Investment action

Based on my outlook and analysis of SharkNinja (NYSE:SN) business and valuation, I recommend a hold rating. I think SN has a pretty good business, honestly, it’s just that the stock is not cheap enough yet-the stock is trading at 19x LTM earnings when peer (Whirlpool Corp. (WHR)) trades at high single digits.

Basic info

SN provides consumers with innovative, high-quality products that improve their quality of life. They have a presence across a wide range of consumer product categories, including those related to cleaning, cooking, food preparation, the home, and beauty.

Speed to market is key to meeting consumers’ everchanging preferences

SN has always placed emphasis and focus on bringing disruptive innovations to market first. Being the first to market is a big competitive advantage, as they can gain market share in that segment quickly without much competition. The head start also provides SN with a dominant presence in consumers’ minds, associating the segment with SharkNinja’s brand when they think of the product in the future. This is important because it also means that consumers are well exposed to the SN brand and know that their product works. The next time SN innovates a new product, consumers will be more willing to try it. Such a strategy works extremely well in the market they operate in, as new product innovation in household product categories often drives excitement and hype among consumers, which leads to word-of-mouth marketing and brand awareness.

In order to facilitate this speedy execution, the real competitive advantage is SN’s ability to tap into their global consumer insights. This gives them the ability to identify common problems and create ground-breaking products to address them. Specifically, they have a team of designers and engineers around the world. With a global team that is equipped with different geographical expertise, they can design products that meet the requirements of many different geographical regions into one product or create different products that meet the different requirements. This gives their product a competitive advantage that smaller-scale players are unable to achieve.

In addition, as part of their “always-on” strategy, they analyze how customers use their appliances and listen to feedback from customers on various channels. With that motto and strategy, they are rapidly iterating and continuously refining their products, and thus, they can increase the value of their existing offerings while decreasing costs. Their products have longer life cycles, which sets them apart from rivals.

Overall, I believe SN’s strategy has allowed them to quickly become leading players in both established and emerging product categories by bringing more new products at competitive prices to the market (more below), thus separating them from their traditional rivals, who only introduce new products every few years.

Presence in multiple product segments improves CLTV/CAC

In addition to speed, SN has a wide variety of products in 27 distinct categories for the home, such as cleaning, cooking, food preparation, etc., which include categories like “home environment” and “beauty.” By providing such a variety of products, they offer consumers a one-stop solution to all their household needs. With that, customers do not have to go to different brands to source the individual household products they are looking for. Also, from a consumer perspective, it is a lot easier to purchase everything from one vendor or store, as I would only need to deal with one customer support representative in the future.

If we look at this from a return-on-customer-acquisition-cost perspective, it makes a lot of sense. For example, SN spends $x to acquire the customer lead for the purchase of a vacuum cleaner, but the customer also ends up purchasing other items like air purifiers, carpet cleaners, blenders, coffee machines, etc. Overall, the ROI becomes a lot higher.

Offering products at affordable rate is key

Lastly, SN products are priced at an affordable rate. They have built a highly efficient, globally based product design and supply chain with one goal in mind: providing customers with the best possible product at an attractive price. This is made possible by their design and manufacturing teams, as well as their local procuring organization in Asia, which organizes a bidding process amongst multiple manufacturers to ensure they receive the most competitive prices. In addition, many of their manufacturers rely heavily on them as partners due to the prominence of their brands; as such, I believe SN has high bargaining power to negotiate for lower prices. This can be seen from its financials, where SN had a 47% gross margin in 1Q23 while peers like WHR and Arhaus (ARHS) had lower margins. This strength is exceptionally strong in the current high inflationary environment, where consumers’ discretionary income is not matching up with inflation. By offering consumers a product that serves multiple innovative functions at accessible prices, they can effectively gain market share from other smaller players who are unable to compete in pricing.

Valuation

Finmasters

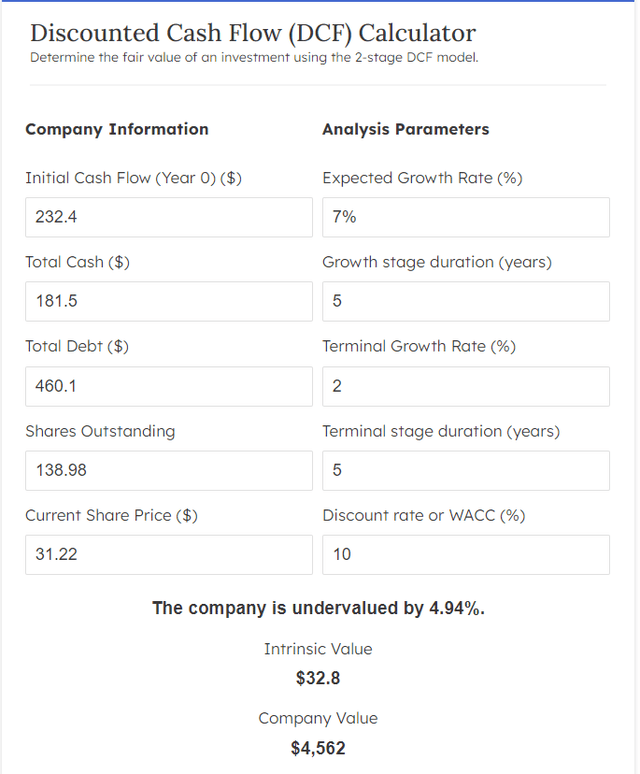

Note that my DCF model uses earnings as a proxy for cash flow.

I believe SN can grow earnings at a similar pace to the industry. According to Grand View Research, the US Household appliance market is expected to grow at 6.7% from 2023 to 2030. I note that this is not totally comprehensive of the SN market as it also has exposure to China (17%) and the rest of the world (4.5%), but this is a good enough benchmark as the US is 80% of the SN revenue base. Over the course of 10 years, I expect SN to reach full maturity (the industry is largely mature as well) and grow at a terminal rate of 2%, reflecting long-term inflation rates. At a 10% discount rate, I believe the stock is fairly valued today.

Risk and final thoughts

A large part of SN’s ability to win market share and grow is through innovation. While they have a strong global team to gain insights that sub-scale players are unable to, there is no guarantee that SN will be right all the time. A persistent “miss” in identifying the next trend could lead to a devaluation in brand equity value, which impacts SN’s financials.

In conclusion, considering SN business dynamics and valuation metrics, I recommend a hold rating. Despite the company’s robust position in various consumer product categories and its strategic emphasis on innovation and speed to market, the current stock valuation remains a concern.

Read the full article here