Investment thesis

Our current investment thesis is:

- There are various data points that suggest a weakness in BLMN’s competitive positioning, with superior peers and net restaurant closures.

- Offsetting this partially is international expansion and margin improvement, allowing for a resilient performance during uncertain market conditions.

- Relative to peers, BLMN materially underperforms, with lower growth and margins. Based on this and the commercial concerns, we consider the stock a hold.

Company description

Bloomin’ Brands (NASDAQ:BLMN) is a leading casual dining restaurant company that owns and operates a portfolio of well-known brands, including Outback Steakhouse, Carrabba’s Italian Grill, Bonefish Grill, and Fleming’s Prime Steakhouse & Wine Bar.

BLMN operates 1,186 full-service restaurants and off-premises-only kitchens and franchised 321 full-service restaurants. The company operates in 13 countries.

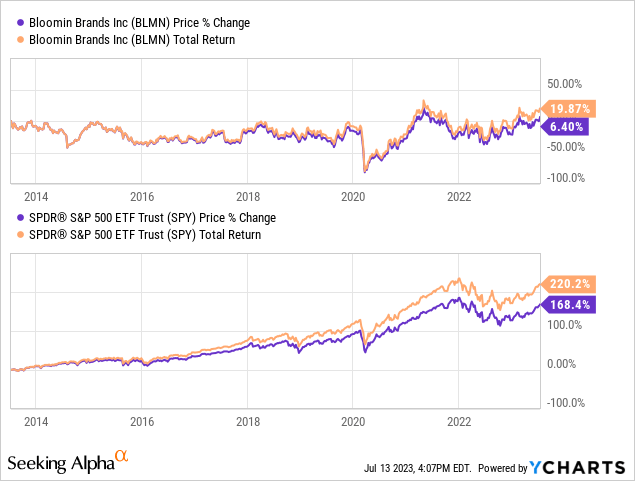

Share price

BLMN has performed poorly in the last decade relative to the S&P 500, although has marginally gained. This weakness is a reflection of a difficult period for the business, as it has faced increased competition and changing industry dynamics.

Financial analysis

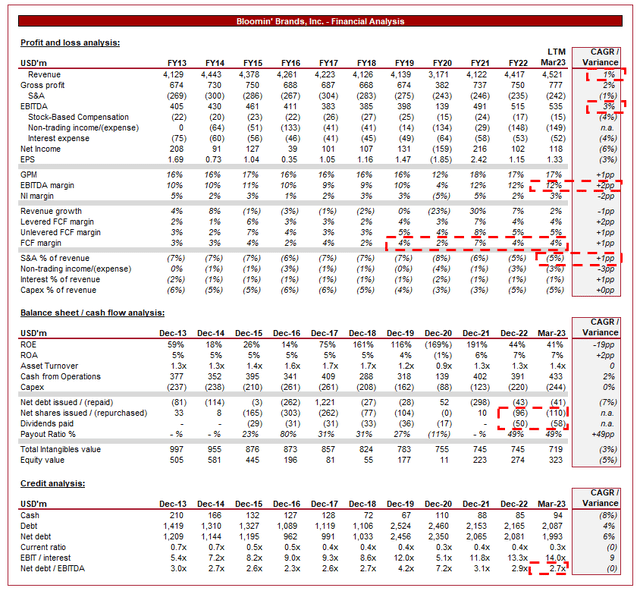

Bloomin’ Brands’ financials (Capital IQ)

Presented above is BLMN’s financial performance for the last decade.

Revenue & Commercial Factors

BLMN’s revenue has underwhelmed, with a 1% CAGR in the last 10 years, a rate below the inflation level during this period. Revenue has been below 1% in 5 of the fiscal years (excl. FY20), illustrating the weakness the business has had with maintaining positive growth.

Business Model

BLMN’s business model is focused on providing a high-quality and value-oriented dining experiences. The company strives to differentiate its brands through its unique concepts, signature dishes, and attentive service.

BLMN operates a mix of company-owned and franchised restaurants, allowing for ease of expansion while also maximizing its revenue generation from its IP. The restaurant industry, and the QSR segment in particular, has experienced a rapid transition toward franchising, as this provides greater certainty over revenue generation, reduces execution risk and the associated issues with direct control, and ease of expansion.

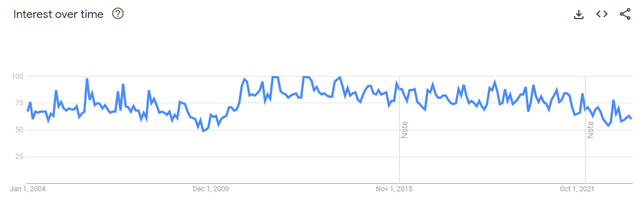

BLMN’s weak revenue is an illustration of a key weakness in the current business model. As the following graph illustrates, the interest in Outback Steakhouse has flatlined for most of the decade, with a downward trend in recent years.

