Thesis

We are in a different environment now, with interest rates and inflation much higher than a few months ago, and nobody really knows when or if low interest rates and low inflation will return in the near future. So it is always good to look at history as a guide to what might happen, and in a high inflation environment dividend paying stocks are a good place to be.

According to Fidelity, dividends are responsible for 54% of market returns during periods of high inflation, and stocks that increase their dividends outperform the market during these periods.

Therefore, fairly valued Dividend Aristocrats or Kings are an interesting long-term bet over the next 5+ years as they have a high potential for outperformance and Archer-Daniels-Midland (NYSE:ADM) is a high quality company with such a valuation. However, the question is whether their earnings growth in recent years is reliable, as the environment has favored ADM in recent years and things could change.

Analysis

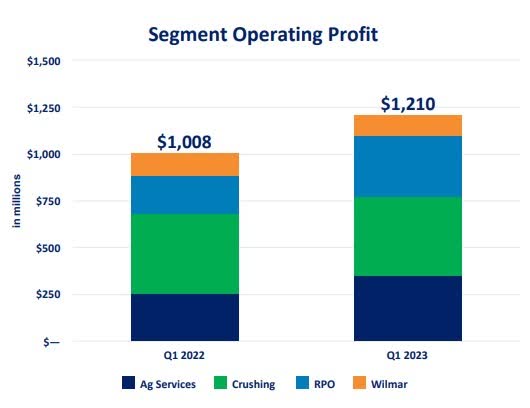

ADM Q1 Investor Presentation

ADM has once again posted strong results in its latest Q1 report. Its largest division, Ag Services & Oilseeds, showed a strong year-on-year improvement due to the record Brazilian harvest and strong soybean exports. In addition, there were record sales volumes in the biodiesel segment in North America.

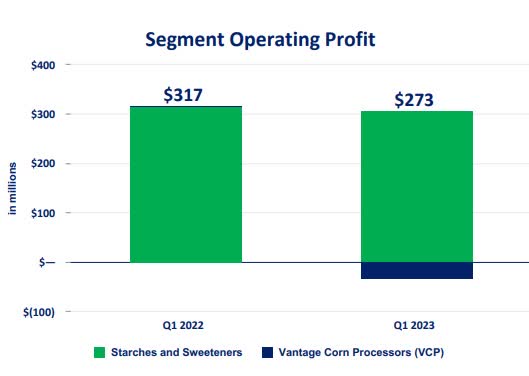

ADM Q1 Investor Presentation

The carbohydrates segment had to contend with some high inventory levels in the ethanol sector, which led to pressure on margins, and the segment’s performance was therefore worse than in the prior year.

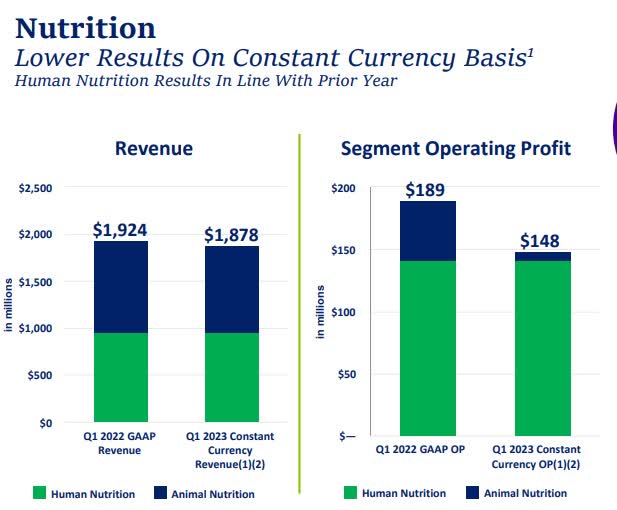

ADM Q1 Investor Presentation

The nutrition business also faced margin challenges as demand for amino acids in animal nutrition was challenging. However, the challenges in nutrition and carbohydrates are likely to be temporary.

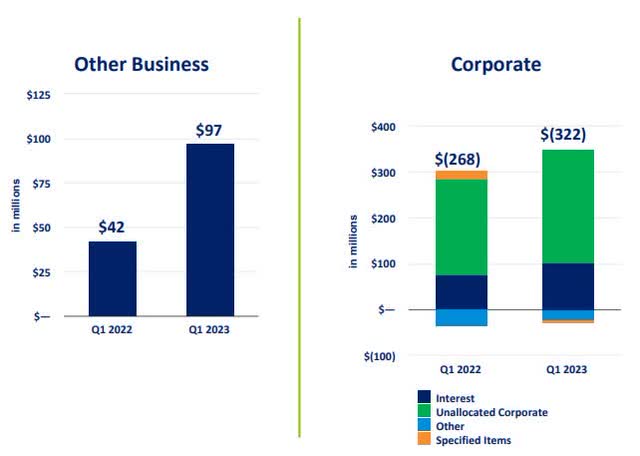

ADM Q1 Investor Presentation

The smallest segment, Other Businesses, benefited mainly from higher interest income. Overall, however, they see strong demand for biofuels and regional supply and demand constraints in some parts of the world.

Competitive Advantage

I think it could be argued that ADM and its peer Cargill, which many shareholders overlook because it is a private company, are the clear dominant players in this market. Because of their size, they have economies of scale and a lot of expertise, which is a strong barrier to entry. In my opinion, this is a big safety net because it limits competition.

