Thesis

Luminar Technologies (NASDAQ:LAZR) is losing large amounts of money every quarter and has a low quality balance sheet. While the company does have a sizable backlog and is making progress on their business goals, a backlog does not guarantee that that revenue will be profitably earned. Investors can be conservative here and wait for the company to prove they can profitably operate their business before buying shares.

Large Quarterly Losses

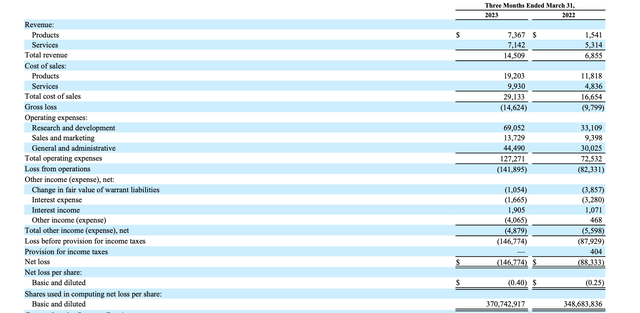

In their most recently reported quarter, Luminar reported revenue of $14,509,000 and an operating loss of $141,895,000. This ratio of losses to revenue is more akin to a startup than a $2.4 billion market cap company. The critical question regarding an investment in Luminar is whether the eventual payoff to investors will justify those investors paying the current price for the shares. We will cover their backlog later, but just because a company has a backlog does not mean that this revenue will have any level of profitability. A company can have a $3 billion backlog, but if the total cost to service that backlog is $3.5 billion the backlog didn’t end up meaning much to investors when it’s all said and done. The company is making gross losses (before operating expenses are factored in), so there is a lot of improvement to be done on this front.

Income Statement (Luminar’s Q1 10-Q)

Luminar’s operating expenses grew from $72,532,000 in Q1 2022 to $127,271,000 in Q1 2023. This implies that the company is still a ways off of realizing operating leverage in their business model. Of note is that a $7,654,000 increase in total revenue was accompanied by an increase of $54,739,000 in operating expenses. This expense growth is to blame for why their operating losses increased from $82,331,000 to $141,895,000.

While it would be nice if we could just assume that companies will gradually reduce their losses over time, this sometimes is not the case. Some companies can be quite large and still have considerable operating losses for longer than many investors initially expect. Conversely, some companies can actually be cost disciplined and show profitability after their start-up phase is over and production is ramped.

Given the evidence so far, Luminar could certainly have some cost discipline problems. Investors should monitor their expense growth going forward to see if expenses continue to grow at such a rapid pace compared to revenue.

Balance Sheet

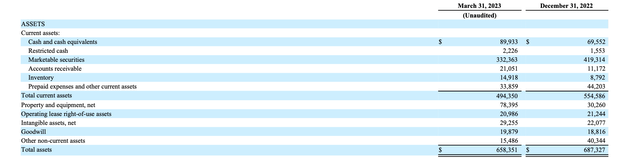

Luminar’s assets are made up of primarily cash and marketable securities. Much of their manufacturing is contracted out, so they don’t need to have significant property and equipment on their books. Likewise, they have a relatively asset light business model with low capex requirements as long as they continue to contract out manufacturing.

Luminar Q1 10-Q

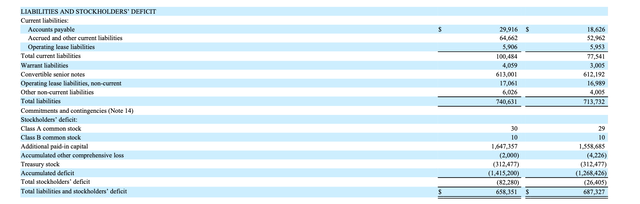

The problem with Luminar’s balance sheet lies on the liabilities side of the equation. The company has almost as much convertible debt on its books as their total assets. Their book value is negative. The entirety of Luminar’s value to investors is going to come from future cash flows, and current investors will likely be required to stomach many more quarters or even years of operating losses before Luminar achieves consistent profitability. Some form of dilution will probably be on the table in the near future. All of this means that the present value of Luminar shares in our opinion is below where the stock is currently trading. As it currently stands, investors are being asked to tolerate a lot of risk and uncertainty in the name, and current price levels do not make the risk/reward favorable.

Luminar Q1 10-Q

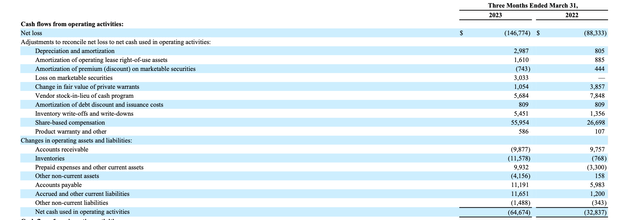

There is not much stock based compensation here relative to their net loss, which means that the company is burning a lot of cash. Luminar may need to do an equity or debt raise in the future to cover their growing cash burn.

