Introduction

As I explained in my recent article on Trican Well Service (OTCPK:TOLWF) (TCW:CA), not all oilfield services were created equal. Whereas Trican has an excellent balance sheet, Ensign Energy Services (TSX:ESI:CA) (OTCPK:ESVIF) is definitely weaker. The company is focusing on deploying its 246 land drill rigs as efficient as possible. As of the end of last year, Ensign has 123 rigs in Canada, 89 in the United States and 34 elsewhere in the world. The company also operates 21 coring rigs and 94 well servicing rigs.

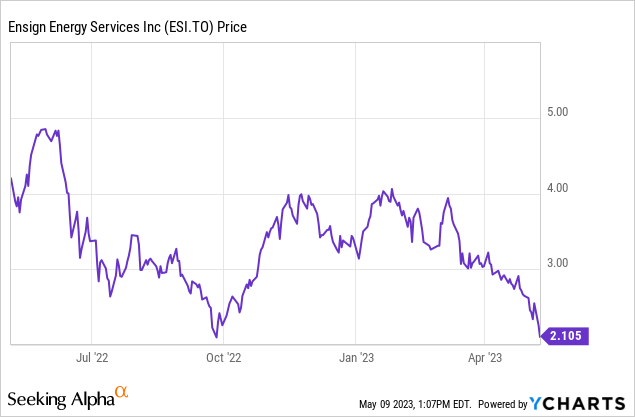

Ensign Energy Services currently has 183.9M shares outstanding and based on the current share price of around C$2 the market capitalization is approximately C$365M. You can find all relevant financial documentation here.

Despite the slowdown on the oil market, Ensign’s revenue and EBIT increased

The financial performance and health of the companies active in the oilfields service industry are closely related to the oil price as that’s the determining factor in the level of field activity. It’s a rather cyclical sector wherein it’s important to make hay when the sun shines and save up for a rainy day.

Despite the gradually weakening oil and gas markets during the first quarter, Ensign reported a strong improvement in its operating results but unfortunately the increasing interest rates are hurting the bottom line.

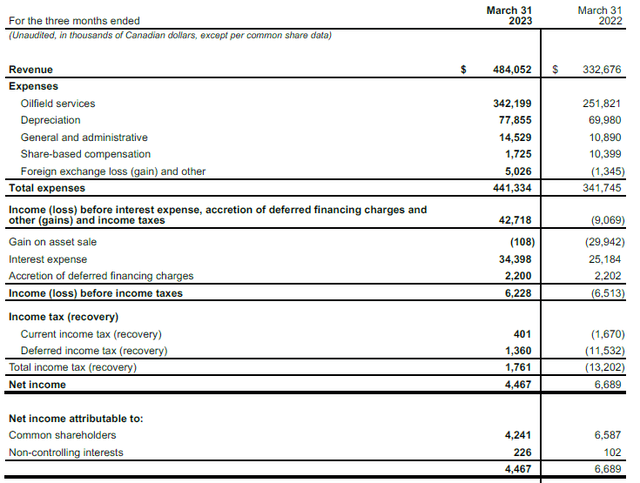

The company reported a total revenue of C$484M during the first quarter of the year, which is an increase of almost 50% compared to the C$333M generated in the first quarter of last year. The operating expenses obviously increased as well but the company was able to record an EBIT of C$42.7M which is a very substantial improvement from the negative EBIT of C$9.1M reported in the first quarter of 2022.

Ensign Investor Relations

That’s despite the FX loss of C$5M in Q1 2023 compared to a C$1.3M FX gain in the first quarter of last year.

Unfortunately Ensign had to deal with higher interest expenses (I will discuss the debt and interest situation in a separate section of this article) and the pre-tax income came in at just C$6.2M. That’s still better than the C$6.5M pre-tax income generated in the first quarter of last year, which was fueled by the aforementioned C$1.3M FX gain as well as a C$30M gain on an asset sale.

A noticeable improvement indeed, and the net income for the first quarter was approximately C$4.5M of which C$4.2M was attributable to the shareholders of Ensign Energy Services. As there are currently 183.9M shares outstanding as of the end of Q1, the EPS was C$0.02 (rounded down from C$0.023).

As most of my readers know by now, I’m an investor focusing on the cash flow a company is able to generate.

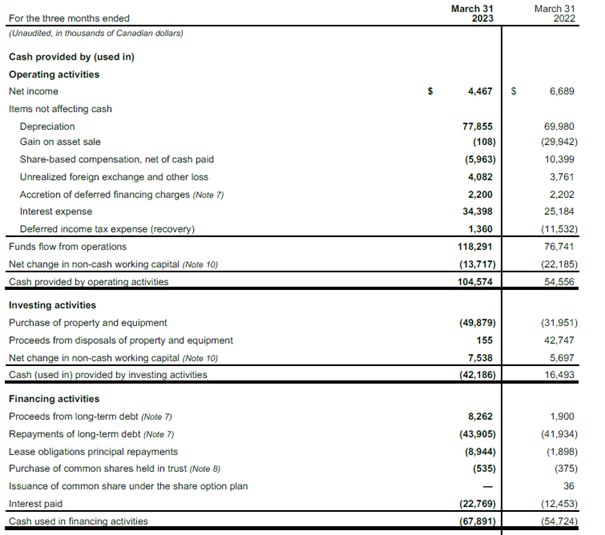

The total operating cash flow in the first quarter was C$118.3M before changes in the working capital position, but we still have to deduct the C$22.8M in interest payments and the C$8.9M in lease payments. This means that on an adjusted basis, and before changes in the working capital the operating cash flow was approximately C$86.6M.

