Author’s Note: This article was published on iREIT on Alpha in April of 2022.

Dear subscribers,

So, AvalonBay (NYSE:AVB). I’ve been a proponent of increasing one’s REIT/RE exposure in 2023. My own ambition is to double it from 10-12% to potentially 25%. I’m currently at around 16% – and I’m doing more as I see great opportunities.

AvalonBay recently reported results – and those results beat expectations, resulting in a forecast raise. I personally believe this REIT is in for a significant RoR, despite its exposure to the west coast. Like its sibling company, Essex (ESS), it shares some of the risks and issues found here – but also comes with many of the same advantages.

Let’s review it and provide an update for the rest of 2023.

AvalonBay – A significant upside remains

So, AVB did great during 1Q. The company reported, like ESS, core FFO growth. In AVB’s case, it was even higher at a 13.7% YoY growth, with a revenue growth of 9.5% YoY, and 1.5% sequentially.

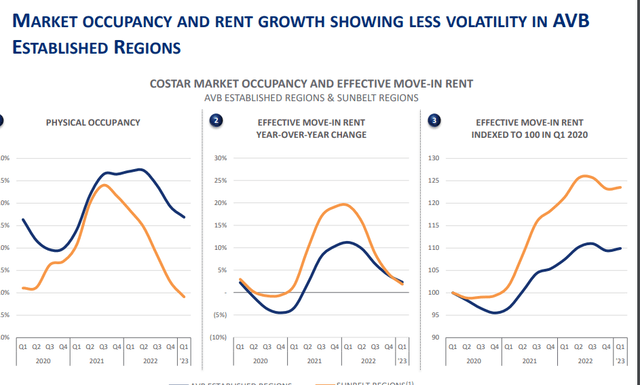

Yes, occupancy and rents are taking a hit. How could it be different given the areas where AVB’s communities are located? But overall, the company is doing better in most things than in other areas, including the Sunbelt regions.

AVB IR (AVB IR)

AVB has a lot of confidence here. The reason is they believe the company’s regions where the establishment is present from AVB, will be relatively insulated from new apartment deliveries during all of ’23, which obviously will increase the demand for what actually is there. Rent growth in the west coast is down, yes – but the drop is decelerating, and the east coast results are actually stabilizing.

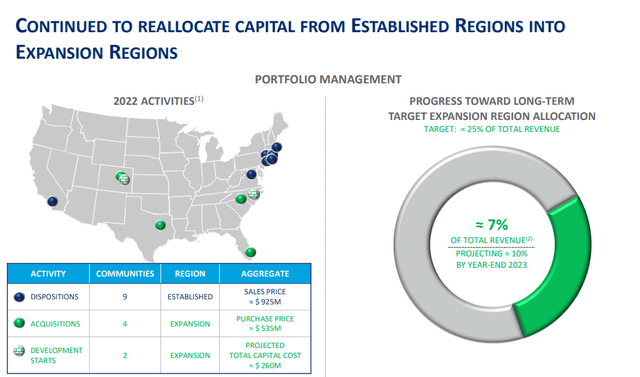

AVB has also been actively disposing and expanding, moving from legacy northeastern and western into becoming more of a sunbelt REIT.

AVB IR (AVB IR)

AVB continues to view its portfolio as being exposed to regions with structural advantages – as we’ve seen with ESS, not all west coast regions are similar. There are pockets of weakness, but AVB’s exposure to these remains limited. Moreover, the company’s established regions are expected to be extremely supply-constrained in terms of new apartments. This alone should at least cushion the fall here and lessen the potential fall that was expected here, and has been integral in the share price drop we’ve been seeing.

AVB isn’t as undervalued as ESS – not in terms of multiples. Like ESS, AVB typically trades at a premium above 20x – now it’s below 20x. ESS is at 15x, and AVB is around 18x. So, not as undervalued – but AVB is also expected to grow more than ESS, owing to its expansion projects and focus on going into sunbelt regions.

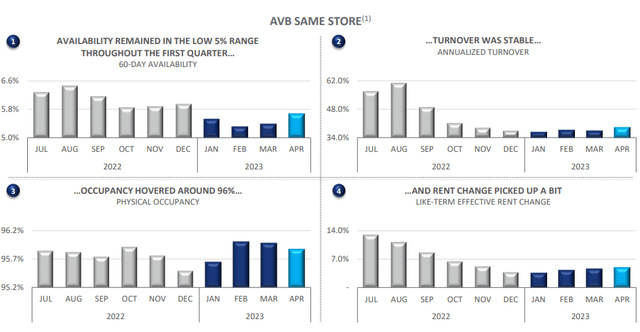

Any underlying indicator you can look at, things are if not positive, at least stable.

AVB IR (AVB IR)

Current lease-up trends are actually outperforming expectations, with plenty of more lease-ups on the way. The company also has developments ongoing, that are expected to bring yet another $130M of NOI to the table once leased and stabilized.

AVB is simply, a very good company – that is why my position in this REIT is even larger than ESS, and I bought it far cheaper. Why is AVB so great?

AvalonBay is one of the premier residential REITs out there. It has an EV of closing in on $40B, and owns 290+ apartment communities in 25 markets, with over a billion in active construction, at this time despite challenges. Its dividend is safe – it has a 5% annualized DGR since its IPO and has averaged nearly 13% TSR since that IPO, making it a better bet than the broader market. Some very basic, and some very positive facts.

