By Brian Nelson, CFA

Everything is relative when it comes to sovereign health. The strength of a sovereign rests in part on its capacity and willingness to continue to pay its debts and meet its future expected liabilities. To do so, sovereigns often may need to “print money” at times to manage the budgetary cycle. The drawback of “printing money,” however, is the risk of inflation and resulting weakness in their currency.

If a sovereign’s currency remains strong relative to a basket of other currencies, however, there may be little risk that the sovereign will not meet its future expected liabilities. After all, the sovereign can keep “printing money” to meet such liabilities as they come due and generate little impact on the health of its currency–and little change to the purchasing power of its currency on the world stage.

To a large degree, this “money printing” then becomes net-neutral. Though there may be much that goes into assessing the credit health of a sovereign, from our perspective, it generally boils down to the view that the stronger a sovereign’s currency relative to other currencies, the negligible impact that “printing money” to meet debts will have–and therefore, the stronger its credit rating should be.

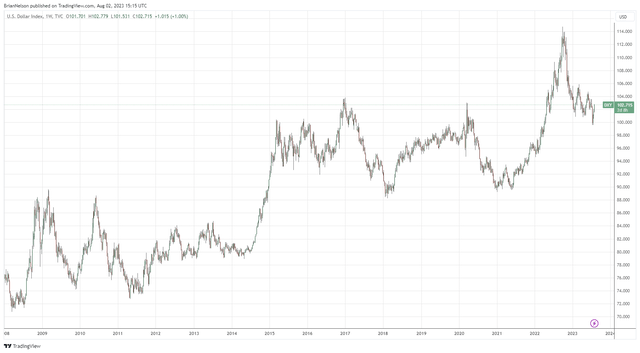

The U.S. Dollar Index has strengthened considerably since the Great Financial Crisis. (Trading View)

On August 1, Fitch downgraded the credit rating of the U.S. one notch to AA+. Here is the rationale:

The rating downgrade of the United States reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions.

The strength of the U.S. dollar, however, is undeniable and remains a safe haven, in our view (see image above). One only has to think back a few months when many market participants were traveling the world using strong U.S. dollars to purchase foreign goods and leisure on the cheap. For a sovereign to experience weakening financial health, we would expect that to manifest itself in a weakening currency as investor assets flee the country seeking other currencies, but the U.S. remains the place to be when it comes to the global stage. Quite simply, U.S. equity returns, as measured by the market-cap weighted S&P 500 (SPY), have dominated the global stage, and we don’t expect that to change anytime soon.

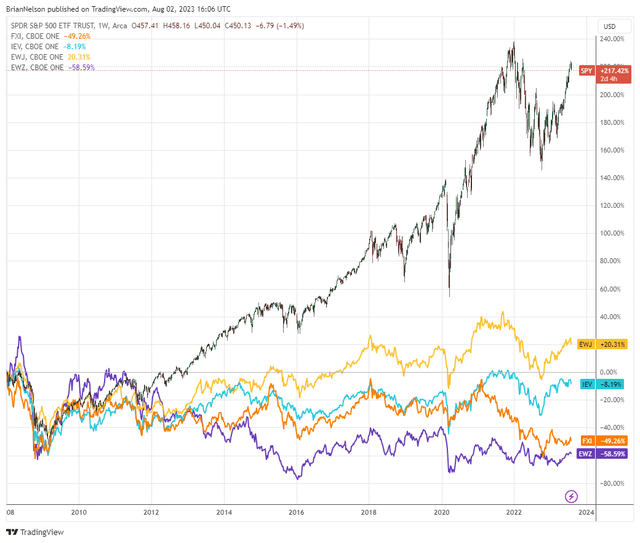

The U.S. markets (top) have trounced European, Chinese, Japanese, and Brazilian equities since the Great Financial Crisis. (Trading View)

Though many believe gold (GLD) and Bitcoin (BITO) may be viable alternatives to the U.S. dollar, both gold and Bitcoin lack what’s needed in a dependable currency. For one, you can’t buy groceries at the local supermarket with gold, and businesses generally don’t accept cryptocurrencies for payment given their volatility and the uncertainty surrounding the SEC’s crackdown on many of them as securities. Gold and Bitcoin also don’t generate future expected free cash flows, so estimating their intrinsic values becomes a very difficult proposition. In many respects, both gold and Bitcoin are “greater fool” assets as most own them for price appreciation (diversification) potential, not to conduct business. Their prices are then more a reflection of what somebody else will pay for them than anything else. A stock, on the other hand, is unique.

Unlike other investments such as classical art, fine wine, or vintage baseball cards, for example, stocks represent a claim on all the assets of the company, particularly their future enterprise free cash flows. Whereas the prices of a rare Picasso, the best Bordeaux money can buy, or an authentic, gem-mint Cracker Jack “Shoeless” Joe Jackson may be almost entirely based on what someone else will pay for them, stocks are different, and it is in this difference that enterprise valuation is distinguished from speculative, illogical frenzy. Stocks can actually have intrinsic monetary value, in addition to what someone will pay to take it off your hands.

Now that is not to say that intrinsic value estimation is not part art and part science–both arguably of equal importance–but it is the very idea that a share of stock is not just a piece of canvas or cardboard or a fermented grape that very much matters. For one, a fine Picasso cannot intrinsically generate enterprise free cash flows, a Bordeaux cannot either, nor can one of the most sought-after treasures of the 1914/1915 Cracker Jack baseball card collection. Because a stock is an ownership claim on a company’s assets (and, by definition, those very assets’ future enterprise free cash flow stream), a stock has tangible monetary value, regardless of one’s opinion of the company.