Outback Steakhouse (Google Trends)

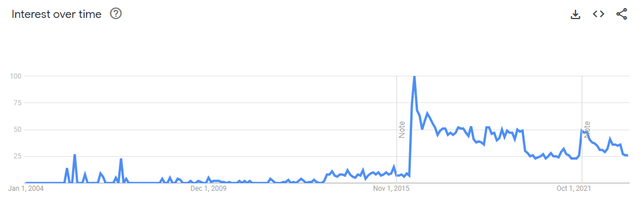

A similar trend is observed with its 2 other leading brands.

Carrabba’s Italian Grill (Google Trends) Bonefish Grill (Google Trends)

This implies an inherent weakness in the attractiveness of its restaurants. We believe this is likely a reflection of the increased competition in the market. With continued new entrants and the rise of delivery apps, there has been increased pressure to differentiate and provide consumers with a clear value proposition above-and-beyond the benefits of convenience. We believe BLMN’s brands have struggled with this. They operate in a highly competitive segment of the market, with no clear area of differentiation. As a result, the increased competition looks to have diluted its share of the market.

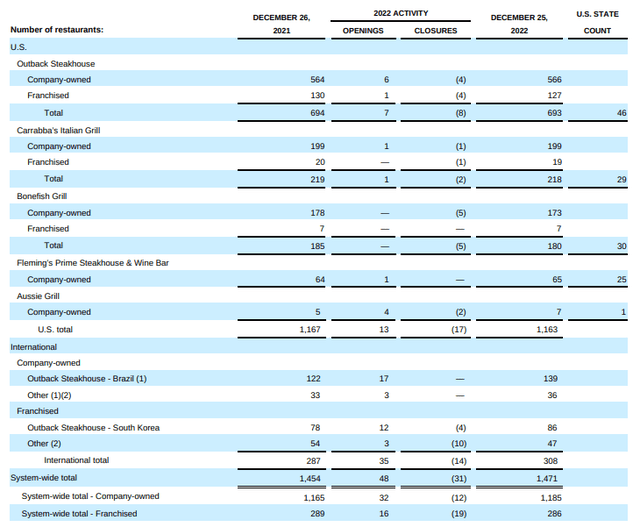

As the following table illustrates, the business is struggling to achieve consistent restaurant growth, with the US count declining in 2022. Importantly, the number of franchises is declining, implying an unattractive brand.

Store count (BLMN)

Competitive Positioning

The strength of the business is its brands and reach geographically but given the poor financial performance, it is clear it has a weak competitive position in the industry.

Restaurant Industry

Companies differentiate themselves through brand concepts, culinary expertise, restaurant dining experience, price, and customer loyalty programs. BLMN faces competition from other casual dining restaurant chains, including Darden Restaurants (DRI), Brinker International (EAT), Chipotle (CMG), Shake Shack (SHAK), and Texas Roadhouse (TXRH).

We are currently reviewing Cheesecake Factory (CAKE), and consider it to be a well-performing business (without standing out). We attribute this performance to the experience of dining at Cheesecake Factory. With a unique dining experience and a large menu, individuals are encouraged to dine in, especially in groups. No longer are restaurants just judged on the quality of food /price, but also on the wider experience. If consumers can order the food online, restaurants must convince consumers to come in-store.

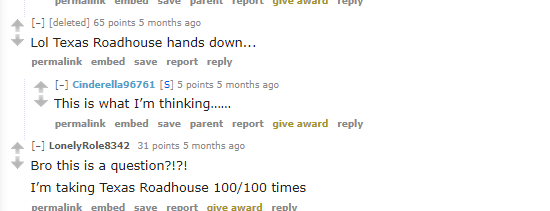

Further, we have already reviewed Texas Roadhouse and consider it a well-positioned business to a strong trajectory. Having considered reviews comparing Texas and Outback, the following best illustrates the differences.

1 (Business Insider) 2 (Business Insider) 3 (FixinTexas) 4 (Reddit) 5 (Reddit)

The consensus seems to be that not only are the steaks better at Texas Roadhouse, but the wider theme and atmosphere is better. The only area of contention looks to be the quality of service. This is a concerning assessment.

Growing consumer demand for healthier and more sustainable dining options necessitates menu innovation. This is where a chain such as Cheesecake Factory does well, as its large menu allows for the easy inclusion of vegan, gluten-free choices. For BLMN, however, this is problematic when it has a Steakhouse and Seafood chain.

The increasing popularity of food delivery services and off-premise dining has materially disrupted the dining experience, as consumers benefit heavily from convenience. This has contributed to tighter margins due to the app taking a cut, as restaurants have been forced to join these platforms.

