Investment Thesis

PayPal (NASDAQ:PYPL) has been a challenging investment over the past several years.

The stock is down significantly from its highs and its CEO is stepping down and leaving a new CEO in place to pick up the reigns and to try to turn around this business. This is the narrative that overwhelms PayPal. And there’s little to distract investors away from these dynamics.

However, I argue that these considerations and a lot more are already in the share price. After all, investors only get a value investment, when the outlook is poor. There’s no other reason why a stock would sell cheaply, apart from the outlook being grim.

I declare that everyone already knows all these characteristics. And those insights are already in the share price. I stand by bullish contention, that paying 11x next year’s EPS for PayPal is a mighty compelling investment opportunity.

The Outlook of a Mature Business

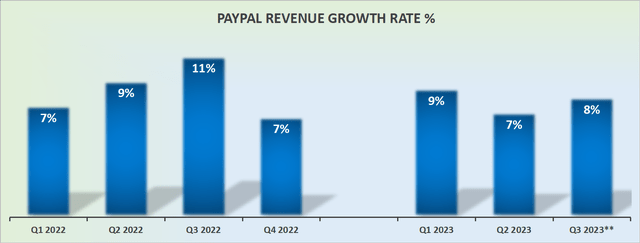

PYPL revenue growth rates

The graphic above is a reminder that PayPal’s growth rates have matured. This is no longer a rapidly growing company, that can be counted on to deliver premium growth rates, meaning +20% CAGR.

That being said, there’s a lot to be said about a company that has reached maturity. The business will no longer strive to seek to expand its market share aggressively. It can deploy extra resources towards maximizing profitability and, in the not-too-distant future, returning capital to shareholders.

Here’s a quote from the earnings call that reflects this argument,

As we look ahead to the rest of 2023 and into 2024, we expect to drive meaningful productivity improvements. Our initial experiences with AI and continuing advances in our processes, infrastructure and product quality, enable us to see a future where we do things better, faster and cheaper. These overall cost savings come even as we significantly invest against our three strategic priorities.

With this context in mind, let’s turn our focus toward PayPal’s underlying profitability.

Profits Shining Brightly

PayPal reaffirmed that it can deliver $4.95 of non-GAAP this year.

In my previous analysis, I said,

If we assume that PayPal’s profitability slows down [in 2024] and its EPS only grows by 18% y/y compared with the 21% y/y EPS growth expected for this year, this would mean that PayPal’s 2024 non-GAAP EPS could reach nearly $6 of non-GAAP EPS.

I stand by those assertions. I continue to believe, as I did previously, that PayPal can deliver $6 of non-GAAP EPS in 2024.

What’s more, given that PayPal is clearly so profitable with strong cash flow conversion, PayPal is able to support its EPS profile through large share repurchase programs.

Indeed, we know that in 2023, PayPal will have returned the equivalent of an approximate 6% buyback yield to shareholders. And if PayPal were to return a similar $5 billion of free cash flow to shareholders next year, this would perhaps even support PayPal reporting higher than $6 of non-GAAP in 2024.

PYPL Stock Valuation — 11x Next Year’s EPS

PayPal isn’t quite as cheap as when I wrote my previous analysis titled, PayPal: 10x EPS, Period. However, for all intents and purposes, it’s still in the bargain basement.

Of course, the bull case isn’t one without blemishes. After all, as we’ve already discussed, PayPal is no longer growing at a particularly fast rate. The business now operates ex-growth.

And for a business that has decidedly become ex-growth, that means that its shareholder base must rotate out. The shareholders that become interested in PayPal as a rapidly growing company will come to terms that those fast-growth days are gone. And a new group of investors will come in that will put tremendous focus on PayPal’s underlying profitability practically to the exclusion of all other considerations, including its underlying narrative.

Furthermore, PayPal has on numerous occasions in the past 2 years had a proclivity to be too aggressive with its outlook only to later have to downwards revise its original guidance. Investors will be acutely aware of this dynamic, and request a large margin of safety.

But even on the back of all those considerations, I believe that paying 11x for EPS for a business that is clearly growing its bottom line in the very high teens makes sense.

The Bottom Line

In my analysis of PayPal, I acknowledge that the company has faced challenges in recent years, with the stock price declining and a change in CEO.

However, I argue that these factors are already priced into the stock. As a mature business, PayPal is no longer experiencing rapid growth, but it has the opportunity to focus on maximizing profitability and returning capital to shareholders.

Further, I believe PayPal can achieve around $6 of non-GAAP EPS in 2024.

With a valuation of around 11x next year’s EPS, I see PayPal as a compelling opportunity for investors, especially considering its strong profitability.

While there are some concerns, such as past aggressive guidance revisions and a shift in the shareholder base, I maintain my bullish stance on the stock due to its attractive valuation and profit growth potential.

Read the full article here