Luminar Q1 10-Q

Backlog and Business Progress

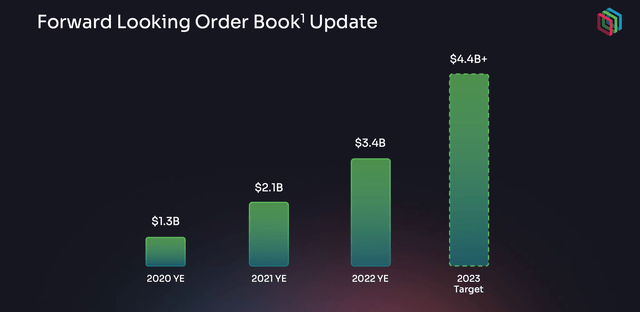

Luminar details their order backlog in their Luminar Day 2023 Investor Presentation. While impressive, this backlog does not guarantee anything for investors. Luminar must not only fulfill these orders, they also need to do so profitably for it to be beneficial to shareholders. Whether or not Luminar can profitably run their business remains to be seen, and they will need to improve their cost discipline going forward.

Luminar

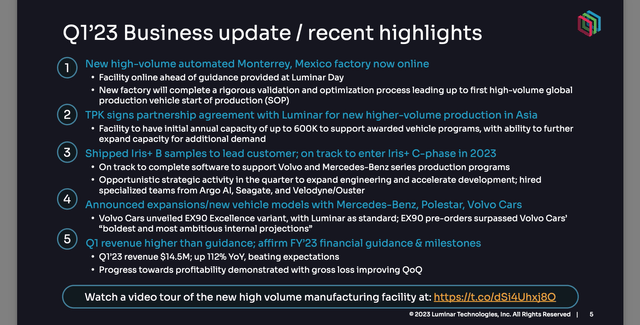

Luminar’s recent business highlights are all solid developments for the company. This is part of why investors have been willing to give Luminar the benefit of the doubt. The company is continuing to reach new milestones and sign new partnerships.

Luminar Q1 Earnings Presentation

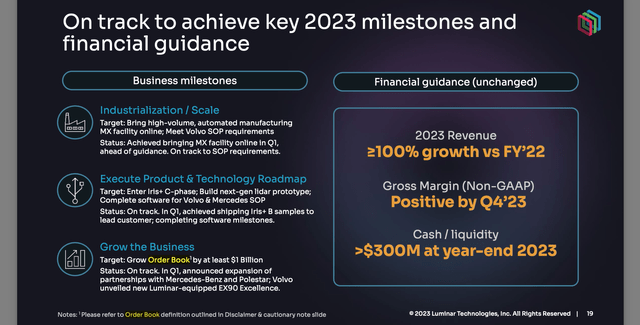

The company is continuing to execute regarding their 2023 milestones and financial guidance. The only figures that I am uncertain about are the cash/liquidity position and non-GAAP gross margin guidance. In order for the company to achieve this guidance, they either need to drastically reduce their cost base in a short period of time or shift more of their compensation to SBC. I suspect they will go with the latter option.

Luminar Q1 Earnings Presentation

Price Action

Luminar was very hyped around the beginning of 2021, but has since seen relatively steady share price declines. This year hasn’t been terrible for the stock, and the company is continuing to improve their business. Just because a stock has declined in value by a lot does not mean that the company is damaged. In this case, the company is even stronger than it was when shares were trading above $30 a share. We still view shares as being overvalued at these levels, but the price now is much more reasonable than it has been in the past.

Finviz

Valuation

Since the company is unprofitable, has a negative book value, and a PS ratio of 50 there is not much to go off of from a fundamental basis. An investment in Luminar at this stage is purely an investment in the company’s ability to realize their long-term vision. A lot has to right for investors to be adequately compensated for taking this risk. Everyone certainly could go right, but we would wait until the fundamental picture becomes more favorable before taking a position here.

Everyone likes to point to companies such as Tesla and Amazon as a reason to blindly invest in a company while their fundamental picture is hazy. While there certainly is the largest potential return from these types of investments, investors who waited until Tesla and Amazon were profitable before investing also made quite good returns without taking as much risk, as well as being protected from if those companies ended up not meeting expectations. For every Tesla and Amazon, there are 100 companies that go bust and are only remembered by the bag holders. Investors should be cautious when faced with companies that are unproven, and understand that it is okay to watch and wait on the sidelines.

Risks

A risk to this bearish thesis is Luminar’s ability to rapidly monetize their product offerings while continuing to sign new strategic partnerships. This would justify the premium investors are currently willing to pay, and cause Luminar to be fundamentally undervalued at these prices.

Despite what can go right, we view the risk/reward as being unfavorable and lean towards being cautious in this environment. In our book, Luminar is a show me story.

Key Takeaway

We view Luminar as being fundamentally overvalued in light of their operating losses and poor balance sheet. Investors can be conservative and wait for the company to prove that they can profitably run their business before taking another look here.

Read the full article here