unprofitable for quite a while. As it has reported net losses, therefore, negative earnings, it is only natural that it finds ways to change this dire situation. DDD has developed restructuring initiatives to help salvage it by improving efficiencies in its operations to create value to benefit its shareholders and customers.

One of the approaches is regarding its European metal printer operations. 3D Systems will insource particular metal printer platforms into its manufacturing facility in Riom, France. This will also involve bringing together its manufacturing operations with the existing engineering metal printers. This action will shorten the cycle time from development to production and simultaneously enhance operating efficiencies. DDD expects the initiative to tone down its operating expenses by about $2.5 to $3.5 million in 2023 and yield annualized savings of about $5.5 to $7 million starting in 2024.

The other aspect of its restructuring initiative is downsizing its employees. Following this action, the company anticipates incurring severance payment costs ranging from $3.5 to $4.5 million during 2023. The initiative is expected to cut operational expenses by about $4 to $6 million in 2023 and yield annualized savings ranging from approximately $9 to $11 million starting in 2024.

3D Systems approaches, which largely involve adjusting their costs to a sustainable level, reflect their efforts to attain positive bottom lines and positive earnings.

Brighter Future?

The company disclosed its long-term collaborative partnership with TE Connectivity, a global leader in sensors and connectors. They’ll develop an additive manufacturing solution to produce electric connectors in unison. This collaboration will benefit TE Connectivity by enhancing its efficiency to meet customer demand. The partnership also shows great potential to become an exceptionally important market in the future for 3D Systems additive manufacturing technology.

The company has also entered a deal to acquire Wematter, a manufacturer of 3D printers based in Sweden. Wematter has designed an unrivaled Selective Laser Sintering [SLS] solution that enables additive manufacturing in smaller environments/settings, previously regarded as impossible. Through this acquisition, the company will expand its SLS portfolio and gain from Wematter’s teams’ expertise and distinctive engineering approach, a valuable asset to the DDD’s R&D organization. It will also be able to provide a reliable and affordable SLS solution to a wider range of customers.

What of its Balance Sheet?

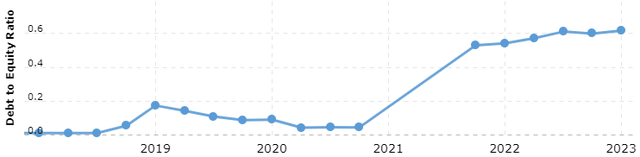

DDD has a total debt of $515.95milion an increase from $501.1 million in March 2022. Its debt-to-equity ratio has also increased over the last half decade from 0 to 70.5%. Nevertheless, it has $529.9 million in cash resulting to net cash of $14 million.

Macrotrends

Looking at the company’s liabilities, its total liabilities exceed its cash and receivables by $86.2 million, signaling fewer liquid assets than its total liabilities. Its unprofitability, and negative earnings, make it impossible to pay its interest expenses. The debt level causes more concern, especially because of the company’s inability to generate positive cashflows and earnings. 3D Systems needs to raise capital should it continue with this trend, which could dilute shareholders.

Risks

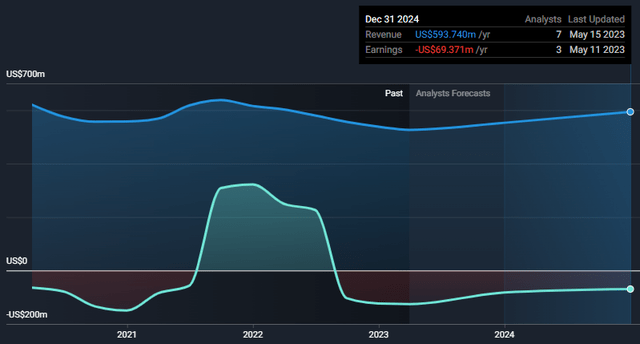

In addition to its unprofitability, it is forecasted to remain so for the next three years. Its earnings are also projected to grow negatively even at the end 2024.

Simply Wall Street

It is also considerably overvalued in its price-to-sales ratio (2.09), outpacing the sector’s median of 1.30. This shows that it is expensive compared to the industry and may be priced at a level that does not reflect its performance.

Conclusion

DDD has been reporting net losses and, in response, has developed restructuring initiatives that largely focus on cost reduction to generate profits at least. Its recent acquisition and long-term partnership seem promising and could be instrumental in improving its growth and performance going forward. There are signs of optimism, but given the long spell of projected poor profitability, investors should hold as the company turns things around.

Read the full article here