Bank Of America”s Earning Exceed Analysts” Expectations

Bank of America (NYSE:BAC) stock has been falling in price all year long. Down 19.16% for the year as of this writing, it has fared particularly poorly compared to its peer group. For the year, the Vanguard Financials ETF (VFH) is only down 8.75%, so BAC has performed worse than the average bank this year.

Interestingly enough, though, Bank of America has actually been doing well as a business. It beat on revenue and earnings in its most recent quarter and delivered positive growth in profits as well. In a year where many tech stocks have been rallying on 0% earnings growth, BAC’s underperformance appears perplexing.

Of course, the heart of the problem is the regional banking crisis. The failures of Silicon Valley Bank, First Republic (OTCPK:FRCB), and Credit Suisse (CS) have soured sentiment toward the banking sector overall. Most financial ETFs, like the aforementioned VFH, are down for the year. However, this still leaves open the question of BAC’s underperformance compared to other banks. JPMorgan (JPM) is only down 0.04% for the year-why is Bank of America being hit so hard? Obviously, there’s more than just ETF selling at play here, as BAC is behind its sector.

We can never be quite sure what investors were thinking when they sold a particular stock, unless they comment on it. Institutions are only required to report what they bought or sold, not why they did so, so there’s always some ambiguity about why a particular stock is out of favor.

Personally, I have a hunch as to why Bank of America stock is selling off so hard this year:

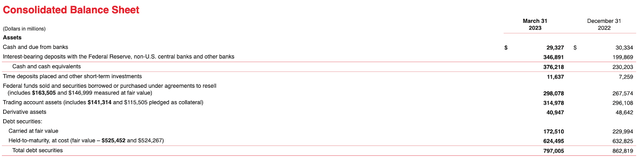

Unrealized securities losses. Many of the banks that failed this past Spring had large amounts of unrealized losses on securities on their books, and Bank of America has even more. As the table below shows, BAC’s $624 billion worth of securities shrinks to $525 billion when adjusted to fair value, leaving a whopping $99 billion in unrealized losses! Granted, that’s down from $120 billion at the end of Q4, but still, investors don’t seem to be taking chances here.

BAC balance sheet highlights (Bank of America)

Bank of America’s $99 billion worth of unrealized losses is the largest amount of such losses among America’s four largest banks. It’s understandable to worry about it a little, but what’s often forgotten is that BAC’s liquidity is still good even after adjusting everything down to fair value. In fact, it actually beats JPMorgan-the bank often called a “fortress” – on liquidity! It’s for this reason that I consider Bank of America to be the best value in the banking sector today, and actually much less risky than most of its peers.

Bank of America’s Liquidity

One of the reasons why Bank of America is not nearly as risky as the markets are making it out to be is because it has a lot of liquidity. If you look at the table above, you’ll notice that the bank has:

-

$376 billion in cash and equivalents.

-

$172 billion in fair value securities.

-

$525 billion in HTM securities when adjusted down to fair value.

That’s $1.073 trillion in liquidity, or 56% of BAC’s total deposit base ($1.9 trillion). This is improved from the same figure in the first quarter (liquid assets were about 51.5% of deposits back then). It’s also better than the same figure for JPMorgan. In its most recent quarter, JPM had:

-

$754.5 billion in cash.

-

$312 billion in available-for-sale securities.

-

$366 billion in held-to-maturity securities.

-

$2.561 trillion in deposits.

All of JPM’s combined cash and investment securities come out to 55.9% of deposits-slightly worse than Bank of America’s 56%! So, it looks extremely likely that the markets are fixating on BAC’s large amount of unrealized losses without really thinking about the overall picture. It’s actually beating the supposedly “safest” name in the industry on liquidity.

Additionally, Bank of America’s cash position is enough to survive a full $376 billion worth of withdrawals. That’s approximately 20% of the bank’s total deposits that could be paid off without the bank even having to sell securities. So, Bank of America appears relatively safe from the perspective of being able to survive a bank run. Additionally, it had an 11.4% CET1 ratio at the end of Q1, improved from the prior quarter, and well above the 4.5% regulatory minimum.

