By James Smith

The Bank of England has raised rates as widely expected to 4.5% – and has kept its options wide open for future meetings.

There are no massive bombshells here – the decision to hike rates was backed by seven committee members, as it was at the previous two meetings. Lots of the post-meeting headlines will focus on the big upgrades to growth, but ultimately this was flagged by the BoE in its previous set of meeting minutes and as much as anything else, it reflects lower natural gas prices over recent months. Importantly, the Bank has retained its deliberately vague forward guidance that further hikes could come if inflation shows greater signs of “persistence”.

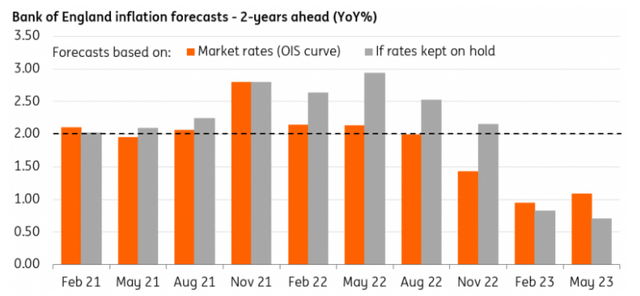

Scratch beneath the surface though, and there are hints that this tightening cycle is reaching its limits. Policymakers often point to the inflation forecast for two-years’ time, the time horizon over which interest rates have their biggest impact. And as we saw in the last set of forecasts from February, the committee sees inflation well below target at around 1% in mid-2025 – and crucially, that’s regardless of whether interest rates follow the path expected by financial markets, or if rates stay fixed at 4.5%.

Admittedly some of this will be accounted for by energy – and the committee has made a point of saying the risks are skewed to the upside. But the simple fact is that the Bank’s own forecast shows little need to take rates higher. As the chart below shows, it’s unusual that the two-year-ahead forecast is so far below target.

The BoE is forecasting inflation well below target in 2 years’ time

Bank of England

What next? We continue to feel that this will most likely mark the top in this tightening cycle, though we accept this is heavily contingent on the next set of wage and inflation data. Another hike in June is possible, though for now not the base case. The Federal Reserve’s much-discussed pause and widely expected rate cuts later this year does provide the BoE with some breathing room.

The more interesting question is when rates will ultimately be cut. Our view is that this is unlikely to be this year, in part because the jobs market is proving resilient. The Bank has watered down its forecasted rise of the unemployment rate, and with that lifted its prediction for wage growth. But equally the story on inflation is starting to look better.

Yes, inflation has been higher than the BoE predicted in February, but that’s largely because of stickier food and goods prices – neither of which are as relevant for monetary policy as service-sector inflation, which has been less unpredictable and appears to be nearing a peak. Survey indicators are suggesting that firms’ pricing expectations are cooling off, and assuming gas prices stay low, we think there are good reasons to think service-sector inflation will fall materially over the next 12 months or so.

With interest rates now, by any reasonable definition, in restrictive territory, we think the Bank will begin the process of taking them back to a more neutral footing with rate cuts by this time next year. We’re penciling in the first cut for May next year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here