Quality investing comes in different flavors, and the popular concept of an economic moat is one of a myriad of quality-centered approaches to selecting the most robust players, possibly with an adequate immunity to the repercussions of a recession, for a long-term portfolio with an outperformance potential.

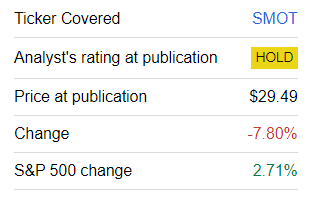

Incepted last year, the VanEck Morningstar SMID Moat ETF (BATS:SMOT) is a comparatively novel investment vehicle targeting attractively valued small- and mid-sized U.S. stocks with narrow- and wide-moat characteristics. In my previous note on SMOT published on 22 February 2023, I warned that its upbeat performance since its inception in October 2022 should not be extrapolated.

Seeking Alpha

And since the February note, SMOT has declined by almost 8%, while the S&P 500 index has advanced by 2.7%, now on the brink of entering the bull market.

Why should SMOT be given a second look today?

- First, its lackluster performance delivered since February might have resulted in valuations across the portfolio compressing, thus paving the way for a value/quality thesis.

- Second, SMOT’s underlying index was reconstituted in March, thus the fresh version may contain new plays that are supportive of a more bullish opinion on the fund.

But before delving into the assessment of the current portfolio mix and factor exposure nuances, I believe it is worth quickly summarizing the core principles of SMOT’s strategy.

A quick investment strategy recap

In short, according to its website, SMOT tracks the Morningstar US Small-Mid Cap Moat Focus Index, which is essentially a sub-section of the Morningstar US Small-Mid Cap Index composed of the names that have either narrow or wide moat, or, another way of saying, as clarified in the rulebook, are considered capable of sustaining their competitive advantages for either five or ten years. There are momentum, liquidity, and size screens as well. Also, a value ingredient is added to the strategy as fair value estimates assigned by Morningstar’s equity research team are also taken into account. Importantly, despite the index having simple equal weighting, its reconstitution is rather nuanced, with a quarterly staggered schedule, so I would recommend reading the prospectus, as well as the rulebook for more context on that matter.

Does SMOT deserve an upgrade?

First, let us discuss how the SMOT portfolio has changed since February.

As of May 15, SMOT had a portfolio of 101 holdings (excluding cash), which represents a slight increase from the February version of 95 holdings. Upon closer inspection, it seems that the fund removed 13 stocks that accounted for ~9.5% as of writing the previous article, replacing them with 19 names that now have a ~12.5% weight. The key additions are Biogen (BIIB), Electronic Arts (EA), and Fortune Brands Innovations (FBIN), with 85 bps, 79 bps, and 77 bps weights, respectively.

The sector mix has remained relatively the same, with information technology (a decline of 2.6%) and consumer staples (an increase of 1.4%) having seen the most significant changes.

