Essential Utilities (NYSE:WTRG) provides water, wastewater and natural gas services in the United States. The company’s operations are what I’d call recession-proof as water is a core necessity. Although the company has a low risk profile, I believe the company’s valuation is currently way too high as the company has troubles in converting its accounting earnings into free cash flow. For this reason, I have a strong sell-rating for the stock.

The Company & Its Financials

Essential Utilities’ operations are as the name suggests – they provide essential infrastructure related to providing water. The company also holds “Peoples”, a company that replaces natural gas pipelines in the United States, that the company acquired in 2020. The company has a long history as Essential Utilities was founded back in 1886.

The company has had a modest growth rate of 6.2% from 2002 to 2019 – in 2020, the company completed the acquisition of Peoples worth over $3.4 billion in costs for the year, boosting its growth temporarily. Analysts expect the company’s growth to come down from 2020-2022 highs into figures that are in line with the company’s history – I believe this is a reasonable belief, as in Q1, the company’s growth was 3.9%, roughly in line with the company’s history.

Essential Utilities has a very strong operating margin that has historically been around 40%. With the company’s acquisition in 2020, their operating margin fell significantly to around 30%:

Currently, the company’s trailing operating margin stands at 28.7%. I don’t currently see any signs of an improving margin, although analysts currently expect a jump into historical figures as consensus estimates point at a 39% margin for 2027.

Essential Utilities has a low cash balance of $20 million, and outstanding interest-bearing debts of $6726 million, of which almost all is in long-term debt.

Weak Cash Flows

Essential Utilities has very weak cash flows as the company needs to continuously invest into its operations and acquires growth non-organically through acquisitions of communities to expand the footprint of Aqua’s pipelines. Essential Utilities has financed its operations a lot through share offerings – for example in 2020, the company raised approximately $311 million through an offering. Shareholders have seen a large dilution in their holdings, as the company’s outstanding share count has jumped from around 177 million in 2013 to the current number of over 263 million.

In addition, to finance the company’s historical modest growth, the company constantly acquires assets to expand its operations. Some examples of this include the purchase of the Union Rome Sewer system in July 10th for $25.5 million and a wastewater system purchase of $18 million expected to be completed in Q1/24, announced in May. Essential Utilities’ cash acquisitions are constant and bleed significant amounts of cash flow from investors:

The Company’s Acquisition History (Seeking Alpha)

These factors contribute to the fact that Essential Utilities has very weak cash flows compared to its accounting earnings. To add to the previous inconveniences, the company has strong needs in capital expenditures – in the last twelve months the company’s CapEx stands at $1188 million, when the company’s D&A is only at $327 million.

Valuation

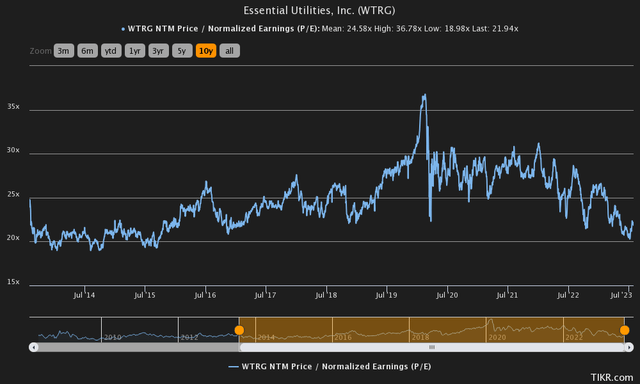

Essential Utilities’ NTM price-to-earnings ratio is at 21.94, around its historical figure:

The Company’s Historical P/E (Tikr)

This is a relatively high figure, but as the company has arguably recession-proof revenues, it could be understood. As the company converts its earnings so poorly into free cash flow, a discounted cash flow model reveals the ugly truth about the company’s valuation.

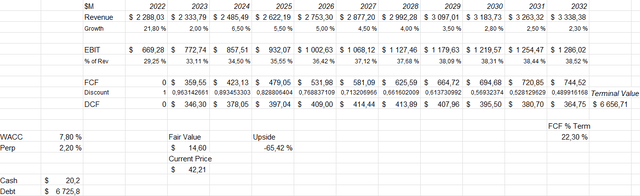

In the DCF model estimates, I have a 2% growth for the current year, with the growth speeding up in 2024 to a 6.5% rate, where it slowly declines into a rate of around 2%. I believe these are fair estimates, as they are quite in line with the company’s past performance.

I estimate the company’s EBIT margin to come back up from the current figure into a margin of 38.52% in 2032 – this is a rise that analysts expect, but I don’t currently see a very strong foundation for the claim; the acquisition of Peoples was done in 2020 weakening the company’s margins, and possible synergies and improved efficiencies should already have materialized by a good amount, but the company’s EBIT margin keeps on falling. A possible explanation could be that current inflation tampers the company’s margins temporarily, but the company should overcome the inflation with time, improving margins.

As explained in the previous paragraph, Essential Utilities converts its accounting earnings poorly into free cash flow – their cash flows have been negative for several years. In my estimates, I give the benefit of doubt in future estimates, as I estimate cash flows to be positive even with moderate growth. This would essentially imply that the company can significantly decrease their capital expenditure levels going forward.

These expectations create an estimated fair value of $14.60 for the stock, a -65% downside from the current price of $42.21:

DCF Model of the Company (Author’s Calculation)

The low weighed average cost of capital I used is derived from a capital asset pricing model:

CAPM of the Company (Author’s Calculation)

The company had interest expenses of $72.7 million in Q1. With a debt balance of $6726 million, this represents around a 4.3% interest rate, which I used in the model. I believe the company’s long-term debt-to-equity ratio should be around 20% – a lower figure than currently, as the company begins to pay out debts taken to finance the acquisition in 2020.

I use the United States’ 10-year bond yield of 3.94% as the risk-free rate. The equity risk premium is Professor Aswath Damodaran’s estimate. Yahoo Finance estimates the company’s beta to be 0.76. Finally, I add a 0.5% liquidity premium to the cost of equity. This crafts a cost of equity of 8.93% and a WACC of 7.8%.

Takeaway

Unless I missed a significant piece of information in my research process, I think Essential Utilities seems like a bad investment. The company bleeds cash flow to achieve modest growth, and as the company gives out dividends it constantly dilutes its outstanding shares. Although the company’s operations have a very low risk profile, the low cash flows weigh in on my evaluation. At $42.21, I have a strong sell rating for the stock.

Read the full article here