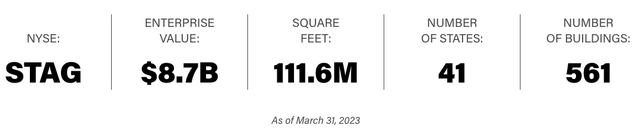

STAG Industrial (NYSE:STAG) is a real estate investment trust that owns properties primarily within the industrial sector. As of Q1 ’23, STAG owned 561 buildings within 41 states in the US that amasses to more than 111 million square feet.

STAG IR

STAG looks to acquire single tenant properties at attractive cap rates within secondary markets, and as you will see below when we take a closer look at the portfolio, they have some high-quality tenants within their top 10.

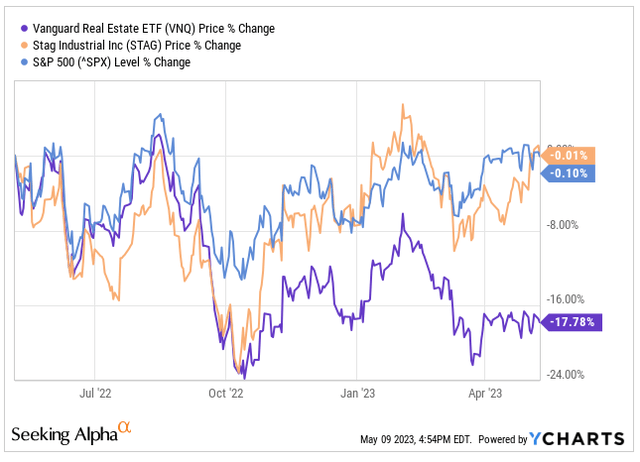

However, the macro environment has been challenging for REITs, which as a sector has been hit hard during this period of rising interest rates. Over the past 12 months, the Vanguard Real Estate ETF (VNQ) is down nearly 20%. STAG and the S&P 500 are neck and neck over the same period about to turn positive, oddly enough.

yCharts

Investors continue to sift through numerous high-quality income stocks that have felt the brunt of rising interest rates over the past year plus. After all, REITs do rely more heavily on debt in order to expand, as they are required to distribute at least 90% of their taxable income to shareholders in the form of dividends. The quality of the company can make a huge difference within the REIT sector. STAG has done a nice job navigating this tough macro environment, and we will look more into that below, but let’s first look at the company’s Q1 earnings, which were released just a few weeks ago.

STAG Quarter Underperforms Its Competition

STAG recently reported their Q1 earnings that topped analyst expectations on the top line with the REIT generating revenues of $173.6 million, easily surpassing analyst expectations of $170.9 million. Q1 FFO was $0.55, which was in-line with analyst expectations.

STAG generated cash NOI of $132.6 million during the quarter, which was an increase of 7.8% year over year. Same-store cash NOI, which is more of an apples to apples comparison, grew 5.9% year over year during the quarter, which was an increase from the 4.5% growth we saw in Q4 ’22.

The occupancy rate at the end of Q1 ’23 was 97.6%, which was a decrease from the 98.5% occupancy rate seen at the close of 2022.

The results were not off the charts, especially when you compare it to another industrial favorite of mine in Prologis (PLD). PLD during the quarter generated record same-store cash NOI growth of 11%, which nearly doubles the growth seen by STAG.

A Look At The Portfolio

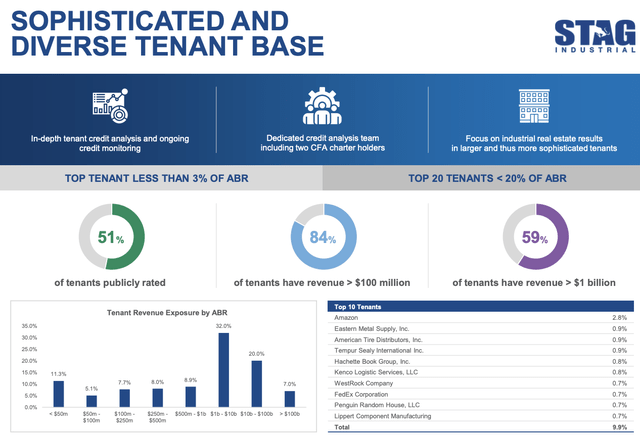

STAG Industrial is known for having a diverse tenant base, as their top 10 tenants account for less than 10% of the company’s annual base rent. As you can see below, no single tenant accounts for more than 2.8%. However, the single largest tenant is quite notable as it is the largest e-commerce company in the world in Amazon (AMZN). Other notable top tenants include American Tire, Tempur Sealy International, and FedEx Corporation (FDX).

