Dear readers/followers,

In February, I came with a slightly controversial HOLD rating for Ally Financial (NYSE:ALLY). I say controversial, because at the time the general sentiment was relatively bullish. Not only that, but at $30 per share, Ally seemed relatively fairly priced and with management guiding towards a sharp (50%) rebound in earnings in 2024, it wasn’t difficult to calculate potential upside. Still, I didn’t buy and decided to wait, because things were clearly deteriorating in Q4 as seen by the drop in net interest margin (NII) and an increase in net charge offs. I also mentioned that auto loans usually underperform during a crisis and since we had been talking about a potential crisis for a while, the risk/reward simply wasn’t worth it for me.

Seeking Alpha

Since then several banks have collapsed, so we could say that we’ve had a small crisis, at least in Financials. The price unsurprisingly responded by a 17% drop, while the S&P 500 climbed by 3%. That’s clear underperformance, but now that the price is lower and the company reported their Q1 earnings recently, it’s time for an update to determine whether it’s time to jump in.

Overview

First let’s start with a quick recap of their business. Ally is an online bank which has become quite popular especially with the younger demographic. This gives them a major advantage because with no physical branches they reduce their overhead significantly (no rent and less staff). As any bank, they rely on deposits from their customers for funding, pay depositors interest and then try to redeploy the capital by providing loans at a higher interest. In case of Ally, the majority of these loan are auto loans provided to retail as well as dealerships. In addition to auto loans they also provide corporate financing, mortgage, credit cards and insurance solutions.

Deposits

Since this is a fairly simple business, there are only a handful of variables to consider here. Let’s start with the banking division and the depositors in particular. With the recent banking crisis, many banks struggled with an outflow of deposits as people moved their capital from riskier regional banks into larger (and hopefully safer) ones. No bank can withstand a bank run, unless it gets liquidity from the Fed and although the Fed has said that it is ready to help banks if they need it, I only consider investing into banks that clearly show that they still have customers trust. This gives me peace of mind as it reduces the chance of a bank run. Ally in particular has done quite well. In Q1 they added 126 thousand new customers which was the highest quarterly increase since 2009, their total deposits grew by $813 Million to nearly $140 Billion and their client retention stood at 96%. This clearly shows depositors trust the bank. Moreover, with 91% of retail deposits FDIC insured, the risk of a bank run isn’t too high. Liquidity is also high and able to cover 3.6x uninsured deposits.

Revenue drivers

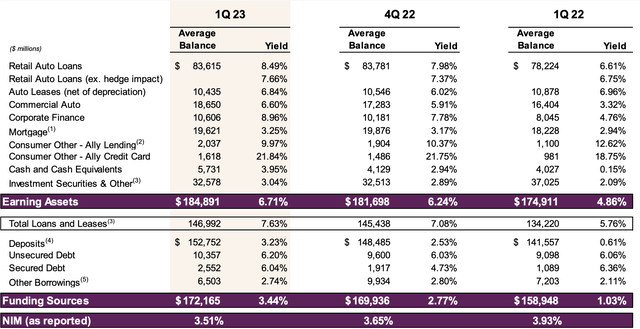

Beyond deposits the most important driver of results for Ally is the spread they earn on their loans vs what they pay their depositors, this is called net interest income (NII). As you can imagine, in a high interest rate environment, depositors demand a higher interest on their balance, but the bank is also able to charge higher interest on their loans (mostly the new ones). The spread shrinks when the rate on deposits increases faster than on the loans and that’s exactly what has been happening to Ally which saw their NII fall from 3.93% in Q1 2022 to 3.51% in Q1 2023. A fall of 42 bps may not seem significant, but keep in mind that this is the single most important driver of earnings and though it may not seem like much it represents a nearly 11% drop in the spread they earn.

Ally Presentation

For 2023, assuming fed funds rate peaks at 5.25%, management expects NII to average 3.5% – essentially forecasting no further decline. The company has also added significant hedges to protect against higher for longer scenarios. Beyond this year, management forecast a return of NII back to 4%. I think this is definitely achievable if rates stabilize or drop.