Ensign Investor Relations

The total capex bill was C$49.9M which means the net free cash flow was almost C$37M or C$0.20 per share. That’s almost 10 times higher than the reported earnings and this is predominantly thanks to the difference between the depreciation and amortization expenses and the lease payments plus capex. Additionally, about C$6.3M in finance expenses (FX changes and deferred financing charges) were non-cash, and although those two elements had a negative impact on the pre-tax (and net) income, these are just accounting elements and had no impact on Ensign’s ability to generate positive free cash flow.

The interest expenses spiked as well

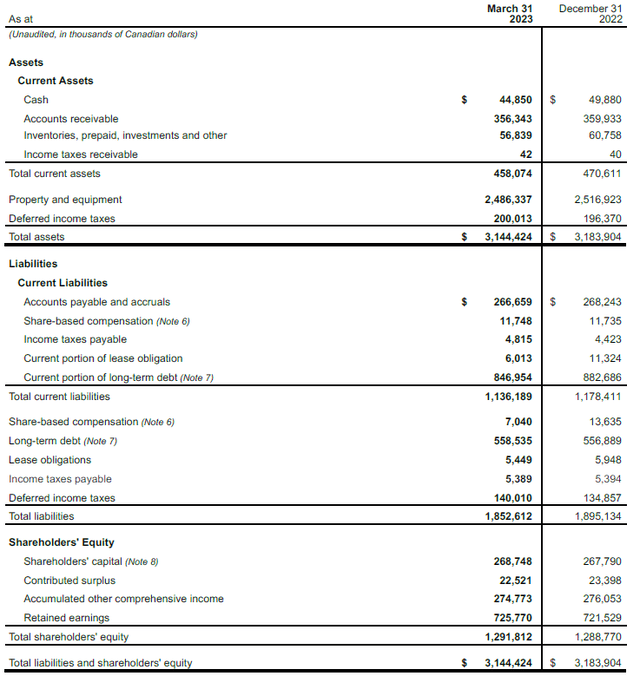

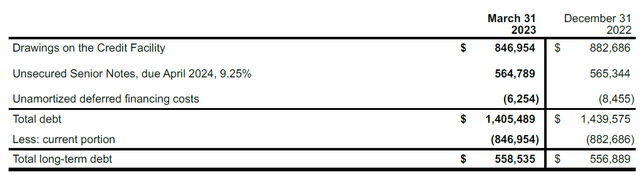

Ensign doesn’t pay a dividend and the company needs to keep a very close eye on its balance sheet and debt ratios. As of the end of the first quarter, Ensign Energy Services had about C$45M in cash but it had C$847M in near-term debt and an additional C$559M in long-term debt resulting in a net debt position of approximately C$1.36B.

Ensign Investor Relations

That’s rather high, and although the adjusted EBITDA in the first quarter of the year was C$127M (which means that on an annualized basis the debt ratio would be below 3), the current debt level is rather unsustainable. About two-thirds of the total EBITDA consists of depreciation and amortization expenses, and although the company’s capex level is currently tracking below the depreciation expenses, there eventually will have to be a “catch up” investment. Additionally, as we saw in the cash flow statement, almost 20% of the EBITDA had to be spent on interest payments.

Fortunately the majority of the debt has a fixed interest rate. Back in 2019, Ensign issued US$700M of senior notes with a 9.25% coupon. These senior notes are maturing in April 2024. And that’s what makes the balance sheet tricky. As those senior notes are maturing in April 2024, they are still classified as non-current on the Q1 balance sheet. However, they will move to the current debt designation in the balance sheet that will be published at the end of the current quarter.

Ensign Investor Relations

This means that – unless Ensign Energy Services is able to secure a comprehensive refinancing package – the balance sheet will contain C$1.4B in short-term debt.

Ensign Investor Relations

Investment thesis

The clock is ticking and the maturity date of the C$900M credit facility is “six months before the maturity date of the unsecured notes” which means the credit facility is expiring in October of this year. That’s in just five months from now and despite facing a difficult task, the company mentioned in its quarterly financial statements it has “not entered into formal discussions about the renewal and extension of its existing credit facility.”

And that’s the issue. Right now, the market is definitely doubting the company will be able to secure a refinancing deal at acceptable terms. Rather than buying the shares, the senior unsecured notes maturing in 2024 offer a better risk/reward ratio. Those bonds are currently trading at 97 cents on the dollar which means that if you believe in a positive outcome, buying the bonds would yield an absolute return of approximately 12% in just eleven months ( Double S Capital discussed these bonds in his recent article). While the unsecured notes rank junior to the credit facility, they obviously rank senior to the common equity and it’s easier to assume the creditors will be made whole than expecting the share price to double within the year. Of course, a 12% return is not great but it adds an additional layer of safety. I currently have no position in the common shares nor the bonds.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here