Background

SoFi Technologies, Inc. (NASDAQ:SOFI) was founded in 2011 to offer affordable student loan options. After a decade of fast growth and a series of VC fundings, it became a public company via a SPAC sponsored by Chamath in 2021.

It acquired 2 FinTech firms, Galileo ($1.2Bn in 2020), and Technisys ($1.1Bn in 2022), and acquired a national bank charter in Jan 2022.

Anthony Noto (current CEO) became CEO of SoFi in early 2018 after its founder/CEO Mike Cagney resigned in late 2017.

If you want to know more about SoFi, my fellow Seeking Alpha contributor Data Driven Investing has been painstakingly covering SoFi and laying out detailed analyses with well-reasoned bullish takes.

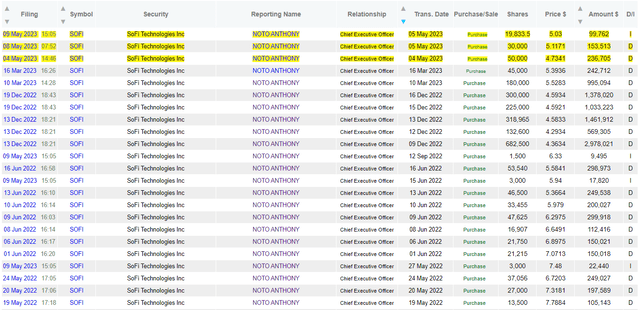

CEO Noto’s Insider Buys

SoFi Bulls point to Noto’s sizeable and repeated insider buys, including his latest $500k+ purchase this month, as strong support for their bullish thesis.

Noto made 20+ purchases, over $11Mn over the last 12 months, a significant amount in relative and absolute terms.

Noto insider activity (Dataroma)

However, today I walk through SoFi’s recent quarter results and discuss a few concerns/red flags that I believe insider buys can’t offset.

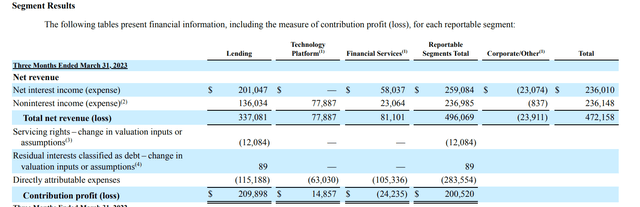

Business Segments

Let me take a detour, quickly examine SoFi’s business segments, highlight its crown jewel, and set the stage and context for the focus of this article – its personal loan lending business.

SoFi has 3 reportable segments, Lending, Technology Platform, and Financial Services.

Lending includes personal, student, and home loans and related servicing.

Technology Platform consists of 2 acquired FinTech firms, Galileo and Technisys.

Financial Services consists of Checking/Savings, Credit card, and Investment.

From its 1Q23 10Q filing, Lending represents ~70% of its total revenue and almost its entire contribution profit. Lending is SoFi’s crown jewel, and within lending its Personal Loan takes the lion’s share in terms of origination, loan book size, and net interest. That is our focus in this article.

segment results (SoFi 10Q 1Q23)

Its personal loan book grew tremendously from less than 2Bn at the start of 2021 to over $10Bn by 1Q23. Currently, it originates between $2.5n to $3Bn each quarter, roughly ~10% total unsecured personal loan market share, one of the top players, together with Lending Club, and to some extent, Upstart, which has a different business model.

Now let’s examine its Q1 2023 results including conference call, 10q filing, and press release.

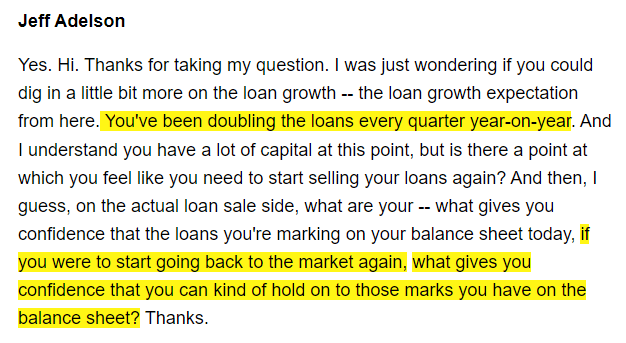

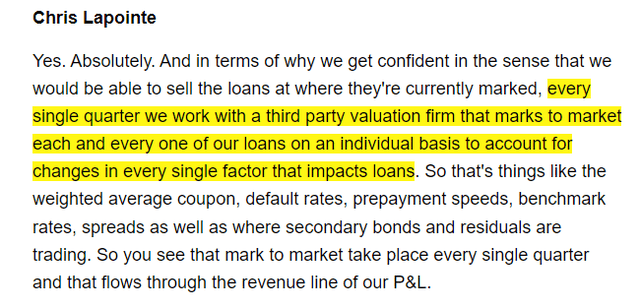

3rd party Valuation Firm

What first caught my eye is the exchange below between Jeff Adelson a sell-side analyst and Chris LaPointe SoFi CFO. When Jeff asked what gives you confidence that SoFi can sell its loan at its marked fair value in the future.