In the case of stocks, intrinsic value–not to be confused with price–is therefore not always in the eye of the beholder. A dollar of enterprise free cash flow generated by the company rightly belongs to the shareholders, and it is because of this that stocks are not, in substance, just pieces of paper, even as this truism may be obscured during manias or in times of panic, when ranks of the greedy or fearful grow, respectively. Rather, stocks have intrinsic, monetary and foundational worth. Stocks generate cash (i.e. free cash flow), and this is a huge difference between them and other investments that do not (source: Value Trap, used with permission).

As we think about Fitch’s downgrade of the credit rating of the U.S., we don’t necessarily disagree that the ability of the U.S. to pay its debts has become more convoluted given rising future expected liabilities, a higher interest rate on those liabilities (given rate hikes), and uncertainty about the willingness to meet its debts in light of the seemingly never-ending debt ceiling debates that have gone to the deadline. We understand that there’s more risk today than before, but investors shouldn’t worry about a very, very modest increase in an assessed probability of the U.S. technically defaulting on its debt. The rating of a AA+ is actually a very good one, and the difference between a AAA and AA+ is quite negligible in the grand scheme of things.

For us, we think the AAA rating that should be downgraded is actually a corporate in the form of Johnson & Johnson (JNJ). The company holds a net debt position, has uncertain talc liabilities, as well as complications regarding its split-off of Kenvue (KVUE). How the U.S. can now have a AA+ rating while J&J can continue to sport a AAA rating speaks to the subjectivity of credit ratings, themselves. AAA-rated companies should fit the bill more like a Microsoft (MSFT), which has AAA corporate credit rating thanks in part to its huge net cash position and tremendous free cash flow generating ability–two of the most important sources of cash-based intrinsic value. Rating sovereigns and rating corporates are two different things, of course, but the rating, itself, generally measures probability of default. J&J’s probability of technical default is bigger than that of the U.S., in our view.

Though Fitch’s downgrade of the credit rating of the U.S. to AA+ may, in many ways, be warranted, as equity investors it’s important to keep it all in context. What a AA+ rating means relative to a AAA rating is that there is only a minor–perhaps miniscule–higher assessed likelihood of a technical default of the debts of the U.S. over the long haul. However, a look at the strength of the U.S. dollar since the Great Financial Crisis speaks of a sovereign that perhaps has grown stronger on the world stage, not weaker. Remember, sovereign credit health is all relative, and unless there may be a country with a strong democratic legal system that emerges stronger and larger than that of the U.S. whereupon the U.S. dollar is sold in droves, there is very little risk in the long run of a technical default by the U.S.–as it can just keep “printing money.” With that said, we don’t disagree with Fitch’s rating move–we just want long-term equity investors to keep it in context.

The U.S. equity markets will likely need to take a breather after experiencing a huge run higher so far in 2023, and Fitch’s downgrade probably gives a reason for some profit taking, but we think the sell-off will be short-lived. The two areas that have dominated returns year-to-date remain big cap tech and large cap growth, and we expect these areas to continue to perform well. Stocks in these areas tend to have fantastic sources of cash-based intrinsic value, including large net cash positions on the balance sheet and strong expectations of free cash flow generation. If the markets are at all concerned about the credit health of the U.S.–and reverberations in the credit markets–the areas of big cap tech and large cap growth are safe havens. Many in these areas can continue to run their businesses effectively, even if the equity and credit markets were to close for years thanks to tremendous balance sheets and considerable free cash flow generation.

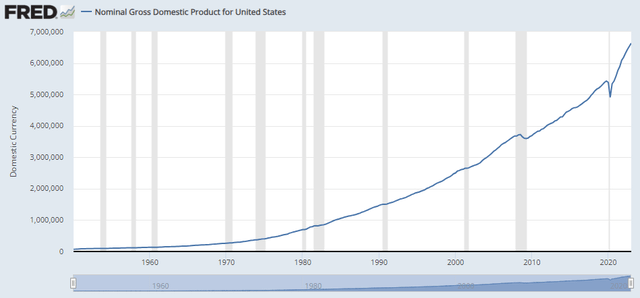

Nominal U.S. GDP continues to surge. (International Monetary Fund, Nominal Gross Domestic Product for United States [NGDPSAXDCUSQ], retrieved from FRED, Federal Reserve Bank of St. Louis)

We recently wrote an article about how investors may be thinking about the P/E ratio and other valuation multiples incorrectly, as the asset-light nature of many of the market leaders today from Apple (AAPL) to Alphabet (GOOG) (GOOGL) to Microsoft and beyond warrant higher-than-typical valuation multiples than in the past, especially in light of their huge net cash positions on the balance sheet. Net cash is an add-back to the present value of estimated future free cash flows in the enterprise valuation context, so we generally prefer equities with net cash positions over those with net debt positions. We also continue to like what the catalyst of artificial intelligence means for future free cash flow generation of big cap tech and large cap growth in coming years, while nominal GDP in the U.S. continues to boom higher (as shown in the image above). We don’t think Fitch’s downgrade of the credit health of the U.S. will derail this bull market, and we point to five of our favorite ideas to consider in this article.

Read the full article here