| Sector | May | February | Change |

| Communication | 7.0% | 7.7% | -0.7% |

| Consumer Discretionary | 19.6% | 20.2% | -0.6% |

| Consumer Staples | 5.0% | 3.6% | 1.4% |

| Energy | 1.7% | 1.0% | 0.7% |

| Financials | 10.8% | 11.1% | -0.3% |

| Health Care | 10.1% | 10.0% | 0.1% |

| Industrials | 19.8% | 19.0% | 0.8% |

| Information Technology | 14.2% | 16.7% | -2.6% |

| Materials | 9.2% | 8.0% | 1.2% |

| Real Estate | 2.5% | 2.7% | -0.2% |

Created by the author using data from SMOT and iShares Russell 3000 ETF

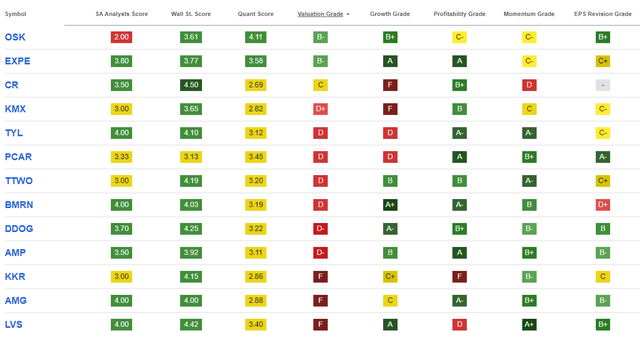

Importantly, most removed stocks currently look fairly overappreciated as illustrated by their Quant Valuation grades except for Oshkosh (OSK) and Expedia (EXPE), so their absence has likely contributed to the improvements in SMOT’s valuation. The minor remark here is that oddly enough, OSK, despite currently trading at rather attractive multiples after an almost 20% three-month price decline, was removed since it failed the price/fair value estimate screen as clarified in the reconstitution report dated 17 March 2023.

Seeking Alpha portfolio tool

Also, KKR & Co. (KKR) and Las Vegas Sands (LVS) score rather poorly against profitability and capital efficiency indicators amalgamated in the Quant Profitability rating, so their removal looks completely rational and justified, especially considering both are seemingly overpriced, which is manifested in the F Valuation grades. And as the reconstitution summary shows, LVS failed the valuation test, while KKR was removed for the reason labeled as “Other” as its lost its place in the selection universe.

What consequences did the recalibration have for the fund’s factor exposure? The following table provides the major metrics worth discussing.

| Metric | February | May |

| WA Market Cap | $17.06 billion | $15.92 billion |

| WA Earnings Yield LTM | 5.3% | 5.8% |

| WA Price/Sales | 3.22x | 3.14x |

| WA EPS Fwd | 10.2% | 9% |

| WA Revenue Fwd | 9.1% | 7.4% |

| WA ROE | 23% | 10.2% |

| WA ROA | 7.5% | 7% |

Created by the author using data from Seeking Alpha and the fund

- First, the removal of expensive names together with a price decline has buoyed SMOT’s value characteristics. More specifically, the weighted-average market cap has dipped to ~$15.9 billion, as of my estimates, allowing the earnings yield to advance slightly to 5.8%, which is marginally above 5.3% of the iShares Core S&P 500 ETF (IVV).

- Interestingly, this was assisted by a minor decrease in the forward EPS growth rate, which makes sense. With the Price/Sales ratio being lower, the forward revenue growth rate has also fallen slightly.

- On a side note, an almost $16 billion market cap suggests that investors seeking small-size moaty opportunities should think twice before buying into SMOT as its performance is principally driven by large-cap plays despite its focus on the small/mid-size echelon; moreover, just about 39% of its portfolio are actually mid-caps (less than $10 billion in market cap), while small caps are not represented, at all.

- Turning to quality, it is worth elaborating here on what caused such a deep decline in Return on Equity. I should immediately clarify that this should not be regarded as a sign of worrisome quality issues emerging. The chief culprit is Etsy (ETSY), an online marketplace player, with its dismal ROE of negative ~1033%. Though this might look horrendous at first glance, the principal reason its sizable goodwill impairment of over $1 billion related to Depop and Elo7, which impacted its 2022 operating income and net earnings, while doing no harm to net operating and free cash flows. For more details, I recommend reading its Form 10-K. Another culprit is Splunk (SPLK), which was added to the portfolio in the wake of the index reconstitution, currently with a weight of 62 bps. SPLK is deeply unprofitable, with an ROE of about 495% below zero, but cash flow-positive.

- The fund’s WA ROA has almost not changed, declining by just ~50 bps. At the same time, the share of stocks with a B- Quant Profitability rating is still solid at 86.4% vs. over 85% previously.

- Most importantly, SMOT is now heavier in stocks priced at a premium to their respective sectors as well as historical levels, with only 16% of the holdings having a B- Quant Valuation rating or better vs. over a quarter previously; 63% now have a D+ rating and worse vs. 49.6% in February.

- Overall, in the light of the developments discussed above, I would not say there is a sufficient reason for a rating upgrade.

Final thoughts

SMOT has a brilliant idea at its crux as blending the value and quality factors using the concept of the moat and fair value estimates is perhaps the best strategy to navigate the current market conditions. But in my view, the equity basket it currently has, as discussed above, does not possess characteristics sufficient for a bullish thesis, and thus the Hold rating is maintained.

Read the full article here