Capital Allocation and Margins

ADM Q1 Investor Presentation

ROIC has improved dramatically over the last few years, from single digits to a strong average of 14% over the last four quarters. This really showed that management and a favorable environment were driving improved business metrics and making ADM a better company, as evidenced by more efficient use of capital.

Seeking Alpha Charting Tab

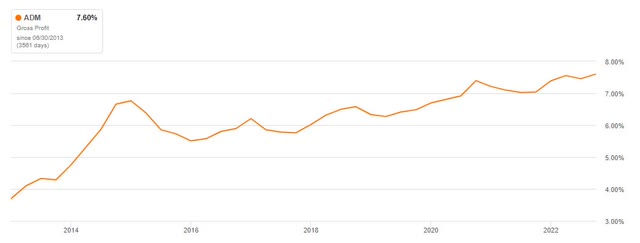

Gross profit margins have also been on a slow but steady upward trend over the past 10 years.

Seeking Alpha Charting Tab

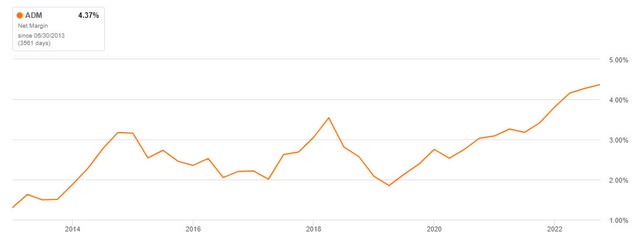

And the same trend can be seen in net income margins, although they are somewhat more volatile. All in all, ADM has dramatically improved sales over the past few years, while also increasing margins and ROIC, which really speaks to good management over the period and has resulted in ADM being a better company than it was before. Its balance sheet and net debt to EBITDA ratio of 1.2x also show that ADM is in a comfortable position.

Seeking Alpha Charting Tab

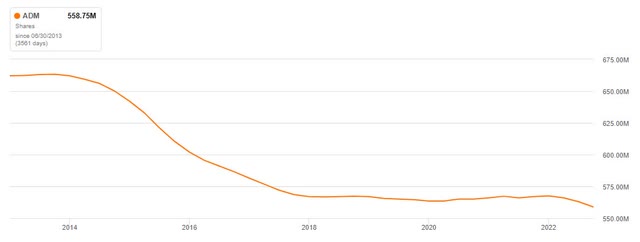

The declining number of shares outstanding and increasing dividends over the past 50 years also show that management is returning cash to shareholders.

Seeking Alpha Charting Tab

And the 11.99x EV/EBIT multiple shows that ADM is a bargain for the earnings you get for the price. Furthermore, it is well below the average multiple over the last 10 years.

Seeking Alpha Charting Tab

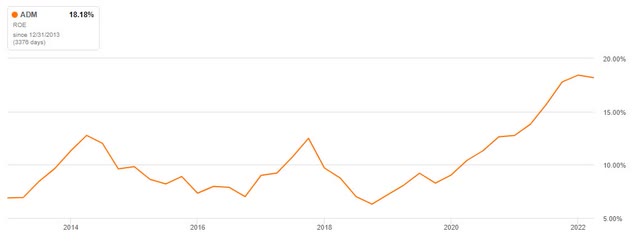

The ROE is now in an attractive range as it is close to 20%, but on a slight downward trend of late, and it will be interesting to see if they can maintain this level. If they can maintain this level, it would really improve the chances of success for shareholder returns.

Author

A reverse DCF analysis with TTM diluted EPS of $7.97 shows that 13% EPS growth is priced in over the next 5 years and then 7% over years 5 to 10. If we now look at the 5-year average of diluted EPS growth (YoY), we see that it was 28.83%, which is well above the current price. This also suggests that the share price is probably undervalued. However, the 5-year average is a bit high because sales really exploded in that period and that kind of distorts the average and the likelihood is that it will be lower in the next 5 years.

Growth Opportunities

The rebound in demand in China, the trend towards renewable energies and the focus on innovation to improve productivity and achieve savings are positive for future growth. However, ADM is in a somewhat cyclical industry and the current environment has favored its top line growth, which may slow in the future and therefore the margin and capital efficiency improvements may only be temporary. Cyclical improvements often mislead investors into believing that this is the new state of things and they are therefore sometimes led into a value trap.

Nevertheless, I see no slowdown at the moment and ADM is clearly investing in the future with its venture capital and other commitments. They opened the first probiotic and postbiotic production facility in Valencia, Spain, which increased their global production capacity fivefold.

The situation in Argentina, which will likely run out of beans in May or June, and the situation in Ukraine, with its black, rich soil, are a bit of a challenge, but hopefully temporary and short-lived.

Conclusion

ADM is currently a cheap, high-quality company that has significantly improved its capital allocation over the past few years. And over the long term, it is very likely to match the total return of the S&P 500, with small deviations. Periods of weakness could be used to buy dips to enhance returns, which is usually the right strategy for cyclical industries.

But the challenge now is when will earnings come back down, or will they stay this high for longer? Nevertheless, ADM is a good inflation and long-term play, with a strong market position and likely years of dividend growth ahead.

Read the full article here