Ally Presentation

Risks

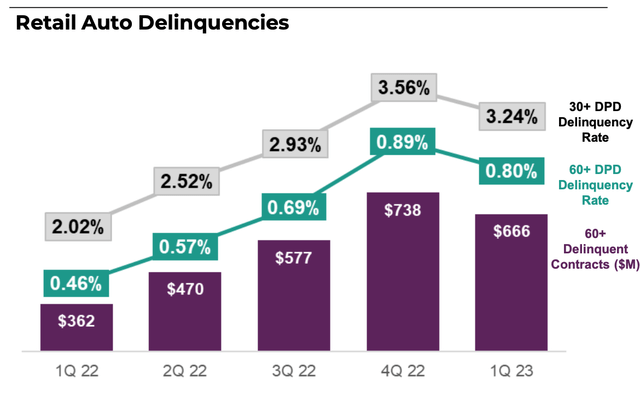

Another key piece of the puzzle we need to talk about is loan defaults. Being able to charge higher rates on loan is great (estimated originated yield on new auto loans average almost 11% in Q1 2023), but we have to remember that there’s someone on the other side paying this interest. With an economic slowdown and high payments, it’s more likely that the borrower won’t be able to pay. This represents a major risk for Ally. We saw a sharp increase in Net charge-offs (NCOs) in Q4 and this continued into Q1 2023 with total NCOs of $409 Million. The vast majority of this ($351 Million) came from auto loans where annualized NCO rate remained elevated at 1.68%. For comparison, prior to Q2 2022 NCOs were about a third. This is of course in large part driven by retail auto delinquencies that have climbed pretty steadily throughout 2022 as the economic situation got worse and interest rates increased. In Q1 2023, delinquencies actually dropped QoQ, but remained elevated.

Ally Presentation

Of course, some level of defaults is expected which is why Ally has a credit loss reserve of $3.8 Billion of which $3.0 Billion is set aside for auto loans alone. This massive reserve accounts for 3.6% of all auto loans and 2.74%. With net charge-offs at today’s levels, the reserve is large enough to cover almost 10 quarters of elevated defaults.

Guidance

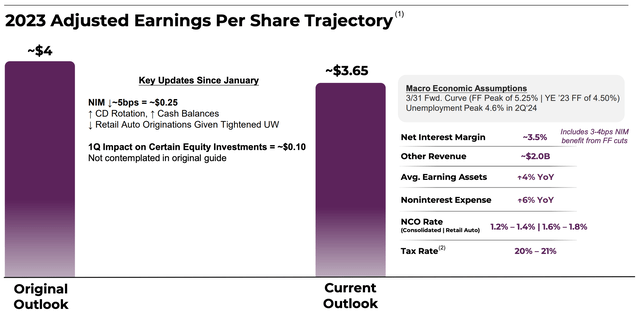

In lights of Q1 results, management gas reduced their full year EPS guidance from $4 to $3.65 per share. Notably they also removed their previously stated target EPS for 2024 of $6 per share (which many analysts used for their valuation) and simply stated that they “continue to project EPS expansion throughout 2024 – pace dependent on rates, liquidity & capital levels, and origination strategy”. On the earnings call they said:

no one should take the removal of the outer period outlook as a fundamental shift in guidance. The Company will migrate toward that $6 per share outlook, but obviously, several moving pieces at the moment may impact the pace in which we get there.

To me it feels as though they feel they were too optimistic in their guidance and it’s definitely not a good sign.

Ally Presentation

Valuation

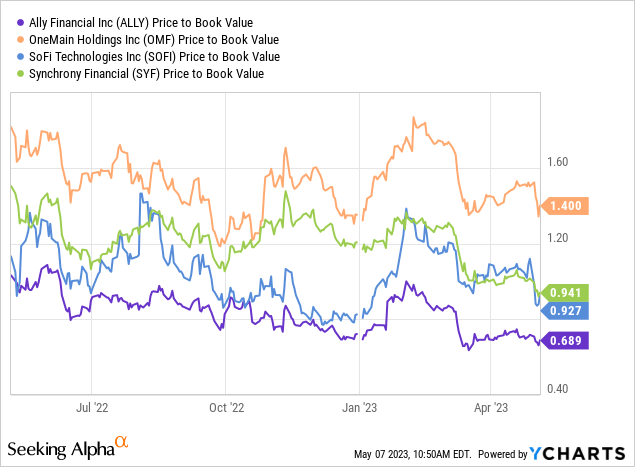

Ally now trades at 0.69x book value (significantly below peers) and at 7.2x their 2023 expected earnings of $3.65 per share. It’s worth noting that these are most likely their through earnings and historically they have traded closer to a P/E of 9x. With all of this I do feel that ALLY is entering undervalued territory here. Add to that their $0.30 per share quarterly dividend (4.6% yield) and the stock starts to make sense as an investment. That’s why I will join Mr. Buffet who owns a 10% stake in the company and issue a “BUY” rating for ALLY here at $25.30 per share. I will start building the position slowly though, as I do believe that the road to recovery will be fairly bumpy and if the economic situation worsens, Ally will have to deal with significantly higher net charge offs which will send the stock price lower. My plan is as follows.

- Start a small position here – 25% of target allocation.

- I also sold some June $24 puts in early March (see comment on original article) for another 25% of target allocation.

- I will invest the remaining 50% around $22 per share if the price ever gets there

Read the full article here