The company has an A-rating in credit, less than 5.5x net debt/core EBITDA, a 6x+ interest coverage, a 93%+ unencumbered NOI, and a payout in terms of FFO that goes below the 70% range for the 2023-2024E period. Those 3-4% you’re getting when you invest in AVB, that’s “safe cash”.

Its source of alpha, which is after all that we’re seeing comes from a number of things:

-

Knowledge of the markets in which they invest

-

Scale and operating platform technology.

-

Growth platforms, M&A’s, renos/development.

-

Superb portfolio management

-

Capital management.

You do “have to” hold the stance that the west coast isn’t worthless geography. If you’re very bearish on the overall west coast, then I would probably reconsider AVB – because it’s a play on those geographies. Me, I believe that AVB has what it takes to outperform even in a worse market and with more challenges.

Yes, the labor market is tightening. But payroll numbers, GDP numbers, and job openings continue to suggest an upside. What little challenges that the company does see can be considered little more than rounding errors in an environment where everyone is tightening the belt. REITs are no different in this.

When I first covered AVB here, it was down 35%. I said then that this is not the type of company that deserves to trade down 35% because of the trends we see from the company or are likely to see.

To me, that has now been confirmed.

The company has raised both the lower and upper end of its 2023E guidance range significantly – $10.21-$10.61, vs. $10.41 average analyst estimate, compared with $10.06-$10.56 in the prior outlook.

The company’s positives are actually back-end loaded this year. Some of the risks we could discuss include when costs are starting to come down – because if costs do not come down, that would impact the company’s yields versus its targets, which are currently at the low 6% level. AVB is still looking for about a 100-150 bps spread when it comes to new starts, and unlike many other REITs in this sector, AVB is still doing a lot of new starts. So how the company handles these will be something to look at – however, AVB is a lot like ESS in a lot of ways – a lot of good ways.

The company’s larger and more spread-out exposure does account for more volatility – which is why the accuracy rates from analysts aren’t as high as for ESS, an 8% miss ratio with a 10-20% MoE – but nothing to really expect too much negativity from.

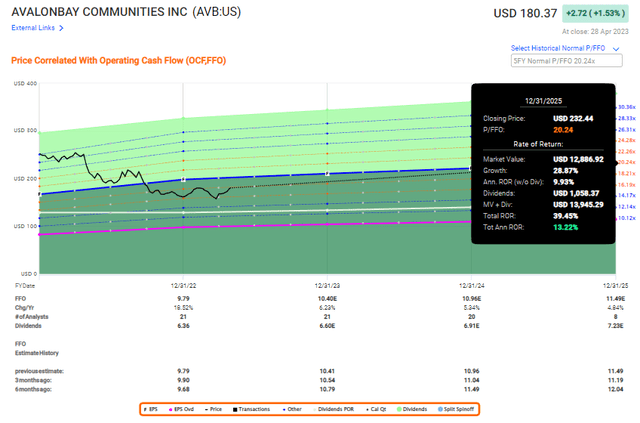

When I last wrote about AVB prior to my first article here on iREIT, the company was almost at $250/share, which was close to 30x P/FFO. I would steer well clear of the company at this point.

The company has been below $160/share, and I’ve been slowly accumulating shares over the past few months as we’ve been troughing.

We’ve now started to climb.

F.A.S.T Graphs AVB upside (F.A.S.T graphs)

The upside to full normalization is well above double digits – though it’s not at the level of ESS, and it’s not at the level of market-beating RoR at a 15x forward P/FFO. That’s why when putting ESS and AVB next to one another, I would go for ESS before AVB here.

Remember the market’s tendency to overreact in either direction. I bought nearly 2% of AVB in COVID-19 and sold it at a nearly 110% RoR when the company was close to $250 and above. Exactly as presented to you in the initial part of this article. Every business has a trim and a “BUY” target.

The company’s relative yield is close to 3.7%, it’s trading at an 18x P/FFO compared to a typical multiple of over 20x. What’s more, the company is expected to improve its FFO for the coming 3 fiscals. How likely is this based on historical accuracy? Quite high – as I’ve said, analysts have a hit ratio of 90% with a 10-20% margin of error. S&P Global analysts are expecting the company dividend to continue to grow at an attractive rate, with a not-insignificant bump coming in next year.

Current valuations have 23 analysts calling for a range between $160/share up to $282/share, with an average of $193/share. Remember, you don’t need to claim for the company to be worth $250. I personally do not view AvalonBay as being worth close to $250/share, and I would trim if I saw that price when I logged into my broker.

No, I just think it’s worth more than $200/share. At iREIT on Alpha, we believe that the company is worth just below $220/share, which implies a current MoS of 21.2%, with a trim target of $265. Those are close to the targets I myself hold for this company.

Outperforming the market is very much possible only with conservative and qualitative investments, and I have no desire for the implied risk that comes with quadruple-digit RoRs or above. That sort of outperformance is what I’ve managed to score for the past couple of years, and that’s without investing too much in risk. What risk i have taken could have easily been substituted for lower-upside investments at no real penalty or lower RoR, if a more conservative approach was desired.

I’m happy with triple-digits over time – and I want my safety.

AVB can very well provide this in the long term – so my message here is clear.

Thesis

- AvalonBay Communities is one of the better apartment REITs out there. It has a decent upside – not as good as some, but good enough to invest in a double-digit upside.

- AVB is A-rated, with a 3.5%+ yield, and promises, if targets are reached, an upside of 13% per year. I don’t see much downside here.

- This company is a “BUY” here, PT $220/share.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I won’t call it cheap here, but it has enough of an upside for a market-beating RoR.

Read the full article here