Chris’ response was that marks-to-market is performed by a 3rd party valuation firm.

That sounds perfect on the surface, that an unbiased 3rd party agency conducts loan valuation. However, Loan mark-to-market exercise is the bank’s core competency – saying that’s a bank’s bread and butter is not an overstatement.

What series of events led SoFi to hire a 3rd party agency to perform these core banking activities? I don’t know and it wasn’t asked or explained.

conference call (SoFi 1Q23 cc) conference call (SoFi 1Q23 cc)

Thus, I take that question to examine its 1Q23 10Q filing.

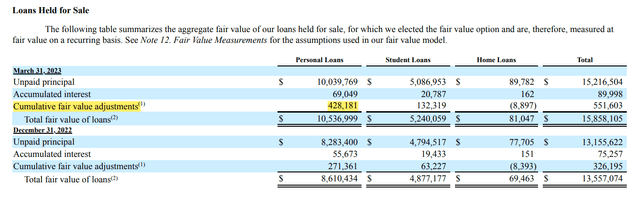

Personal Loans Fair Value

The first thing I noted is its ~$10Bn personal loan remaining principal had a positive $428Mn fair value adjustment in 1Q23, with the noted explanation (Page 16):

The increase in cumulative fair value adjustments for personal loans during the three months ended March 31, 2023 was primarily attributable to higher origination volume and higher coupon rates

Page 15 (SoFi 1Q23 10Q)

How does high origination volume justify a fair value increase?

How can higher coupon rates (assuming the new loans in 1Q23) increase the fair value of its entire loan portfolio?

I have no good answers to both questions.

Let us continue.

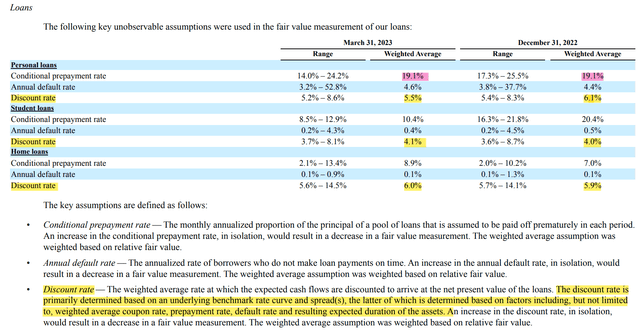

Its entire personal loan is categorized as level 3 in fair value measurements, which use key unobservable assumptions for measurements.

Among its unobservable assumptions, its personal loan discount rate (weighted average) is adjusted from 6.1% in 4Q22 to 5.5% in 1Q23, a 60bps drop, while both its student loans and home loans have a minor 10bps increase.

While the filing didn’t disclose its fair value assessment formula, the discount rate is probably one of the most impactful ratios for FV measurements. (in the discount cash flow model, a lower discount rate increases the present value of the loans)

It went on further explains:

The discount rate is primarily determined based on an underlying benchmark rate curve and spread(s), the latter of which is determined based on factors including, but not limited to, weighted average coupon rate, prepayment rate, default rate and resulting expected duration of the assets

Loan Data (SoFi 1Q23 Filing)

As shown in the table above, the personal loan prepayment rate and default rate remain largely unchanged from 4Q22 to 1Q23. Based on its disclosed annual default rate and lifetime default rate, its personal loan duration has also been relatively consistent at ~18 months for both quarters.

It went on with more explanations (emphasis added):

“The two and five year swap rates declined by 32 bps and 35 bps, respectively, as well as the applicable benchmark rate forward curve. For personal loans, our discount rate assumption in the first quarter reflected the lower benchmark rate and narrower spreads indicated by asset-backed security and secondary bond markets compared to the fourth quarter, but assumed a wider implied spread than our current period securitized deal and our most recent whole loan sale.

There is a lot to unpack from this vague explanation and the full examination is beyond the scope of this article. I just want to highlight that “assumed a wider implied spread than current deal…” best captures its optimistic and wishful thinking with regard to its approach to model the declining discount rate.

If you are still with me, you probably know I’m questioning this third-party valuation firm’s Fair Value Measurement work for SoFi’s personal loans.