The Profitability Question

Having established that Bank of America is a relatively liquid and well-capitalized bank, we can now turn to the matter of profitability. I think the previous section of this article is adequate enough to prove that Bank of America is relatively safe from the perspective of being able to survive a crisis and that this year’s selloff was overdone if it was based on concerns about liquidity. However, it could be that investors are selling BAC stock because they think it won’t be as profitable going forward as it was in the past. If that’s the case, then BAC’s liquidity isn’t enough to overcome the bears’ thesis on BAC stock.

So, how is Bank of America doing from the perspective of profitability (and related things like growth)?

Below I’ve included some selected profitability and metrics from Bank of America, JPMorgan, and Wells Fargo (WFC), each from their most recent earnings releases. As you can see, BAC’s margins are comparable to those of its closest competitors.

|

BAC |

JPMorgan |

Wells Fargo |

|

|

Net margin |

31.1% |

32.9% |

24% |

|

Return on equity (“ROE”) |

12.5% |

18% |

11.7% |

|

ROTCE |

17.4% |

23% |

14% |

|

Revenue growth (y/y) |

13% |

25% |

16.9% |

|

Earnings growth (y/y) |

15% |

52% |

31.7% |

As you can see, BAC beats WFC on profitability, though it loses to JPM on profitability as well as growth. Based on these numbers, plus the liquidity situation, we’d expect Bank of America to perform comparably to the average of JPM and WFC. Yet, BAC is actually down more than WFC alone-that stock is only down 6.5% for the year! Also, BAC has a lower GAAP P/E ratio and price/book ratio than Wells does and is far cheaper than JPMorgan on both of those metrics. So, it looks like Bank of America is an attractive relative valuation play here.

Risks and Challenges

As I’ve shown so far in this article, Bank of America has been hit far harder than the average bank this year, despite having among the best liquidity of its peers and middle-of-the-pack profitability. It looks like the selloff is overdone, and that BAC is likely the best value play of the big banks. To my mind, that is in fact the case, and I have been buying the dip in BAC stock. Nevertheless, there are some risks and challenges worth keeping in mind here, including:

-

Continued Federal Reserve hawkishness. If the Fed keeps raising rates, then it could cause the value of Bank of America’s treasury holdings to decline. Basically, when the Fed hikes rates, it causes treasuries to decline in value, because selling treasuries is a primary mechanism by which the Fed raises interest rates. In the section on liquidity, I said that BAC’s liquidity was adequate to cover likely deposits, but that could cease to be the case if the bank’s held-to-maturity securities declined in value even further. If that happened, then my analysis would be way off the mark.

-

Lower profitability. Bank of America’s first quarter release showed a marked increase in cash. Evidently, BAC is preparing for further deposit outflows by selling securities. This increase in cash is a positive thing from a risk management perspective, but it also means that there is less cash being deployed to generate returns. So, we could easily find ourselves in a situation where Bank of America foregoes short-term profits for the sake of risk management. BAC has a reputation for being conservative, after all, so we should expect something like this to occur. From the perspective of long-term shareholders, it’s a positive, but it could hold back BAC’s gains this year.

-

More bank failures. If more regional banks fail, then it will likely cause BAC’s stock price to decline in the short term. Each major bank failure incident this year correlated with declines in the prices of big bank stocks. Even after it became clear that the big banks were gaining deposits at the expense of regionals, this relationship was observed. Probably, investors simply sell bank ETFs whenever bank failures occur. In any case, this is a risky environment for those taking short-term positions in bank stocks. My bullishness on Bank of America stock is over a long timeframe, I can’t vouch for the stock performing well this year.

The risks and challenges above are worth keeping in mind. Nevertheless, Bank of America is highly liquid, profitable, and growing, while its stock is the cheapest it’s been in recent memory. The lower it goes, the more I’ll buy.

Read the full article here