STAG Investor Presentation

84% of the company’s top 20 tenants generate revenues in excess of $100 million with 59% of the top 20 generating more than $1 billion in annual revenues.

High Quality, Low Interest Rate Risk

As I mentioned earlier, interest rates can play a huge factor when it comes to REITs. Companies that have to leverage debt and fail to manage it properly would be adversely impacted in a rising rate environment.

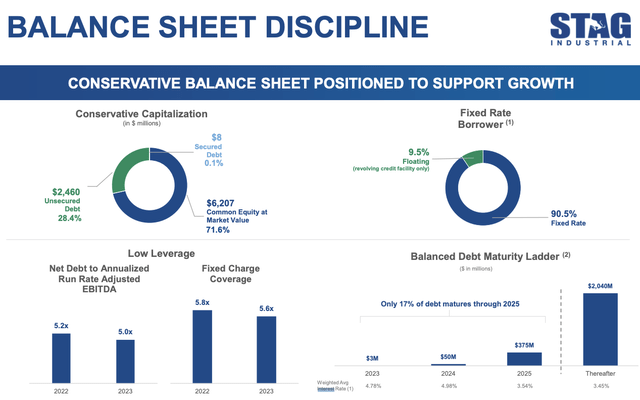

STAG has sone a great job de-leveraging their balance sheet over the years. In fact, 90.5% of their debt is fixed rate debt with a low weighted average rate below 3.5%.

STAG Investor Presentation

Over 80% of the company’s debt matures after the year 2025.

Compelling Valuation and A Monthly Dividend

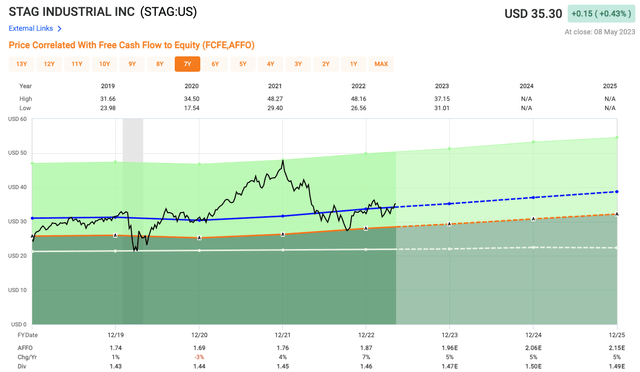

When it comes to valuation, analysts are expecting AFFO growth of 5% for each of the next three years. Analysts expect STAG to produce AFFO of $1.96 in 2023, which equates to a 2023 AFFO multiple of 18x, which is in-line with the company’s 5-year average.

Fast Graphs

However, STAG continues to evolve and the argument could be made that the stock should trade more in the ballpark of a company like Prologis. STAG is not as big as Prologis, but over the past five years, PLD shares have traded at an average AFFO multiple of 27x.

In terms of the dividend, STAG pays a monthly dividend that currently yields 4.2% and has been growing for 11 consecutive years. Given that we are seeing cash NOI growth reignite, I would expect to see dividend growth to pick up as well.

Seeking Alpha

Investor Takeaway

STAG Industrial is a growing REIT that continues to expand within secondary markets across the US. The REIT reported a solid quarter, but it did underperform its competition.

Management has done a great job deleveraging the portfolio as more than 90% of the company’s debt is fixed at a low interest rate, which is huge in the REIT sector.

A slowing US economy could halt a growth for the company, but as e-commerce continues to grow and be a larger percentage of retail sales, which it currently stands around 14%, this will benefit a company like STAG.

Read the full article here