One of the key risks of running a restaurant we highlighted above is execution. This is currently being felt through Rising labor costs, food prices, and other operational expenses, as inflationary pressure bites. We expect pressures to remain, as high competition will make it difficult to pass on price increases.

Expanding the company’s presence in international markets represent a key growth area for the business, as it continues to add locations in Brazil and South Korea. There is scope here for further expansion into the same countries, as well as new geographies, especially through franchising.

Economic & External Consideration

Current economic conditions represent a near-term threat to the business, as high inflation and elevated rates have the potential to contribute to a material slowdown in consumer spending. This has not occurred thus far, as resilient spending has allowed businesses to benefit from increased pricing.

In Q1, sales were up 9.1%, driven by an increase in menu prices, as well as improved comparable restaurant sales. All brands have experienced healthy growth, with their international segment exceeding 10%.

Margins

BLMN’s margins have gradually improved over the historical period, reaching an EBITDA-M of 12% and a NIM of 3%.

Margin improvement has been impressive, given the higher competition and increased deliveries. BLMN has exploited the gains made post-pandemic despite a revenue slowdown.

Outlook

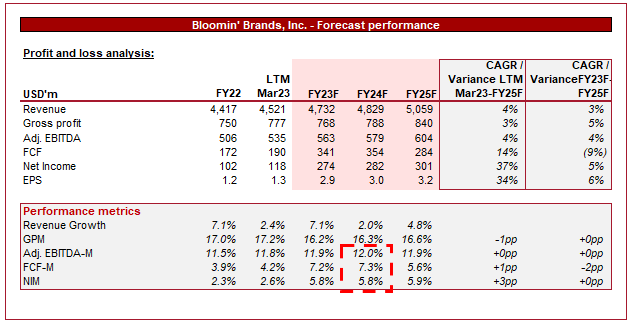

Outlook (Capital IQ)

Presented above is Wall Street’s consensus view on the coming 5 years.

Analysts are forecasting mild growth in the coming years, a reasonable expectation based on the continued expansion of new stores, as well as positive pricing. The key to outperforming this will be the successful expansion into new geographies.

Equally, if the US store count continues to decline and international expansion slows, the business could face a decline.

Margins are expected to normalize at the current level. This looks reasonable as OPM increased by 0.3% in Q1, implying a continuation of its upward trajectory.

Industry analysis

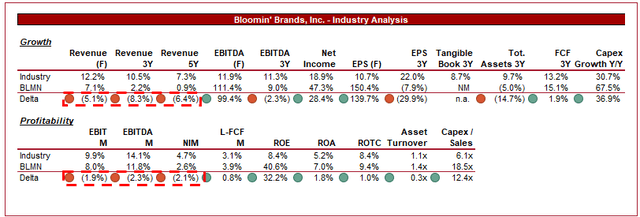

Restaurant (Seeking Alpha)

Presented above is a comparison of BLMN’s growth and profitability to the average of its industry, as defined by Seeking Alpha (37 companies).

BLMN performs poorly relative to peers, partially due to the industry weighting toward franchising, which contributes to higher margins.

BLMN’s biggest issue is growth, with a significant delta to the industry. This is a reflection of its unattractiveness, contributing to market share loss. This will restrict the ability to generate sufficient margin improvement to reach parity.

Valuation

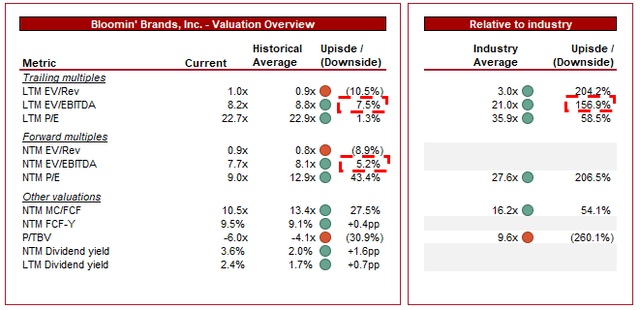

Valuation (Capital IQ)

BLMN is currently trading at 8x LTM EBITDA and 8x NTM EBITDA. This is a discount to its historical average.

Our view is that a small premium is likely warranted. The weakness in brand development and net closure of US locations is quite concerning but is offset by international development and margin improvement. Based on this, there is small upside available. The relative view is less useful, given the superiority of the market.

Final thoughts

BLMN has a strong national presence and is performing well expanding overseas. However, we are quite concerned about the competitive position of its brands. Not only are they unattractive relative to their nearest peers, but the value proposition does not look sufficient.

Operationally, the business has performed well, with improving margins and sufficient action to offset inflationary pressures. Alongside international expansion, the foundations for an improvement in performance are there.

BLMN looks slightly undervalued but we do not see sufficient upside to warrant a buy rating based on the commercial concerns.

Read the full article here