Loan Sale

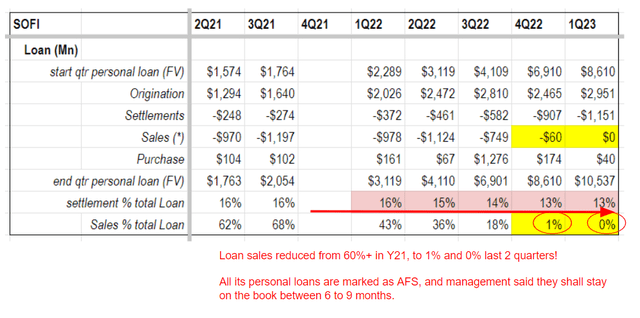

I combed through SoFi’s 7 latest 10Q/K filings and compiled some relevant loan data below to highlight my concerns from a different angle.

compiled by author (SoFi 2022-2023 10Q/10k filings)

Its management said last year, its personal loans are marked as AFS, as on average they stay on the book between 6 to 9 months before sale. That implies it sells about 33% to 50% of its entire loan portfolio each quarter.

From the table above, that proves to be true (Sales%Total Loan – last row), the percentage has been within its projected range until 3Q22.

It suddenly dropped to 18%, and in both 4Q22 and 1Q23, it essentially stopped selling* loans in the marketplace.

* It is worth noting SoFi mentioned in the 1Q23 conference call, it did $400Mn+ securitization in the ABS market. but I failed to find more details in the filing. Without knowing the terms of these packaged ABS deals, it is difficult to assess how close the agreement matches its marked Fair Value.

Noto said the following to explain the sudden stop.

our overall strategy as it relates to loans and when we sell them versus hold them is really driven by liquidity and our ability to optimize return on equity. It’s the same strategy we’ve had since 2018

The other trend I observed is the declining settlement* as a percentage of the total loan. With its avg 18-month duration (prepayment adjusted), we shall expect ~16% settlement each quarter.

That has been slowly declining since 2Q22 and currently stays at 13%.

The 300bps decline looks small but carries significance. For example, if $1.15Bn loan payment in 1Q23 represents 16% of its total loan, its total loan amount shall be $7.2Bn, $1.4Bn less than the reported fair value.

To be fair, that percentage number can be influenced by many factors such as more prepayment, longer loan duration, etc.

I don’t have sufficient data to pinpoint the cause of it but just to note this seemingly minor trend change is potentially very significant.

*settlement is the term SoFi uses in its sec filing, it refers to the loan payment.

Additional Language in 10Q Filing

In its risk section in the latest 10Q filing, SoFi added some notes (vs. 3Q22) worth noting:

2023 GAAP net income profitability is a critical one to avoid capital raise.

It also calls out risks to liquidity and includes the following:

• our ability to sell the loans we originate to third parties;

10Q (SoFi 1Q23) 10Q (SoFi 1Q23)

Connecting the Dots

SoFi has been growing rapidly, and its personal loan book increased 5x+ from less than $2Bn in early 2021 to 10Bn+ as of 1Q23.

While its lending business centers on a gain-on-sale model, and projected 6-9 month average holding time, it has since deviated from that, and essentially frozen the sale process in the last 6 months.

In the meantime, it had 2 favorable fair value adjustments in the last 2 quarters with a total of ~$700Mn appreciation for its ~$10Bn personal loan portfolio.

In the most recent earnings call, when being questioned about their confidence to sell loans at their mark-to-market values, SoFi’s CFO cited using a third-party valuation firm for its loan fair value measurement as a response.

The pieces and bits we examined in its latest1Q23 sec filing didn’t demonstrate compelling reasoning for its fair value adjustment

We know that the unsecured loan marketplace, while currently under macro pressure, operates in an orderly fashion (as we learned from both LendingClub Corporation (LC) and Upstart Holdings, Inc. (UPST) recent quarterly results).

In my opinion, the above dots offer a sufficient amount of information for us to have a reasonable doubt that SoFi might have difficulty finding buyers to purchase its personal loans at its marked Fair value.

If that’s true, its funding source is entirely relying upon continued consumer deposits inflow and the payment from existing loans.

The more concerning thing is if its future personal loan sale would be below its current fair value, its entire loan portfolio would have to re-evaluate, and would have significant downward pressure on its equity, its regulatory capital, as well as its customer confidence.

Concluding Thoughts

Without concrete data points to confirm its personal loan portfolio fair value, a bullish bet on SoFi Technologies, Inc. is a bet on a favorable macro movement (e.g., a lower interest rate, a loose credit market, and friendly consumer deposit env), and equally important taking its management’s words as they are.

I will closely monitor how SoFi Technologies, Inc. handles the ever-growing personal loan portfolio in the coming quarter. In my opinion, it is imperative for SoFi Technologies, Inc. to take concrete measures to demonstrate that its loan fair value measurement is truly marked to market.

Otherwise, the risk is too real to consider owning SoFi Technologies, Inc. stock.

Read the full article here